11:27 am

April 20, 2023

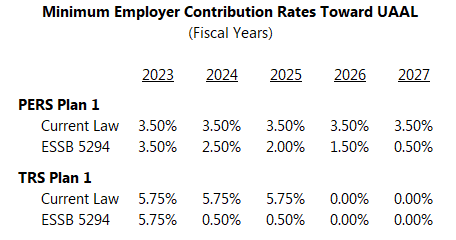

Washington’s public employee pension systems are well funded, with the exception of the Public Employees’ Retirement System (PERS) plan 1 and the Teachers’ Retirement System (TRS) plan 1. For years, the state has been making additional contributions toward the unfunded actuarial accrued liability (UAAL) in these two plans. Currently, the state pays a minimum contribution rate of 3.5% to amortize the UAAL in PERS plan 1 and 5.75% to amortize the UAAL in TRS plan 1, and those rates are effective until the plans are fully funded.

Meanwhile, the 2021–23 operating budget appropriated $800.0 million from the general fund–state (GFS) to be applied to the TRS 1 UAAL on June 30, 2023. (Effectively, this money came from the budget stabilization account, as I noted here.)

The Office of the State Actuary estimates that PERS 1 will be fully funded in 2026 and TRS 1 will be fully funded in 2023 under current law. However, because of the timing of the rate-setting process, the minimum contribution rates would stay in place through 2029 and 2025, respectively. As a result, in 2029, the funded status of PERS 1 would be 146% and the funded status of TRS 1 would be 142%. (See this post for more background.)

The Legislature has now passed ESSB 5294. (It has not yet been signed by Gov. Inslee.) As passed, the bill would reduce the minimum contribution rates for the UAAL beginning in FY 2024. The contribution rates would be stepped down, as shown in the table. Beginning in FY 2028, a 0.5% rate for PERS 1 and TRS 1 would be in effect only when they are less than 100% funded.

Additionally, the bill would reduce the $800 million extra payment to the TRS 1 UAAL to $250.0 million, saving $550 million for the GFS that could be used for other things in 2023–25. (Note, though, that the $800 million is one-time money that should be used for a one-time purpose.)

On top of that $550 million, the policy change in ESSB 5294 would reduce GFS appropriations by $888.3 million in 2023–25 and $266.3 million in 2025–27, according to the fiscal note. Both PERS 1 and TRS 1 would be fully funded in FY 2027.

The Senate-passed operating budget includes savings from ESSB 5294 totaling $807.7 million in 2023–25 and $1.055 billion in 2025–27, plus the $550 million in savings in 2021–23. The House-passed operating budget would repeal the $800 million extra payment entirely, and it assumes passage of HB 1201 (the companion of the original SB 5294). The House-passed budget assumes savings from the policy bill of $337 million in 2023–25 and $1.194 billion in 2025–27.

Categories: Budget , Employment Policy.