9:05 am

March 11, 2026

The Legislature has passed 2SSB 5292. If signed by Gov. Ferguson, the bill would change the paid family and medical leave (PFML) tax rate-setting formula. However, more will need to be done to address program solvency.

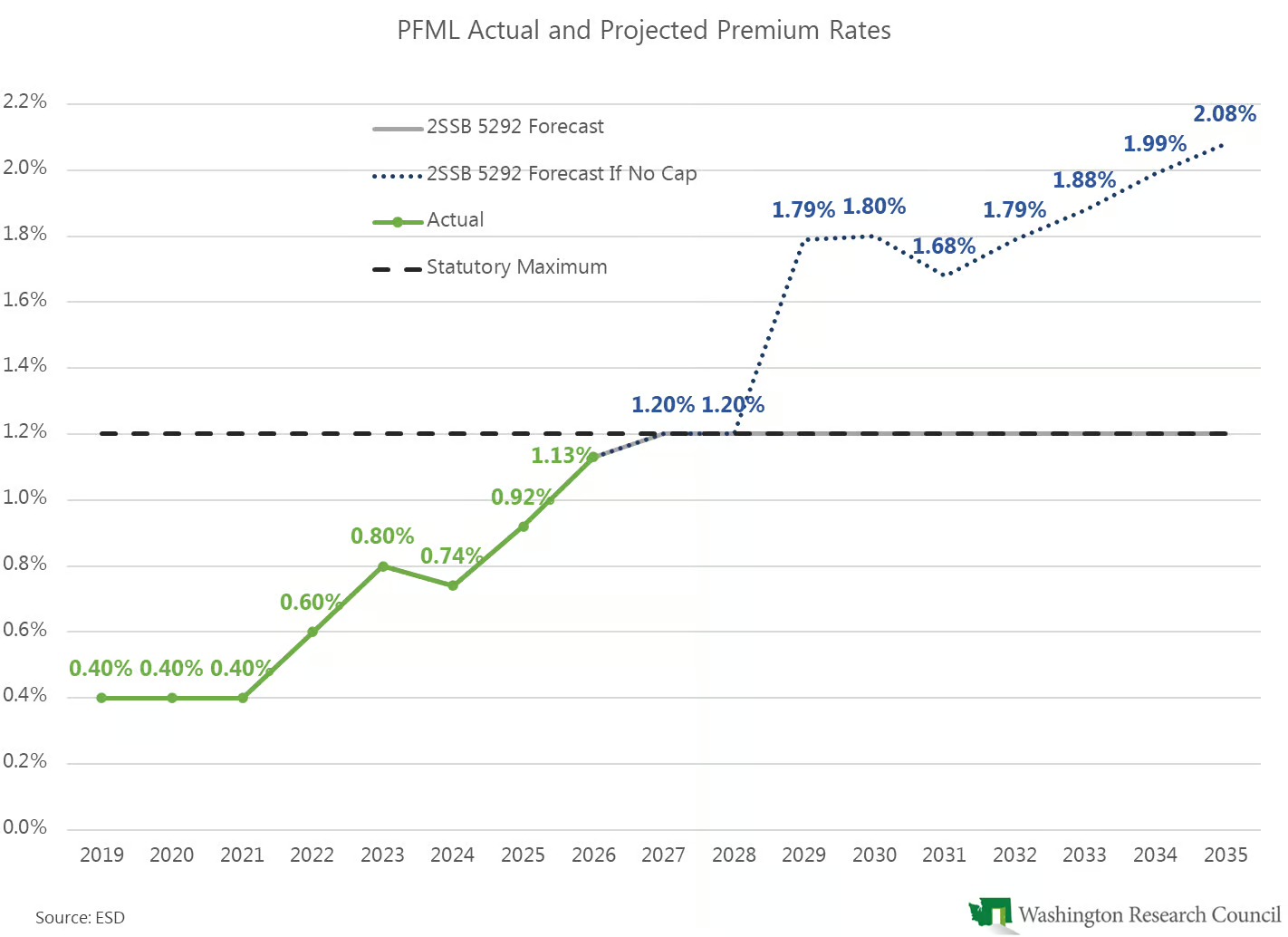

Initially, the tax rate for the program was set at 0.4%. Beginning in 2021, the rate was set based on the family and medical leave (FMLI) account’s balance as of Sept. 30 of the prior year. The tax rate was allowed to range from 0.1% to 0.6%. On top of that, solvency surcharges were allowed, up to 0.6%. Thus, the maximum rate initially contemplated was 1.2%.

The PFML program experienced cash deficits in 2022. The state responded by appropriating $350 million from the general fund–state to the family and medical leave account in 2022 and implementing new actuarial and reporting requirements for the program. (The $350 million appropriation was reduced to $200 million in the 2023 supplemental budget.) Legislation approved in 2023 changed the tax rate structure, which was meant to maintain a three-month reserve for the program. (The 1.2% maximum tax rate was retained in the 2023 legislation.) By November 2023, the PFML actuary was already recommending another change to the rate structure, to use a forward-looking approach. Last Fall, the actuary estimated that the premium rate would hit 1.2% in 2027 and that the rate would not be adequate to cover expenditures beginning in 2028.

Under 2SSB 5292, effective Jan. 1, 2028 (for 2029 rates), the premium rate would be set based on the PFML actuary’s annual report on the experience and financial condition of the program. The rate must be the lowest necessary to maintain solvency and end the year (beginning in 2030) with a four-month reserve. The maximum tax rate in statute remains 1.2%.

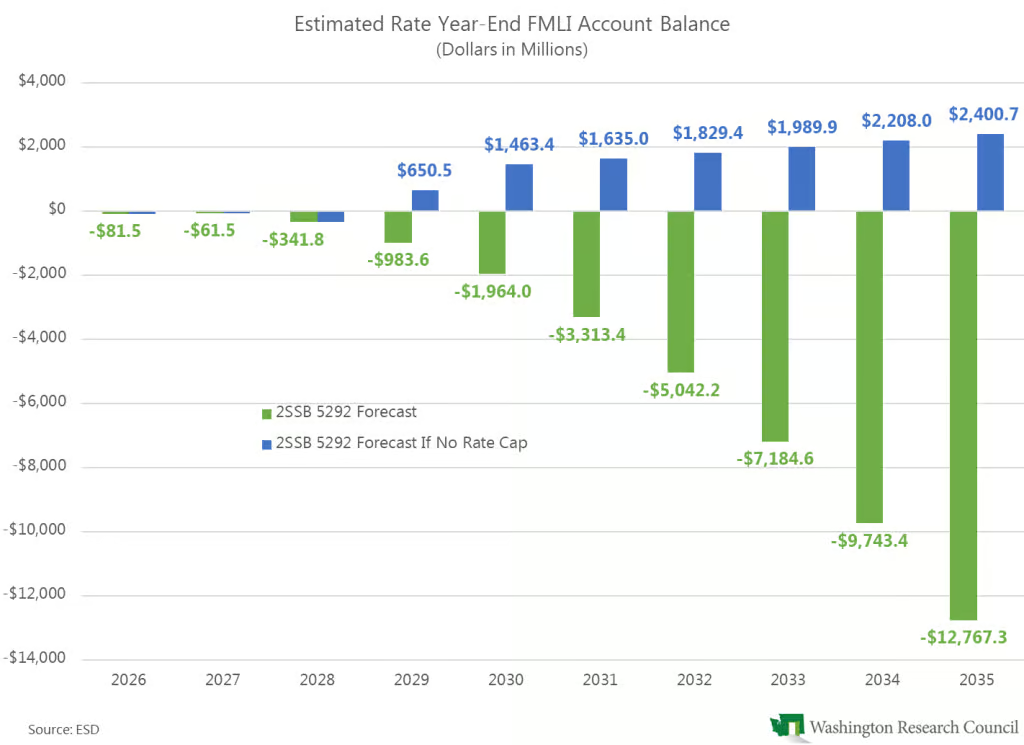

In the fiscal note, the Employment Security Department (ESD) estimates that the rates for 2027 and 2028 (calculated under the prior formula) will hit the statutory cap. Then, under 2SSB 5292, the rates would remain there for the entire forecast window. ESD also provided an estimate of what rate would be indicated by the new rate structure (and reserve requirement) in the absence of a cap. In that situation, the rate would rise to 2.08% in 2035 in order to maintain solvency and a four-month reserve.

ESD also included an estimate of year-end FMLI account balances under current law, 2SSB 5292 as passed by the Legislature, and 2SSB 5292 without a rate cap. ESD notes, “in either scenario with a 1.20% cap the Paid Leave account will continue to experience periods of insolvency, growing over the 10-year projections as the premium rate cannot keep up with the program expenditures driven by program growth unrelated to 2SSB 5292.”

The estimated shortfalls in the FMLI account under current law and 2SSB 5292 (with the cap) are now estimated to be much deeper than estimated by ESD in September. It’s possible the account could need another GFS backfill in the coming years. As I noted in September, increasing the premium rate would not be the only solution. The state could make changes to benefits.

Both the House- and Senate-passed operating budgets included an identical proviso that would require ESD to report on the current state of the PFML program by Nov. 1, 2026. The report would have to include an evaluation of program solvency and integrity, including potential program changes and an economic analysis of those potential changes. Look for PFML solvency to be an issue again in the 2027 legislative session.