9:22 am

January 25, 2024

Earlier this month, the Office of the State Treasurer (OST) released its annual Debt and Credit Analysis report, which provides data on state debt and recommendations for the Legislature.

At the end of FY 2023, Washington had $21.403 billion in outstanding bonds. That was up just 0.6% from $21.269 billion in FY 2022. (Of total outstanding bonds, 66% were capital budget-related and 34% were transportation budget-related.) Net debt service in 2023 was $1.944 billion, an increase of 3.6% over 2022.

According to the report, the state will pay a total of $21.255 billion from 2024 through 2048 in debt service on currently outstanding capital budget-related bonds. The state will pay a total of $11.054 billion from 2024 through 2051 on currently outstanding transportation bonds.

Meanwhile, as of the end of FY 2023, there was $8.589 billion in authorized but unissued capital budget bonds and $7.803 billion in authorized but unissued transportation budget bonds.

The report shows that Washington is a high debt state:

Washington’s debt burden places it among the nation’s most heavily indebted states when assessed by several different metrics. For example, according to Moody’s, Washington ranks in the top ten of all 50 states for debt per capita (7th), debt as a percentage of revenues (5th), and debt as a percentage of personal income (11th).

The credit rating agencies have given Washington high marks despite our debt because of our strong economy, good fiscal governance (including the four-year balanced budget requirement and constitutionally-required deposits to the rainy day fund), and well-funded pensions. To maintain and improve our high credit ratings (which mean the costs of borrowing are lower), OST recommends that the Legislature:

- Maintain reserves of at least 10% of annual revenues from funds subject to the outlook (NGFO);

- Limit projected capital budget debt service costs to 5–6% of general state revenues and limit transportation budget debt service to 50% of pledged revenues; and

- Continue to fully fund state pension contributions.

On reserves, OST notes, “The proposed minimum target of 10% of total reserves as a percentage of revenues is supported by both Moody’s and S&P’s credit rating methodologies.” Further, according to OST, “In general, rating agency criteria suggest that states with higher debt service costs as a percentage of revenues should also have higher total reserves as a percentage of revenues to maintain strong ratings.”

Regarding debt service costs, debt service on capital budget bonds was 4.46% of general state revenues in FY 2023. OST characterizes that as a “strong financial position.” But OST estimates that debt service as a percent of general state revenues will grow to 5.01% in 2026 and 6.02% in 2039. OST estimates that we will reach the statutory debt limit in 2048.

On pensions, the report notes that Washington currently assumes a long-term rate of return of 7% but warns that may be “aggressive.” (The higher the assumed rate of return, the more the state is relying on future returns to cover benefits.) OST suggests a target of 6% could be more accurate: “If the state’s actual rate of return is lower than 7.0%, and/or the state has made less than the annual actuarially determined contribution, the unfunded liability will be greater than projected and require higher annual funding contributions in the future.” The investment rate of return was assumed to be 8% in 2010. It was stepped down over time, reaching 7% in 2021. (Reducing the assumption meant that the state had to increase its pension contributions.)

Additionally, OST reported this month that S&P has updated its outlook for Washington from “stable” to “positive.” Washington is still rated AA+ by S&P, but this change means “there is a one-in-three chance we could raise our rating over the next two years.” S&P notes, “All else equal, we could raise the rating if Washington demonstrates its commitment over time to maintaining and replenishing reserves through positive economic periods. In addition, a moderation in debt levels, coupled with faster amortization, could support upward rating potential.”

S&P dings Washington for not having formal reserve levels:

Under our state ratings methodology, S&P Global Ratings assigned Washington a score of ‘1.5’ on a four-point scale, with ‘1.0’ being the strongest and ‘4.0’ being the weakest, resulting in an indicative ‘AAA’ rating. However, we have notched down to ‘AA+’ given the state’s limited formal reserve levels, which sets them apart from higher-rated peers.

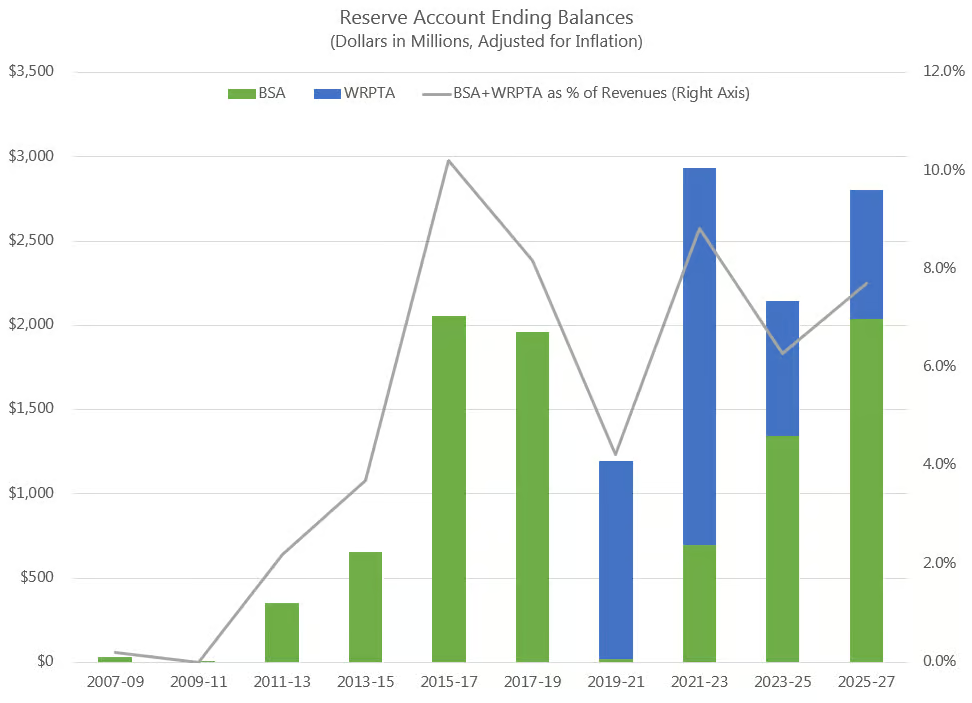

S&P argues that because Washington doesn’t have formal reserve levels, low balances are allowed “to persist through periods of economic and revenue softness.” Washington requires that 1% of general state revenues be deposited in the budget stabilization account (BSA, or the rainy day fund) each year, but state law doesn’t specify a minimum amount that should be kept in reserve, nor is there a firm maximum. (When the BSA balance exceeds 10% of general state revenues, the funds above 10% may be withdrawn for school construction with by just a simple majority vote.) According to the National Association of State Budget Officers, as of 2021, only five states had minimum reserve levels and 33 states had maximum reserve levels.

Also this month, Moody’s affirmed Washington’s Aaa rating and Fitch affirmed Washington’s AA+ rating. According to Fitch, one factor that could lead to an upgrade for Washington would be if it is able “to sustain formal reserves, other than those in ending general fund balance, to at least pre-pandemic levels.”

The enacted 2023–25 budget left $2.143 billion in the BSA and the Washington rescue plan transition account (WRPTA, or the shadow reserve account created during the pandemic). Adjusted for inflation, this amount would exceed pre-pandemic levels in absolute terms, but not as a percent of NGFO revenues. Gov. Inslee’s supplemental proposal would drain the WRPTA and leave $1.33 billion in the BSA in 2023–25. That would not match pre-pandemic levels by either measure. The chart shows the ending balances for the BSA and WRPTA over time (and as assumed in the enacted 2023–25 budget). It also shows the ending balances as a percent of NGFO revenues in the final year of the biennium.