12:19 pm

April 29, 2026

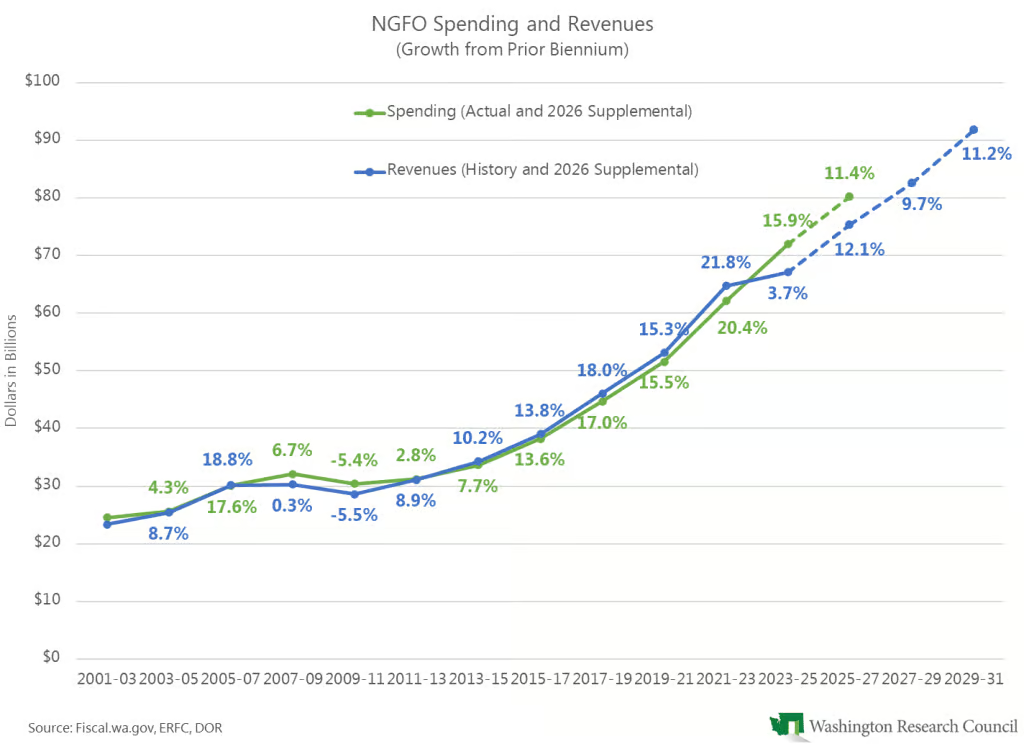

Washington’s budget problem took root in 2023–25, when legislators appropriated substantially more than they expected to collect in revenues. Legislators have widened the gap between spending and revenues since then (despite substantial tax increases in 2025 and 2026). Will the new income tax fix the problem on its own?

Officially, the 2026 supplemental balances over four years, assuming dubious accounting choices and the first year of income tax revenues in FY 2029. The official budget outlook estimates the ending balance of funds subject to the outlook will go from negative $802 million in FY 2028 to positive $653 million in FY 2029. Then, in 2029–31, there will be two full years of income tax collections. 2029–31 is outside the current outlook window, so it might be tempting to assume that all budget problems are thus solved.

That is highly unlikely. First, legal and ballot challenges to the income tax could mean that revenues are never collected. Second, even assuming the tax stands, the current budget balances through 2027–29 because it assumes that appropriations will grow by just 2.8% that biennium. That does not include any spending on new collective bargaining agreements for state employees, other policies the Legislature may want to adopt, or any currently unforeseen changes to the cost of continuing current services.

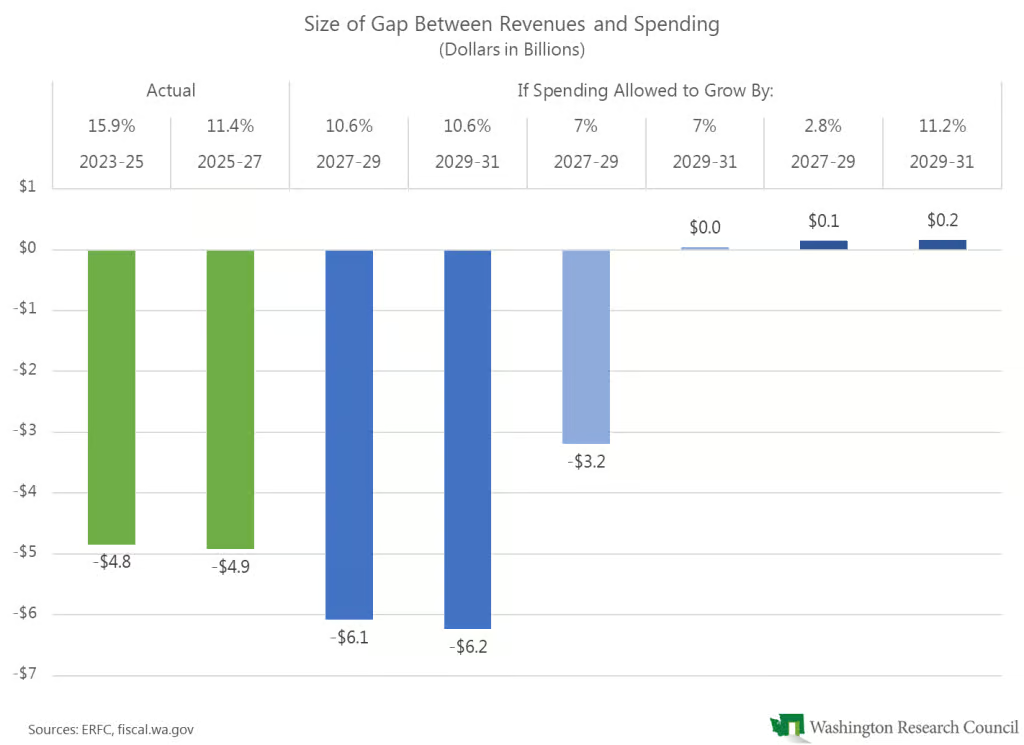

To put 2.8% spending growth in perspective, consider the chart below. As revised this year, 2025–27 appropriations are 11.4% higher than actual spending in 2023–25, and 2025–27 appropriations are $4.9 billion higher than estimated revenues for 2025–27. (Revenues in the chart include the income tax and other tax changes adopted this year.) The last time biennial appropriations grew by less than 3% was in 2011–13—when the state was still dealing with the revenue losses from the Great Recession.

So while it’s true that the income tax could help the state close the gap between spending and revenues, the state must also limit spending growth significantly. Otherwise, spending will remain on a trajectory that is higher than, and parallel to, revenues.

The chart below shows some hypothetical scenarios. (The scenarios assume the revenues in the February forecast plus the 2026 tax changes. If the revenue forecast falls, spending growth would also need to decrease.) For example, biennial spending growth has averaged 10.6% since 2001–03. If appropriations grow by that average in 2027–29, the gap between spending and revenues would grow to $6.1 billion. On the other hand, if spending growth is kept to 2.8% next biennium, then spending could grow with revenues in 2029–31 (by 11.2%).