1:39 pm

April 23, 2026

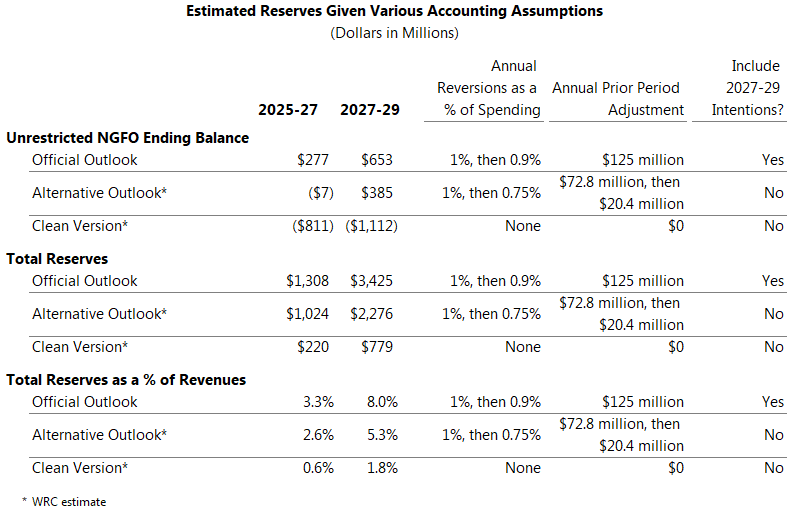

Yesterday the Economic and Revenue Forecast Council (ERFC) approved the official outlook based on the 2026 supplemental operating budget. Officially, the budget left an unrestricted ending balance in funds subject to the outlook (NGFO) of $277 million in 2025–27 and $653 million in 2027–29.

These are larger ending balances than assumed in the estimated conference report outlook, by $46 million in 2025–27 and $90 million in 2027–29.

The ending balances in the official outlook are different than in the conference report outlook because the official outlook includes updated revenue estimates based on the enacted tax legislation, the impact of vetoes, and an increase to reversions related to a double counting of $71 million in the budget that was meant to restore program integrity savings.

The official unrestricted NGFO ending balance for the current biennium is very low, as the chart shows. Meanwhile, since the February 2026 revenue forecast, general fund–state collections have come in below forecast. That doesn’t mean that the June NGFO revenue forecast will decline; but, combined with the expected $802 million shortfall in FY 2028 (the first year of 2027–29), it suggests that the size of the cushion may prove to be inadequate.

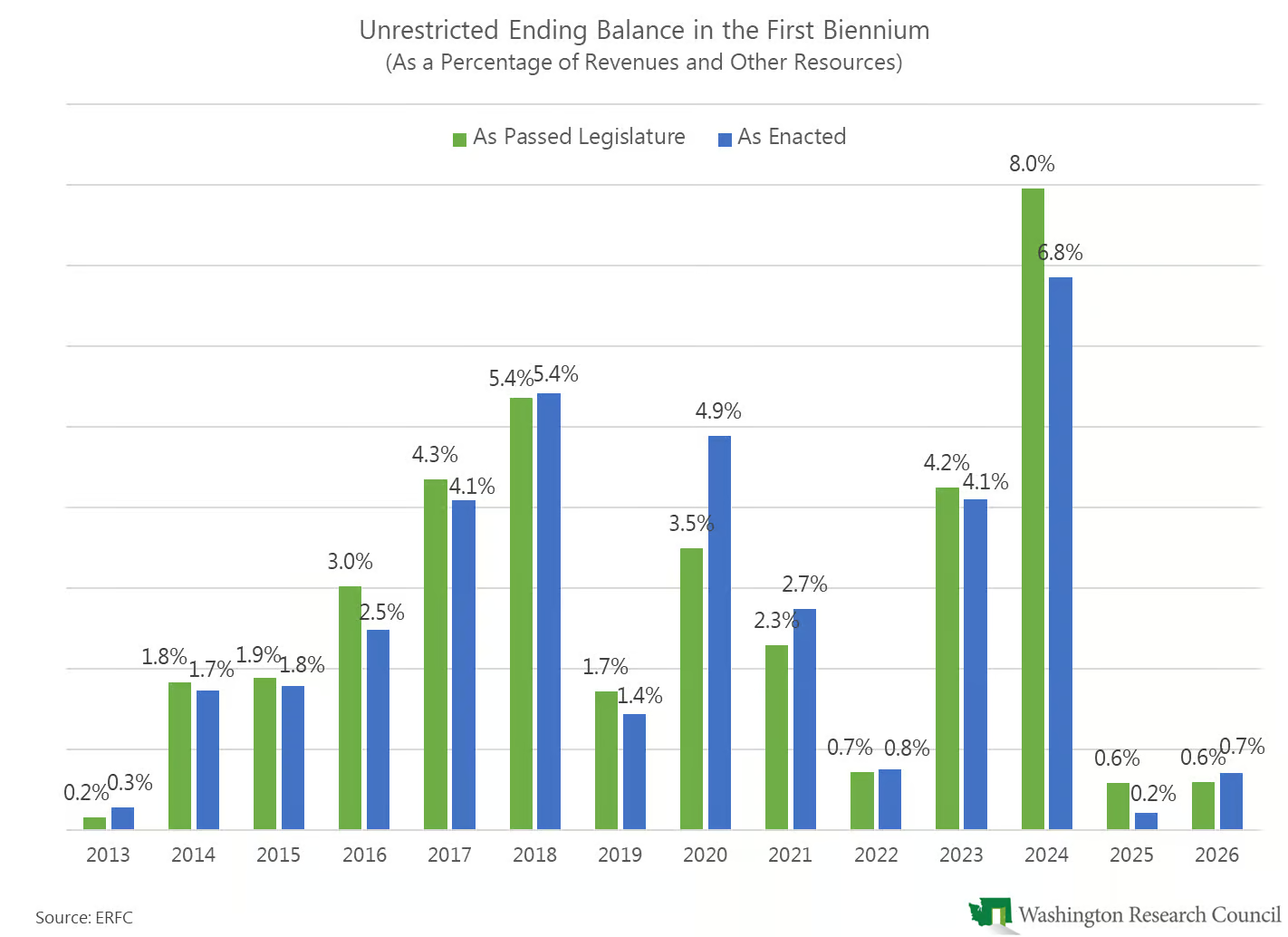

Officially, total reserves (including the unrestricted NGFO balance and the budget stabilization account) as a percent of revenues are 3.3% at the end of 2025–27 and 8.0% at the end of 2027–29.

However, the small official cushion may not be realistic. As I wrote last week, the ERFC decided to rubber stamp unusual accounting assumptions made by budget writers in the conference report outlook. The ERFC also decided to allow the inclusion in the outlook of two potential appropriations and one potential transfer for 2027–29, even though they will require policy level decisions next year.

During the ERFC meeting, Rep. Orcutt requested an alternative outlook that assumes the same reversion percentage as the enacted 2025 budget (it was lower than the assumption for the 2026 budget, but still higher than the pre-2023 assumption), that does not increase the assumption for prior period adjustments, and that does not include the 2027–29 transfer to the BSA or intended 2027–29 appropriations for free school meals and local governments. This alternative is not yet available, but the table below includes my estimate of how the changes would affect reserves.

The table shows how much the bottom line can change depending on the accounting assumptions. The “clean version” focuses on actual appropriations and adopted resources.

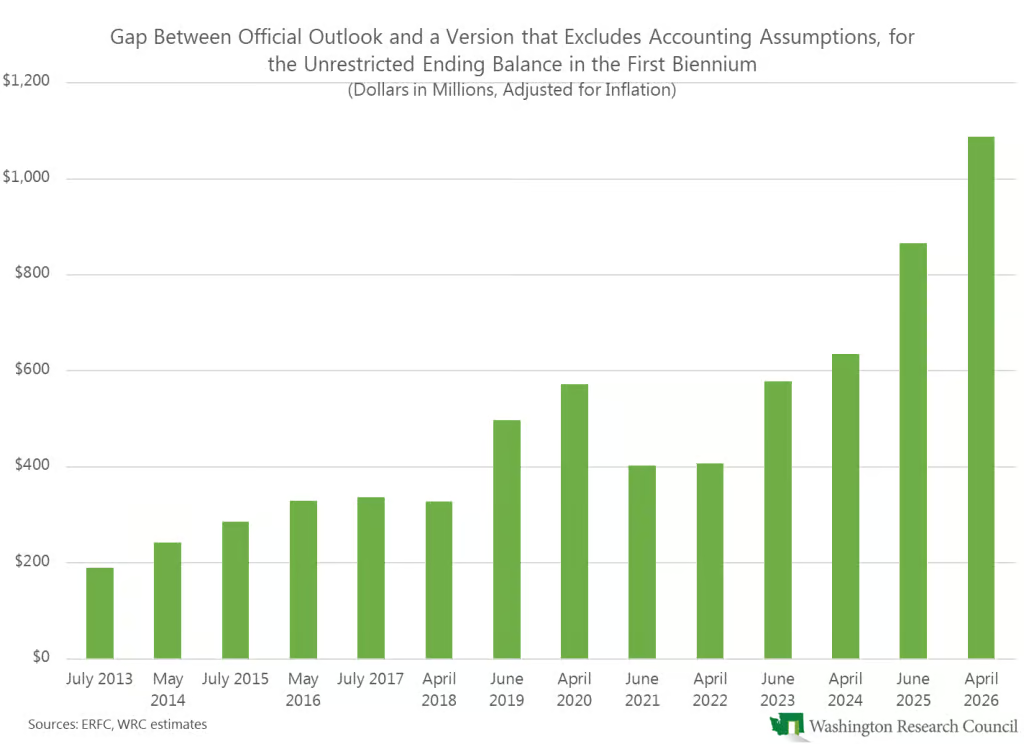

As I discussed here, playing around with these assumptions during the budget process began in 2023 and has accelerated since. The chart below compares the unrestricted NGFO ending balance in the first biennium in the official outlook to a version without any assumption for reversions or prior period adjustments. The size of the bar shows the size of the gap between the two. For example, for the budget adopted in 2026, the official ending balance for the biennium is $277 million, but the balance without the assumptions is -$811 million. The difference between the two is $1.088 billion. This indicates that, beginning in 2023, accounting assumptions have increasingly been used to help fill in the gap between spending and revenues.