12:49 pm

April 14, 2022

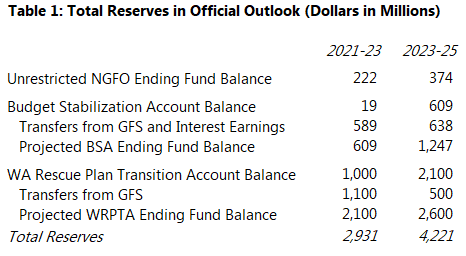

Today the Economic and Revenue Forecast Council (ERFC) adopted an official outlook based on the 2022 supplemental operating budget. Incorporating all actions this session and the governor’s vetoes, the budget leaves an unrestricted ending balance in funds subject to the outlook (NGFO) of $222 million in 2021–23 and $374 million in 2023–25.

It has been customary since the very first outlook to also show the reserves in the budget stabilization account (BSA, or the rainy day fund). Every outlook has shown the unrestricted NGFO ending balance and the BSA ending balance separately, along with a line that combines the two to reflect total reserves.

Last year the Legislature created the Washington rescue plan transition account (WRPTA), which is essentially a shadow reserve account. The account may be used very broadly: “Allowable uses of moneys in the account include responding to the impacts of the COVID-19 pandemic including those related to education, human services, health care, and the economy. In addition, the legislature may appropriate from the account to continue activities begun with, or augmented with, COVID-19 related federal funding” (see Sec. 1902 of last year’s budget). As we noted last year, given these allowable uses, the WRPTA could be used to fund the costs of last year’s child care bill, which was initially funded with federal relief money and which was expected to be funded with capital gains tax collections going forward. (Moreover, the account is not restricted by the constitution, so the Legislature could easily alter the allowable uses going forward.)

Although $1 billion was deposited in the WRPTA last year (and although more is transferred in the current budget), its balance has not been included as reserves in subsequent budget outlooks. The outlook presented to the ERFC today also did not include the WRPTA balance.

During the meeting today, Sen. Rolfes asked if it would be possible to add the WRPTA balance to the summary of reserves in order to be more transparent. David Schumacher of the Office of Financial Management agreed that it would be appropriate. Treasurer Pellicciotti also indicated that the WRPTA balance should be more transparent (to both the public and the ratings agencies) given the broad allowable uses of the fund. (As I’ve written, including the WRPTA balance substantially improves the level of reserves.)

Ultimately, the ERFC voted to adopt the outlook, with the addition of a section showing the WRPTA balance. An updated outlook has not yet been posted reflecting this change, but Table 1 below shows what it might look like. Including the NGFO, BSA, and WRPTA, total reserves are estimated to be $2.931 billion in 2021–23 and $4.221 billion in 2023–25.

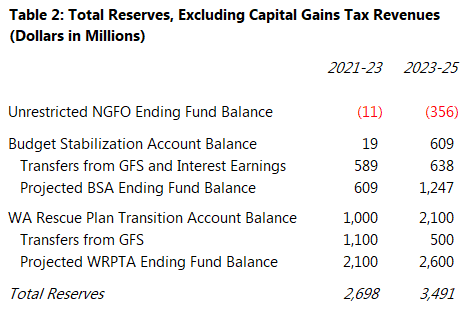

There is a big caveat to all of this. Last month, the ERFC decided to continue to assume capital gains tax revenues in the outlook. The outlook adopted today includes those revenues. However, Rep. Orcutt had asked for an alternative outlook that does not assume capital gains revenues—this alternative was included in the meeting materials (see page 20). Without the capital gains revenues, the enacted budget would not balance in either biennium. The unrestricted NGFO ending balance would be negative $11 million in 2021–23 and negative $356 million in 2023–25. That said, those shortfalls are easily covered by reserves in either the BSA or the WRPTA (see Table 2). Total reserves would be $2.698 billion in 2021–23 and $3.491 billion in 2023–25.

Tags: 2022supp