2:30 pm

March 31, 2026

Gov. Ferguson has signed ESSB 6346, which imposes an income tax. The bill additionally reduces some sales taxes and some business and occupation (B&O) taxes and expands eligibility for the Working Families Tax Credit (WFTC). (I wrote about the details of the final bill last week.)

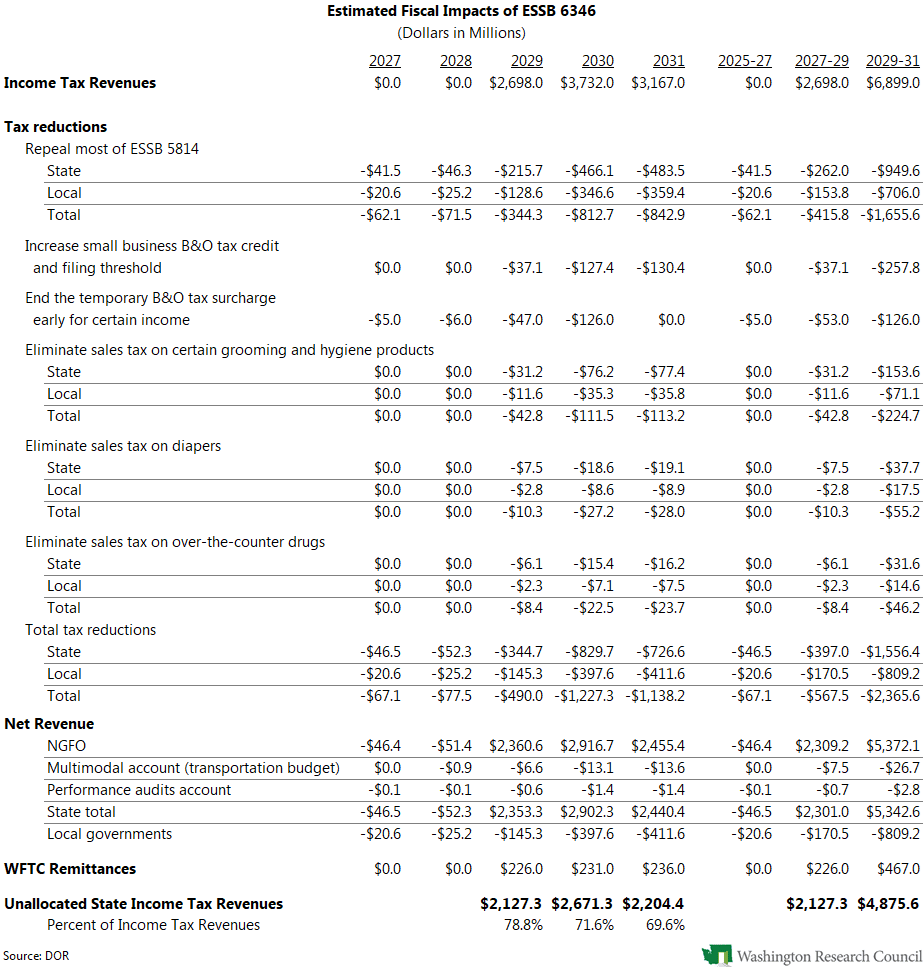

The fiscal note for the enacted bill estimates that it will reduce state revenues by $46.5 million in 2025–27 and increase state revenues by a net of $2.301 billion in 2027–29 and $5.343 billion in 2029–31. (2029–31 is the first biennium with two years of income tax collections.) These impacts will mainly be to funds subject to the outlook (NGFO), but they also affect two other state accounts. In addition to the state impacts, the bill’s sales tax changes will reduce local government revenues. (Note that the fiscal note assumes, “In response to the new tax, affected taxpayers do not reduce taxable income.”)

State spending on WFTC remittances is estimated to increase by $226.0 million in 2027–29 and $467.0 million in 2029–31. (Although labeled a tax credit, WFTC remittances are actually appropriated in the operating budget.)

While most of the bill’s tax relief provisions are effective Jan. 1, 2029 and will only take effect if the income tax remains law, there are a few provisions that are effective July 1, 2026. These, including ending the temporary B&O surcharge for food wholesalers and excluding some entities from the ESSB 5814 changes, will be effective regardless of whether the income tax remains law.

The table below shows the estimated impacts of ESSB 6346 by provision, including the impacts to local governments. (Ending the temporary B&O surcharge early is expected to reduce revenues by more than shown for FY 2029. According to the Department of Revenue, it will affect fewer than three healthcare taxpayers during that period, so it is not disclosable.) After the tax reductions and WFTC remittances, the state will retain about 70% of annual income tax revenues for general spending.

In a press release, the governor’s office claims that 47.3% of revenue will go “back to Washington families and small business owners” in FY 2030. According to the Office of Financial Management, this includes the state portion of the tax reductions in the table below, the WFTC remittances, $134.9 million for the fair start for kids account (FSKA), $144 million for free school meals, and $200 million for a city and county fiscal health account. I think including the last three items is a stretch.

First, ESSB 6346 does indeed specify that 5% of the income tax revenues will be deposited in the FSKA. The FSKA is a fund subject to the outlook, and monies in the account are dedicated for “child care and early learning purposes.” ESSB 6346 does not make any appropriations from the FSKA, and the outlook for the 2026 supplemental budget does not assume any FSKA appropriations. Further, there is nothing that would prevent the Legislature from simply shifting funding for current child care and early learning programs from the general fund–state to the FSKA. Consequently, the 5% of income tax revenues transferred to the FSKA ($321.5 million in 2029–31) is essentially unallocated state revenues.

Second, there is nothing in ESSB 6346 that provides for free school lunches, other than intent language. The 2026 supplemental budget does include $140 million in the outlook for 2027–29 for this purpose, and the budget requires the state to forecast the number of students who might participate. But there is no guarantee the 2027 Legislature will appropriate those funds.

Third, the 2026 supplemental budget outlook includes $200 million in 2027–29 for a “proposed city and county fiscal health account beginning in FY 2029.” There is nothing about this in the budget bill itself, and ESSB 6346 doesn’t create the account.

It’s possible that the Legislature will fund these three items in the future, but it may not—especially considering the already expected shortfall in the 2027–29 budget.

Meanwhile, the Seattle Times has a nice chart in a story by Jim Brunner that shows how the income tax revenues are used in FY 2030.

Regarding the sales tax exemptions, Brunner’s story quotes Sen. Pedersen: “Anything that you buy in a grocery store pretty much is going to be tax-free whether it’s Advil or Crest toothpaste, or Pampers or whatever.” “Pretty much” is doing a lot of work there. ESSB 6346 defines “grooming and hygiene products” narrowly as “soaps and cleaning solutions, shampoo, toothpaste, mouthwash, antiperspirants, and sun tan lotions and screens.”

Here’s an inexhaustive list of things people regularly buy in grocery stores that will still be subject to sales tax: prepared food, soft drinks, bottled water, alcohol, dietary supplements, Band-Aids, conditioner, toothbrushes, floss, lotion, shaving cream, razors, Ziplock bags, paper plates, rubber gloves, toilet paper, trash bags, etc. I’m not suggesting that the sales tax exemption should be expanded to these items; I’m just pointing out that almost everyone will still pay sales tax at the grocery store.