Washington has been getting very high marks from the credit rating agencies in recent years, in part due to Washington’s constitutionally-required rainy day fund and four-year balanced budget requirement. This is important because it means Washington can sell bonds at lower interest rates, lowering the cost of borrowing and helping to limit the share of the operating budget that is devoted to interest payments.

Credit analysis updates from the rating agencies in July incorporated the budgets adopted this session. As I wrote this summer, they highlighted some good and bad budget choices made by the Legislature. New credit updates were released last month affirming Washington’s Aaa (Moody’s) and AA+ (S&P and Fitch) ratings.

However, S&P revised its outlook for Washington’s general obligation bonds from “positive” (meaning that the rating may be raised) to “stable” (meaning the rating is not likely to change). This reflects S&P’s

view that the state’s budget balancing efforts are expected to be more challenging given the softened revenue outlook driven by an expected deceleration in economic growth and ongoing cost pressures. In our view, this will likely result in operating pressure necessitating the use of available reserves at a time when we had expected sustained reserve preservation.

S&P notes that Washington is facing a budget deficit given the September revenue forecast. They write that because Washington enacted a tax package earlier this year, “resolving these forecast gaps will be more financially difficult and that there could be fewer options available for resolving them.” Although S&P suggests that the use of reserves may be the ultimate solution, that could lead to a rating downgrade:

We could lower the rating if the state experiences sustained deficits resulting from structural pressures, or delays taking corrective action in response to potential financial pressures. We could also lower the rating if the state opts to use its available reserves, namely its BSA, to address structural pressures and fails to replenish balances in a timely manner.

S&P rates Washington’s outlook as stable because it expects Washington to “continue to take corrective budgetary action to align expenditures with revenue over the course of the biennium. We expect strong budgetary management will monitor potential pressures and that the state will maintain structural balance by balancing expenditure growth with available resources in future budgets.”

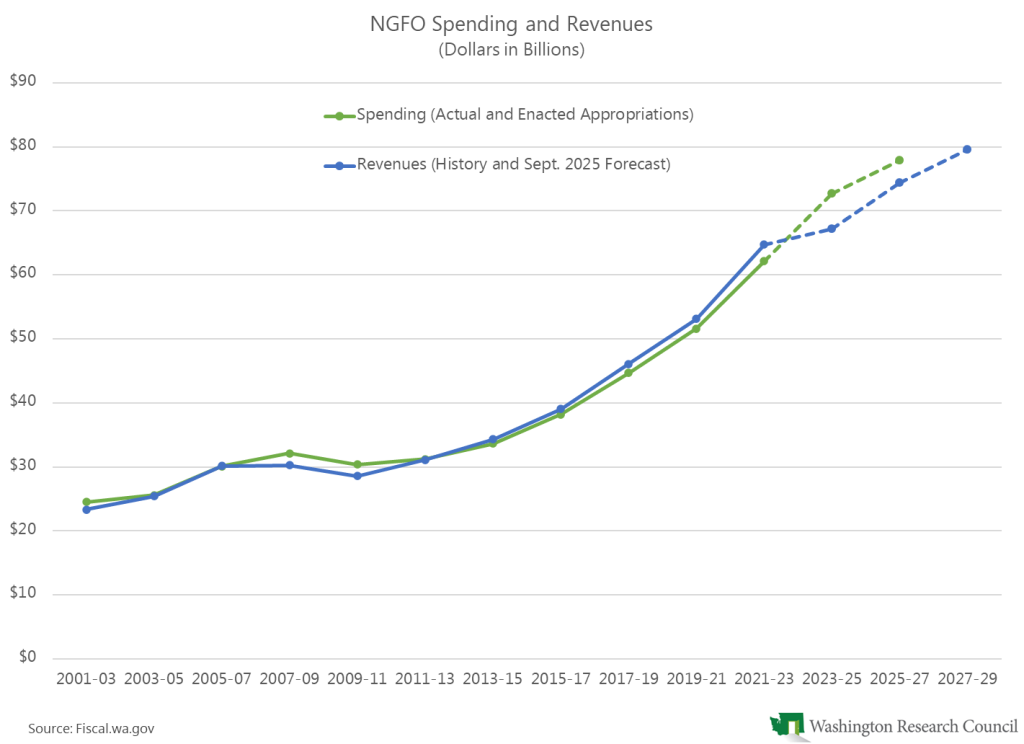

Indeed, one of the reasons for the budget shortfall this year was that the state increased appropriations in 2023–25 by 15.8% when revenues were expected to grow by just 3.5%. As the chart below shows, the 2025–27 budget continued the imbalance between spending and forecasted revenues.

Finally, S&P favorably notes Washington’s four-year balanced budget requirement and regrets its use of reserves (sweeping the budget stabilization account in 2021 was another cause of the shortfall):

The state’s active management practices and forecasting have historically benefited it in tracking potential budgetary pressures, including its most recent stresses, and we view its statutory mechanisms for ensuring budgetary balances in out-years as prudent. Despite the state’s buildup of combined reserves in recent years, its planned spend-down of larger beginning balances over the past few fiscal years has led to less flexibility as it navigates these pressures, in our view.