11:27 am

June 20, 2022

A story in the Seattle Times about Seattle’s projected operating deficits states, “the city must find a sustained new revenue source.” (The headline: ‘“No obvious way out’: Seattle facing $117 million revenue shortfall in 2023.”) Although it’s true that the city is projecting general fund operating deficits over the next several years, it is not the case that revenue is declining.

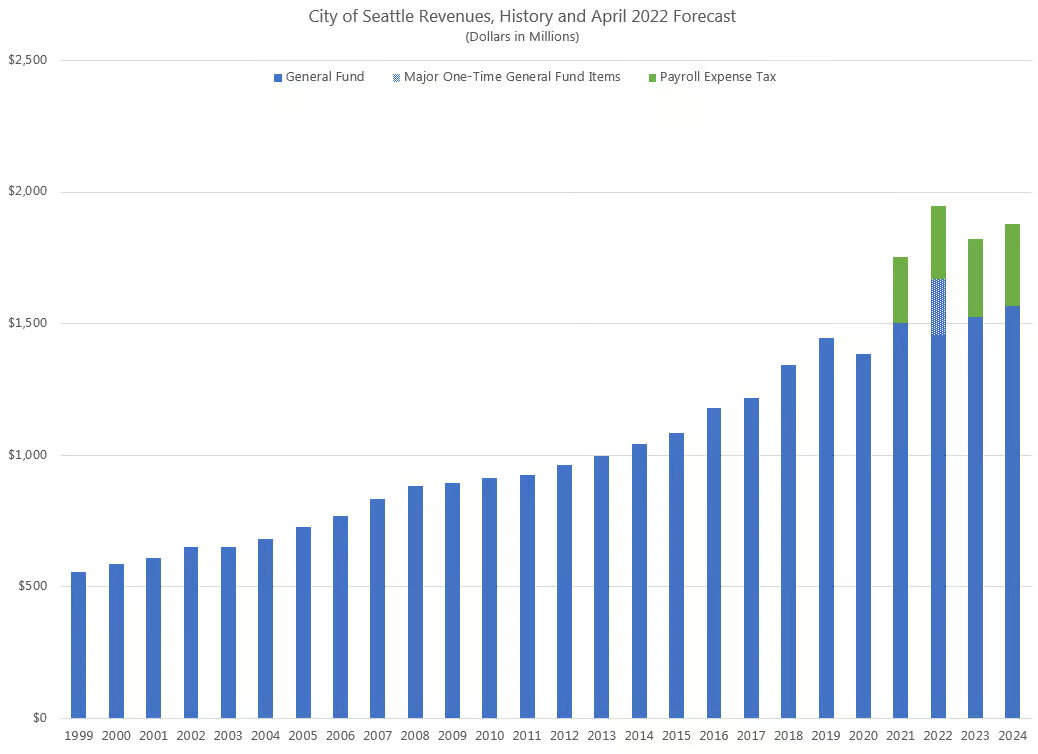

I wrote about the city’s projected $117 million operating deficit for 2023 here. Regular general fund revenues were down slightly in 2022, but major one-time general fund dollars that year (including, e.g., transfers of federal funds and payroll expense tax collections) more than offset the drop. Regular general fund revenues are expected to increase going forward, but at a slower rate than the city experienced prior to the pandemic. Moreover, the April 2022 revenue forecast was higher than the previous forecast.

Despite the fact that general fund revenues are growing, the Seattle Times quotes officials calling for new revenue. For example, “Though the mayor’s office is in the early stages of forming its budget, which will be presented to City Council for approval in September, the administration is looking to find new revenue rather than slash existing spending.”

Meanwhile, according to the Times,

But another large part of making 2023 work will likely be asking the council to free up money earmarked for specific causes — like the Jumpstart tax — to cover general expenditures. Under the tax, businesses with at least $7 million in annual payroll are taxed on salaries paid to Seattle employees who make at least $150,000 per year. It generated $231 million in 2021.

The $231 million was a preliminary figure. The city ultimately collected $248.1 million from the Jumpstart tax (the payroll expense tax) in 2021, and the April 2022 forecast estimates that payroll expense tax revenues will increase to $277.5 million in 2022. If the payroll expense tax revenues were returned to the general fund, operating surpluses would be expected going forward. (For that analysis, I included general fund and payroll expense tax revenues and planned expenditures for both sources, from the financial plans in the 2022 adopted budget.)

Seattle’s revenues have increased significantly in recent years (due to both economic growth and the implementation of new taxes). It is fair to say, as Councilmember Pedersen said in an April meeting, that “Seattle does not have a revenue problem, but we potentially have an expenditure problem.”

Indeed, a general budgeting best practice is to avoid using one-time funds for ongoing programs. Seattle seems to have fallen into that trap. The Times quotes Ben Noble, the director of the city’s Office of Economic and Revenue Forecasts, about Seattle’s use of one-time federal funds:

“As much as it helped in those years, the pandemic funds in some ways exacerbated this pattern of ‘Oh, we have some one-time money, we’re going to invest in an ongoing thing,’” Noble said, noting increased spending on housing and homelessness prioritized by the council and a $100 million investment into BIPOC communities, committed by former Mayor Jenny Durkan without a funding source.

Resolving the operating deficit need not mean new revenues. As the Seattle Metropolitan Chamber of Commerce and Downtown Seattle Association wrote to the Seattle City Council earlier this month,

Categories: Budget , Tax Policy.Budgeting should start with a rigorous analysis of existing spending to determine if it is both effective and necessary – measured against the priorities for the city. Doing everything an institution has always done, at the same level, and then adding to it is both unsustainable and doesn’t recognize what’s happening in our communities.