10:11 am

January 19, 2023

SB 5286, which would make changes to the paid family and medical leave (PFML) rate structure, was approved by the Senate Labor & Commerce committee on Tuesday. The bill reflects the recommendations of the legislative task force on paid family and medical leave premiums, and it comes after multiple periods over the past year when the program experienced cash deficits. (We wrote in depth about the program’s financial problems here.) To ensure that the program is not in deficit at the end of the biennium, the 2022 supplemental appropriated $350 million from the general fund–state (GFS) to the family and medical leave insurance (FMLI) account. (These funds may only be used to the extent they are necessary to keep the account out of deficit.)

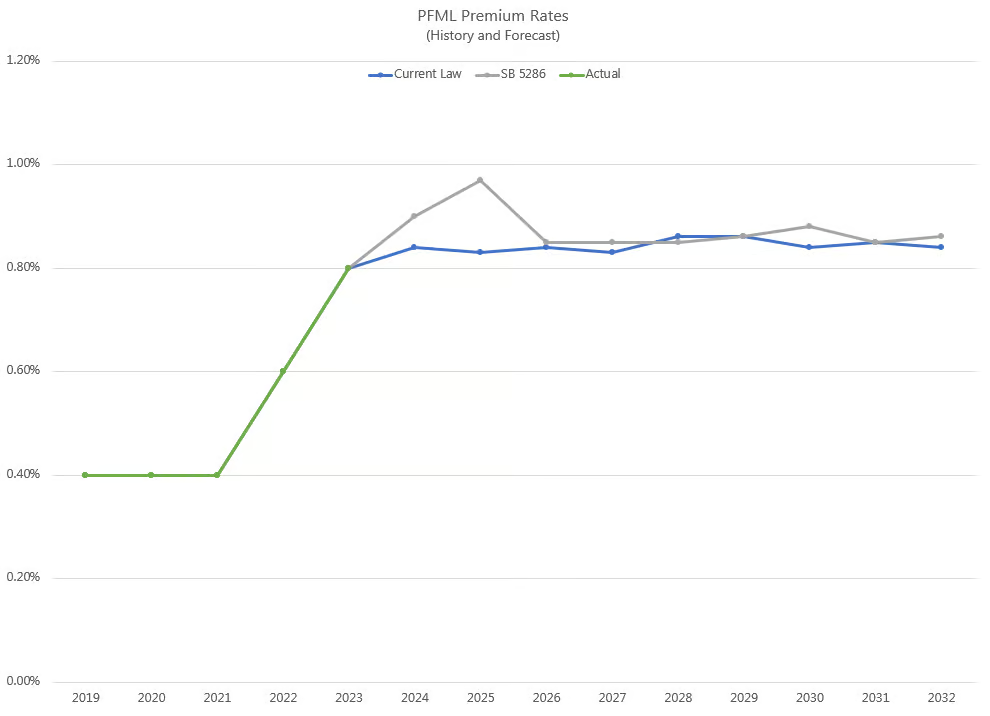

Currently the PFML premium rate is based on the FMLI account balance ratio on Sept. 30. The ratio is determined by dividing the FMLI account balance by total covered wages. The maximum regular rate is 0.6%, but solvency surcharges of up to 0.6% may be added, for a maximum of 1.2%. The 2023 rate is 0.8%. No program reserve is contemplated under current law.

Under SB 5286, the premium rate would be calculated on Oct. 20. The rate calculation would take 140% of the prior fiscal year’s costs (benefits paid plus administrative costs), subtract the FMLI account balance, and divide by the prior fiscal year’s taxable wages.

Regardless of the calculated rate, the Employment Security Department commissioner would be required to set the rate “at the minimum rate necessary to close the rate collection year with a three-month reserve” and the maximum premium rate would be 1.2%. No additional solvency surcharges would be allowed. The three-month reserve is defined as average monthly expenses (including benefits paid and administrative costs) in the prior 12 months, multiplied by three.

As noted above, SB 5286 incorporates the December 2022 recommendations from the legislative task force. However, a key piece of the recommendations is left out of the policy bill, with the intent that it will be addressed in the budget. The task force had recommended the new rate calculation, and it recommended that if any of the $350 million is left over after covering any FMLI deficit, the remainder should be used to seed the new reserve. SB 5286 does not include any mention of the $350 million. During the Jan. 16 public hearing on the bill, Sen. Robinson said that seeding the reserve with that appropriation “will be done through the budget-writing process.” Note that Gov. Inslee’s 2023 supplemental budget proposal would reduce the $350 million set-aside to $80 million (and it made no mention of using the funds for a reserve).

The fiscal note for SB 5286 does not assume that any GFS money will be provided to seed the FMLI reserve. It notes,

As a result of this legislation, the premium rate in the first few years of enacting this bill will increase in order to build up the targeted 3-month reserve to help offset the high variability with regards to premium collections. The rate will then stabilize around 0.86% once the initial build of the 3-month reserve is achieved.

Indeed, the fiscal note estimates that the premium rate under the bill would increase to 0.9% in 2024 and 0.97% in 2025, before dropping to 0.85% in 2026. With these higher rates, premium collections would increase by $213.0 million in 2023–25 and by $264.0 million in 2025–27. The chart compares the fiscal note’s estimates of what the rates would be under current law and under SB 5286.

No fiscal analysis of the legislative task force’s final recommendation was presented at its last meeting or in the recommendations report, so it’s not clear what future premiums would look like under SB 5286 if seed money is provided from the GFS. If it is, the GFS funds would buy down the premium rate to an extent.

That said, rates would almost certainly still be higher than the current maximum regular rate of 0.6%. The legislative task force had considered other rate structure options, and all of them would have resulted in rates ranging from 0.68% to 0.84%—much higher than had been expected when the program was adopted.