12:24 pm

January 20, 2026

Last week, the Economic and Revenue Forecast Council (ERFC) met to approve a methodology for the official budget outlook based on Gov. Ferguson’s proposed 2026 supplemental. (The outlook itself will be presented and approved by the ERFC on Jan. 27.)

The first question staff had for the ERFC was about reversion assumptions. As the methodology memo notes, “reversions are the estimated appropriations that will be unspent and revert, making those amounts available for future appropriation.”

In practice, the outlooks include a line for reversions in each year. Reversions serve to reduce the estimated spending in that year and increase the estimated ending fund balance. As we have shown, appropriations in the 2025–27 budget exceeded resources, so the budget only balanced because it assumed an unusually high level of reversions.

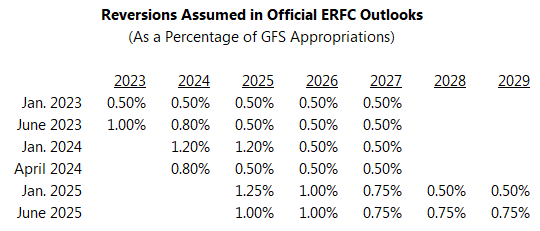

The question about reversions at the ERFC meeting was fairly contentious. Beginning in 2016, the outlooks have assumed that reversions will be 0.5% of general fund–state (GFS) appropriations, and they may additionally include as reversions amounts agencies have been directed to hold in unallotted status (see here and here).

The 0.5% assumption held until 2023. As shown in a staff analysis of reversion history, the level of actual reversions (as a percent of GFS) was extraordinarily high in 2020 (2.2%), 2021 (1.6%), 2022 (1.6%), and 2023 (2.5%). During those years there was an influx of federal relief funding that supplanted state funds and state spending restrictions were in place. Actual reversions have declined since then, to 1.2% in 2024 and 0.9% in 2025.

In 2023, the official outlook based on the enacted budget assumed reversions of 1% in 2023, 0.8% in 2024, and 0.5% thereafter. Since then, not only has the assumption varied from one year to the next, budget proposals from the governor and the Legislature have not agreed on the reversion assumption. The table shows how the assumption has changed with each new outlook. (Again, the larger the reversion amount, the higher the appropriations level can be while still balancing.)

Gov. Ferguson’s 2026 supplemental proposal assumes that reversions are 1% in each year going forward. (Recall that actual reversions in 2025 were 0.9%.) At the meeting last week, the ERFC decided that staff should prepare the official outlook based on the governor’s budget using a 1% assumption for 2026 and 0.9% thereafter.

During the meeting, some ERFC members argued that the official outlook’s assumptions should match the assumptions in the governor’s budget. Others argued that the official outlook should follow the assumptions set for the enacted 2025–27 biennial budget. Both sides argued that their position would be less confusing for the public. (They ended up going with a third option.)

This might seem like an arcane topic. (As OFM Director Chapman-See said, “I can’t recall an instance in which a member of the public has ever asked me a question about reversions.”) However, the reversion assumption can be the difference between the budget balancing or not. The assumption used also factors in to any calculation of the size of a budget shortfall. Thus, if different groups assume different reversions, their shortfall estimates will be different. And that really is confusing for the public.

Ultimately, I wonder whether Washington should be including reversions in the outlook at all.

Reversions were not included in state general fund balance sheets before 2012. In 2012, the Legislature was still facing Great Recession-era budget shortfalls. Part of the solution was to retain “in the general fund an estimated $160 million in projected agency reversions during 2011-13 biennium rather than distributing those reversions to other accounts.”

The November 2012 outlook methodology noted that the 2012 budget “made changes to the way agency underspending is handled. Rather than being distributed to the Education Savings Account, Savings Incentive Account, and various other smaller accounts, the amounts that remain unspent at the end of fiscal years 2012 and 2013 will be retained in the state general fund.” However, that outlook did not assume any future reversions. Beginning with the July 2013 outlook, future reversions have been assumed.

Regularly changing the assumed reversions allows the governor and the Legislature to game the budget, and it could be a self-fulfilling prophecy. First, they can adopt an appropriations level that is not supported by revenues and make up the difference with the reversion assumption. Then, because agency spending cannot exceed resources, they potentially create increasing levels of actual reversions, which can then used to justify higher reversion assumptions in the future.

Categories: Budget.