9:18 am

April 23, 2021

The Legislature has passed ESHB 1297. As passed, a working families’ tax exemption will be provided for certain individuals for sales taxes paid after Jan. 1, 2022. (The first payments will be made in FY 2023.) Individuals are eligible if they are also eligible for the federal earned income tax credit (or would qualify for the earned income tax credit if they had a social security number) and lived in Washington for more than 180 days in the year they claim the credit.

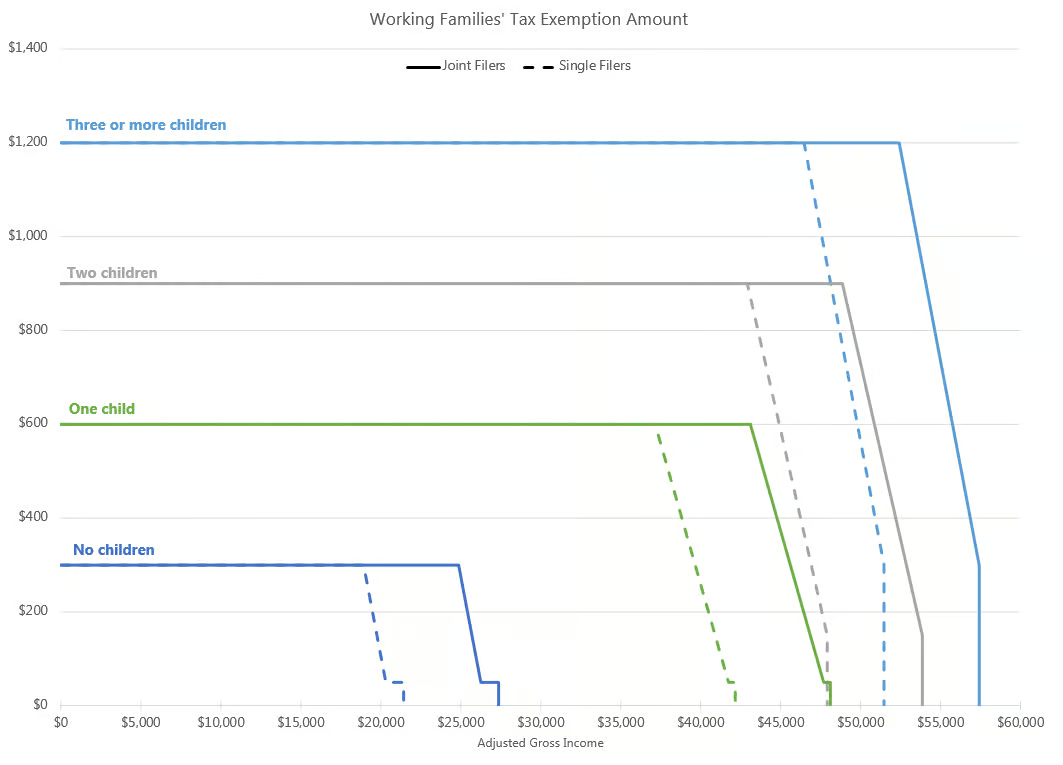

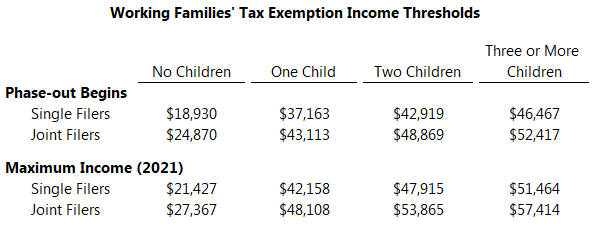

The remittance amount will be subject to a phase-out, but the maximum amounts are:

- $300 if the individual has no children,

- $600 if the individual has one child,

- $900 if the individual has two children, or

- $1,200 if the individual has three or more children.

The minimum amount is $50 a year. The phase-outs are as follows:

- By 18% per additional dollar of income beginning at $2,500 below the federal phase-out for individuals with no children,

- By 12% per additional dollar beginning at $5,000 below the federal phase-out for individuals with one child,

- By 15% per additional dollar beginning at $5,000 below the federal phase-out for individuals with two children, and

- By 18% per additional dollar beginning at $5,000 below the federal phase-out for individuals with three or more children.

Remittance amounts will be adjusted for inflation annually. The chart shows how the phase down of the exemption will work (if my calculations are correct). For example, a single filer with no children will receive $300 until his income reaches $18,930. At that point, the remittance begins to phase out until the filer’s income reaches $21,427, which is the current maximum income to qualify for the federal earned income tax credit (as expanded by the American Rescue Plan Act this year).

The working families’ tax exemption is already established in statute (RCW 82.08.0206). (It was passed in 2008 but never funded.) Compared to current law, ESHB 1297 makes individuals without social security numbers eligible, changes the remittance amounts, and adds phase-outs. The bill repeals the current requirement that the exemption must be approved by the Legislature in the operating budget before it can be claimed. Additionally, the bill removes the requirement that claimants have actually paid sales tax.

There is not yet a fiscal note for the version of the bill that passed the Legislature. Both the House- and Senate-passed operating budgets would appropriate $268.2 million for the working families’ tax exemption in 2021–23. Of that funding, $142.2 million would come from the general fund–state and $126.0 million would come from the taxpayer fairness account. The taxpayer fairness account was expected to be the recipient of some revenues from the proposed capital gains tax (as passed by the Senate in March). However, as Kriss noted yesterday, the version of the capital gains tax bill that was passed by the House this week would dedicate all revenues to the education legacy trust account. If that change holds, the Legislature will have to find $126 million from another source to fully fund the working families’ tax exemption.

Categories: Budget , Tax Policy.