1:01 pm

January 8, 2026

Gov. Ferguson’s 2026 supplemental operating budget proposal would shift funding for working families tax credit (WFTC) remittances from the general fund–state (GFS, which is a fund subject to the outlook) to the climate commitment account (CCA) for 2025–27. Although the WFTC is an allowable use of the CCA (RCW 70A.65.260(1)(a)), making the shift would mean that an ongoing program would be funded with one-time money.

As we have shown, using one-time money for ongoing programs is one of the causes of the recent budget shortfalls.

The governor’s proposal would reduce GFS appropriations for WFTC remittances by $498.0 million and increase CCA appropriations for them by $569.0 million. (As I noted Tuesday, there is a total increase in spending on the WFTC of $71.0 million, but it’s not clear what the policy change is. It’s possible it is a caseload change that should be classified as maintenance level.) The budget documents explicitly state that this would be a one-time shift of funds, which means that the cost of the WFTC would return to the GFS in 2027–29.

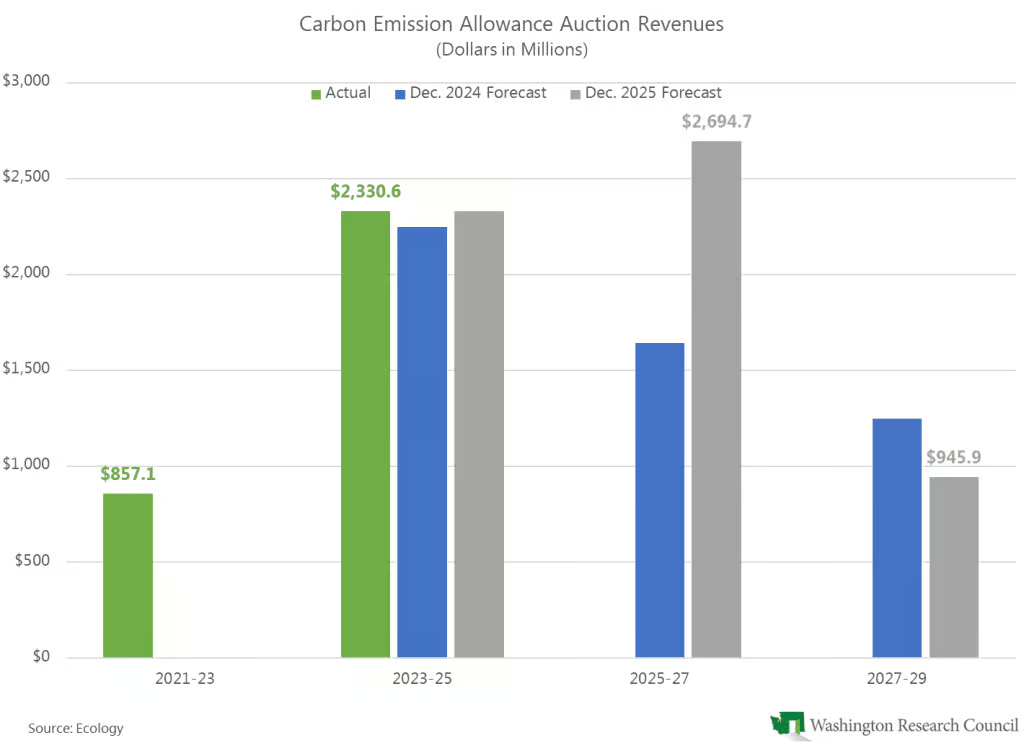

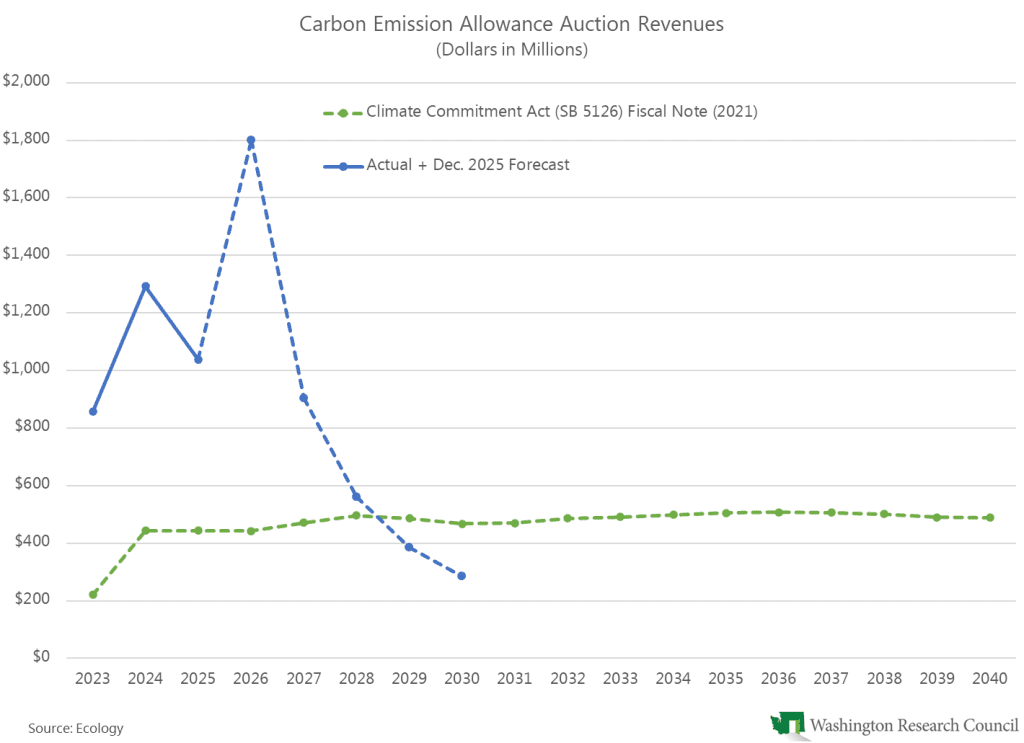

Indeed, given the Department of Ecology’s December 2025 forecast of carbon emission allowance auction revenues, using the CCA for the WFTC would not be an option after 2025–27.

By statute, the carbon emission reduction account (CERA), which is dedicated to the transportation budget, must receive the first $359.1 million of auction revenue each year through 2037. (The 2022 Move Ahead WA transportation revenue package relies on these auction revenues.) Any remaining revenues are deposited in the climate investment account (CIA, appropriated in the operating and capital budgets) and, to a much lesser extent, the air quality and health disparities improvement account (AQHDIA, appropriated in the capital and transportation budgets). Of the revenues to the CIA, 75% are distributed to the CCA and 25% are distributed to the natural climate solutions account (NCSA).

Compared to the December 2024 auction revenue forecast (on which the 2025 budgets were based), the December 2025 forecast increased revenues by $82.5 million in 2023–25 and by $1.052 billion in 2025–27. But estimated revenues for 2027–29 decreased by $302.1 million compared to the 2024 forecast. This means that the Legislature has a substantial amount of new revenue to appropriate this year. However, the Legislature will have less than previously expected for 2027–29.

Further, in FY 2030 (the first year of 2029–31, and the final year in the current forecast), Ecology expects revenues to drop to $285.4 million. Consequently, the transportation budget would not get its full share, and there would be nothing at all for the operating and capital budgets. (The Nov. 2025 transportation revenue forecast took this partially into account, but the FY 2030 revenue estimate has decreased since then.)

According to the forecast, “While higher allowance prices increase near-term revenue, longer-term revenue expectations are moderated by a declining supply of state-owned allowances available for auction in later years, largely due to an increase in expected no-cost allowance allocation to electric utilities and industrial EITE entities.” (Emphasis in original.)

Meanwhile, HB 2251 was pre-filed on Monday. The bill would change how the auction revenues are distributed. First, it would create new accounts. The CIA, CCA, and NCSA would be replaced with the climate commitment act operating account and the climate commitment act capital account. (Allowable uses would be very similar to the current allowable uses of the CIA, CCA, and NCSA—including the working families tax credit.)

Second, CERA would no longer be guaranteed the first $359.1 million of auction revenues. If annual revenue is expected to be $513.1 million or more:

- $359.1 million would be deposited in the CERA,

- $144.0 million would be deposited in the climate commitment act operating account,

- $10.0 million would be deposited in the AQHDIA, and

- the remainder would be deposited in the climate commitment act capital account.

If annual revenue is expected to be less than $513.1 million, the first $25.0 million would be deposited in the climate commitment act operating account (adjusted annually by the average growth in state personal income over the prior 10 years). Of the remaining revenues,

- 50% would be deposited in the CERA,

- 32% would be deposited in the climate commitment act capital account,

- 17% would be deposited in the climate commitment act operating account, and

- 1% would be deposited in the AQHDIA.

Under the Dec. 2025 revenue forecast, revenue is expected to be less than $513.1 million beginning in FY 2029. But note that the allowance auctions are still relatively new, so there is considerable uncertainty in the revenue forecast.

Categories: Budget , Energy & Natural Resources.Tags: Gov 2026