9:14 am

April 29, 2025

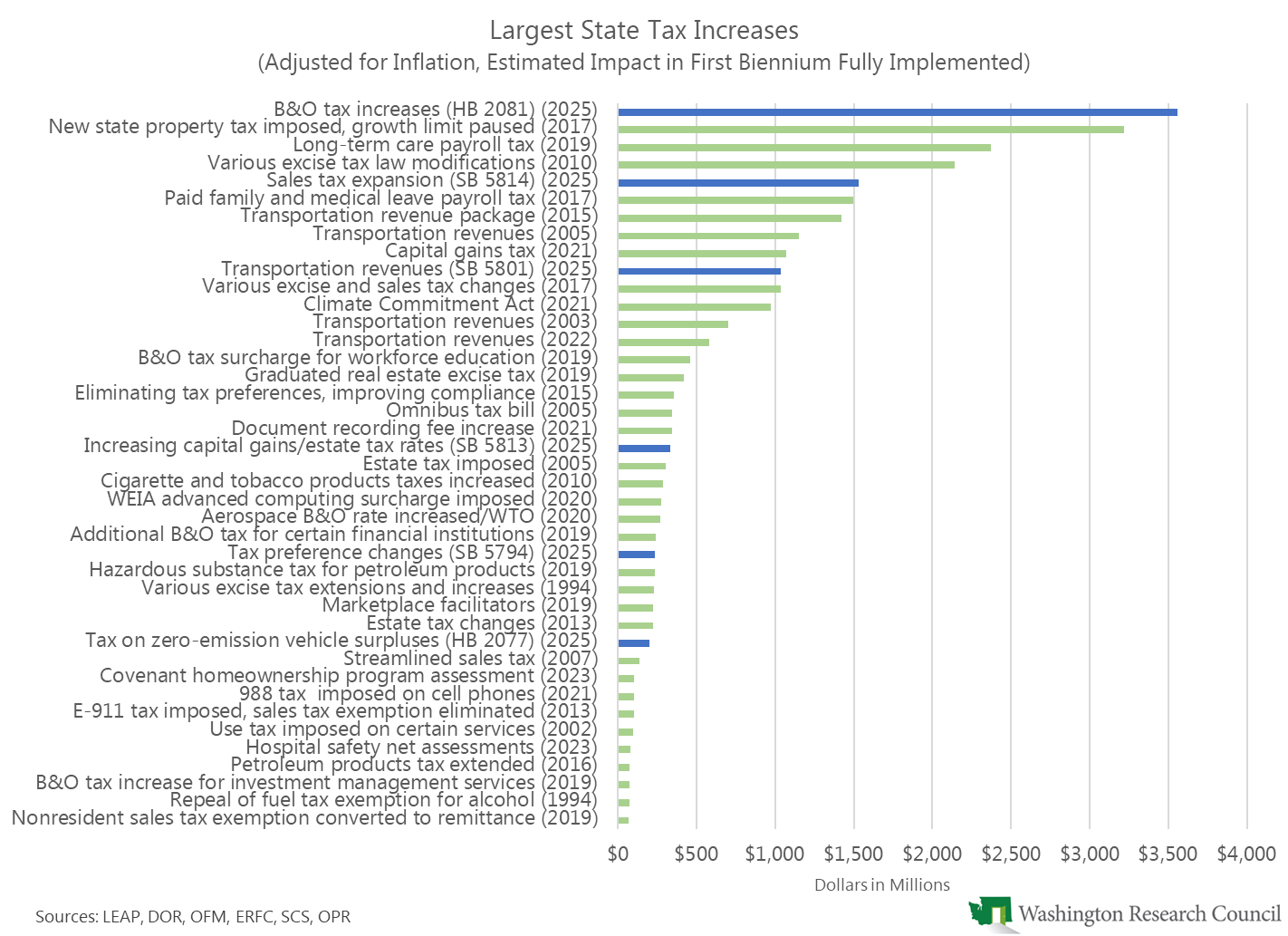

The operating budget, as passed by the Legislature, includes revenues from substantial new taxes. These taxes and the transportation revenue package would all make the list of the largest state tax increases.

As I noted over the weekend, the impact of these taxes to funds subject to the outlook (NGFO) is $9.379 billion over four years. However, the impact to taxpayers is higher, as not all the revenues from the taxes go to NGFO accounts. This is especially the case with SHB 2077, the tax on zero-emission vehicle program surpluses. The fiscal note for SHB 2077 estimates that it would increase total revenues over four years by $281 million. Of that, just $55 million would go to the NGFO. Unfortunately, there are not yet final fiscal notes for several of the other bills (and the budget documents only show the NGFO revenues). Assuming their impacts to non-NGFO accounts will be minimal, the impact of the operating budget tax package on taxpayers is about $9.6 billion over four years.

The chart below shows how these operating and transportation budget taxes compare to the state’s largest tax increases. (Note that there is not yet a final fiscal note for ESSB 5801, which increases transportation revenues. The budget documents include only the 6-year revenue impact, which is $3.208 billion. The fiscal note for an earlier version of the bill estimated that it would increase revenues by $2.951 billion over six years. The chart uses that fiscal note’s estimate for 2027–29.)

ESHB 2081, which both permanently increases business and occupation (B&O) tax rates and imposes a temporary tax surcharge on income over $250 million, is the largest tax increase going back over 30 years at least. (The taxes adopted this year are in blue in the chart.)

Additionally, I’ve put together a spreadsheet showing the potential impacts to B&O rates by industry from ESHB 2081 and ESSB 5794, which would apply or increase the B&O tax to various industries that currently receive tax preferences. (That’s the state’s terminology for exemptions, exclusions, deductions, deferrals, credits, and preferential tax rates. Many preferences are in place for important tax policy reasons.) There are interactions between the bills, and the language in ESHB 2081 is unclear as to exactly which activities are exempt from the temporary surcharge. The rate changes shown in the spreadsheet represent my reading of the bills; the Department of Revenue could come to different conclusions.

As the spreadsheet shows, ESHB 2081 and ESSB 5794 would increase B&O rates for some industries by over 300%.