9:14 am

November 25, 2019

The Senate Higher Education & Workforce Development Committee’s work session on Thursday included presentations on the workforce education investment act (E2SHB 2158) that was enacted earlier this year. As I wrote last week, a staff presentation at the Senate Ways & Means Committee’s work session included a concern about a reduced 2021–23 revenue estimate for the bill and how that would affect the budget. It also appears that there is a shortfall in the new workforce education investment account (WEIA) in 2019–21.

E2SHB 2158 imposed a 20 percent business and occupation tax surcharge for certain businesses in the “other business or service activities” category (see our report on 2019 revenue legislation for more details). The bill set up a new, dedicated account (the WEIA) to hold the collections from the surcharge. It also made 2019–21 appropriations ($374.7 million) from the new account—mostly for higher education programs.

Higher Education & Workforce Development Committee staff provided an updated fiscal summary of the bill for the committee. It itemizes the appropriations made from the account for 2019–21 and notes that, under E2SHB 2158, the Washington College Grant (formerly the State Need Grant) becomes an entitlement in FY 2021. This means that as caseloads change, spending for the program must as well. Based on the preliminary maintenance level estimates from the Office of Financial Management, staff expects the cost of the grant to increase by $28.1 million in FY 2021. Assuming that, 2019–21 appropriations from the WEIA will be $402.7 million, but estimated revenues to the account are just $380.0 million, leaving a 2019–21 shortfall of $22.7 million.

Additionally, the Higher Ed work session included a presentation from the Department of Revenue (DOR) about the revenue collections under the bill. (In the TVW video, DOR’s presentation begins here.)

When the Legislature passed the bill in April, it was expected to increase revenues by $380 million in 2019–21 and $565.7 million in 2021–23. But an amendment was adopted the day of passage that ultimately reduced the fiscal estimate for 2021–23 to $393.2 million.

Section 74 of the bill states, “The legislature intends the provisions of this act to be applied broadly in favor of application of the surcharges.” The amendment made the “rule of statutory construction in favor of the application of the surcharge” effective only through Dec. 31, 2021. The new fiscal note calls this a “heightened standard of proof under which the Department’s determination that a business is subject to the surcharge is presumed to be correct unless the business shows by clear, cogent, and convincing evidence that the Department’s determination was incorrect.”

Because the amendment set an expiration date for this unusual standard, the fiscal note expects “reduced compliance and the possibility of refunds starting in Fiscal Year 2022” and assumes that compliance will be 90 percent in FY 2020, 95 percent in FY 2021, and 75 percent thereafter. DOR also expects refund requests for taxes paid in FY 2020 and 2021 beginning Jan. 1, 2022 and assumes that “refunds will be issued for approximately 20 percent of amounts paid during Fiscal Years 2020 and 2021.” Hence the reduced revenue estimate for 2021–23.

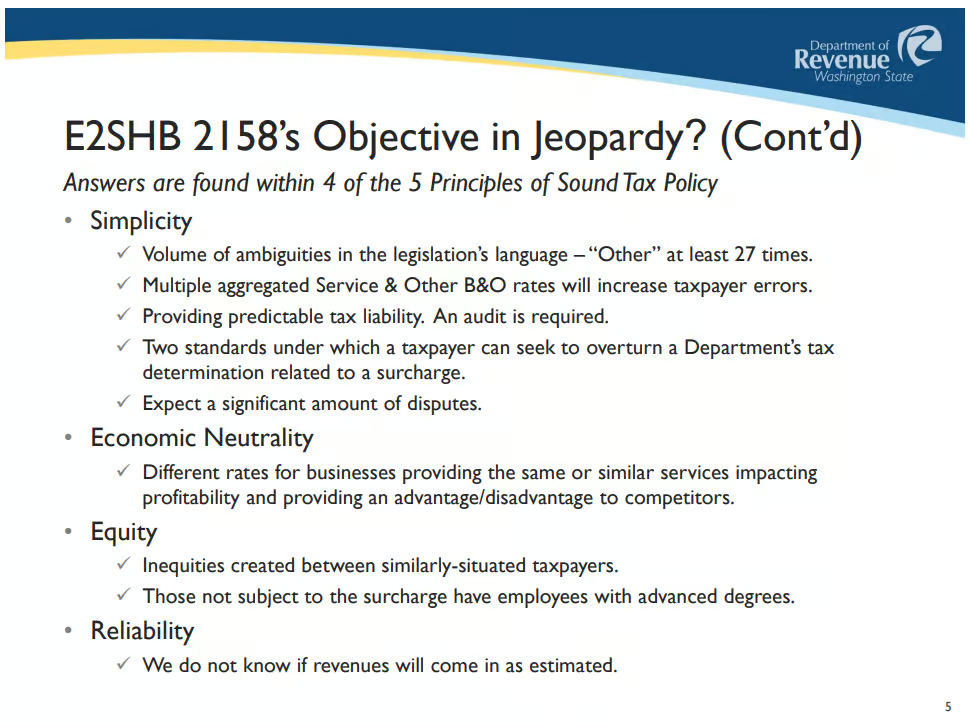

David Duvall of DOR told the committee that the department will be ready for the first returns (due Feb. 25, 2020), but the “[s]ignificant volume of ambiguity in the bill jeopardizes the Department’s ability to administer and taxpayer’s ability to comply.” Here’s a slide from his presentation on how the bill stacks up on principles of sound tax policy:

Duvall said, “Altogether, what this means is that we have doubts about actually collecting revenues as estimated. . . . While these are significant challenges, the Department will do its best, but it’s going to be messy and there will be disputes.”

He asked, too, if the revenues anticipated by the bill will be sufficient to fund appropriations—appropriated and planned appropriations over four years from the WEIA total $937.1 million but expected revenues over four years are $773.1 million. Duvall said, “In essence, 2158 is self-contained and, as such, needs to be self-sustaining to ensure there are adequate resources to cover the appropriations.” According to Duvall, the funding gap and ambiguity in the bill raise “the question of whether Section 74 can fund what it was meant to fund.”

Anticipating some of these issues, the Economic and Revenue Forecast Council decided in June to forecast revenues from the surcharge in order to better assist legislators making appropriations from the WEIA.

Categories: Budget , Categories , Education , Tax Policy.