1:35 pm

November 21, 2019

As Kriss noted, the Economic and Revenue Forecast Council (ERFC) adopted a new revenue forecast yesterday. The ERFC also adopted a new budget outlook.

The June outlook, which was based on the 2019–21 enacted budget and vetoes (and the March revenue forecast), estimated that the unrestricted ending fund balance was $372 million in 2019–21 and negative $58 million in 2021–23.

The November outlook has improved: the estimated unrestricted ending fund balance is now $802 million in 2019–21 and $383 million in 2021–23. The improvement is due to the increased revenue forecast. With yesterday’s forecast, revenues for 2019–21 are expected to increase by 12.3 percent and revenues for 2021–23 are expected to increase by 6.6 percent. (And those significant increases are on top of an 18.0 percent increase in 2017–19.) No extraordinary revenue growth is expected for either biennium.

The outlook includes a preliminary estimate of maintenance level spending (the cost of continuing current services) from the Office of Financial Management (OFM). OFM currently estimates a maintenance level increase of $517 million over enacted appropriations in 2019–21 and $386 million in 2021–23.

In addition to the surpluses now expected in each biennium, the outlook estimates that the budget stabilization account (BSA, or the rainy day fund) balance will be $2.175 billion in 2019–21 and $2.808 billion in 2021–23. (The BSA account balance at the end of 2017–19 was $1.618 billion.)

Kriss also discussed the ERFC’s pessimistic revenue scenario, writing that Gov. Inslee should propose a 2020 supplemental budget “that preserves a healthy four-year reserve.” That’s always a good idea. More reasons for caution were discussed at a Ways and Means Committee work session yesterday, related to revenue bills enacted earlier this year:

- A lawsuit has been filed regarding the constitutionality of SHB 2167 (which imposed an additional 1.2 percent business and occupation tax on certain financial institutions). The new tax was expected to increase revenues by $133.2 million in 2019–21 and $205.6 million in 2021–23. If it is found to be unconstitutional, those revenues would not be realized.

- The revenue estimate for E2SHB 2158 (which imposed a business and occupation tax surcharge on certain businesses to fund higher education) was reduced by $172.5 million in 2021–23 after the bill was passed by the Legislature (but before it was signed by the governor in May). (Our report on the revenue changes made during the session includes the current number.)

- The new tax on vapor products (E2SHB 1873) was expected to increase revenues to funds subject to the outlook (NGFO) by $1.4 million in 2019–21 and $1.5 million in 2021–23. (Another $17.7 million in 2019–21 and $33.5 million in 2021–23 were expected in non-NGFO accounts.) But in September, the State Board of Health banned flavored vapor products for 120 days (and that emergency rule was later expanded to include a ban on vapor products containing vitamin E acetate). According to Ways and Means staff, a new fiscal estimate assumes the flavor ban will become permanent and that health concerns will continue to dampen the market for the products, meaning that “over 95 percent” of the four-year estimate is now not expected to be collected.

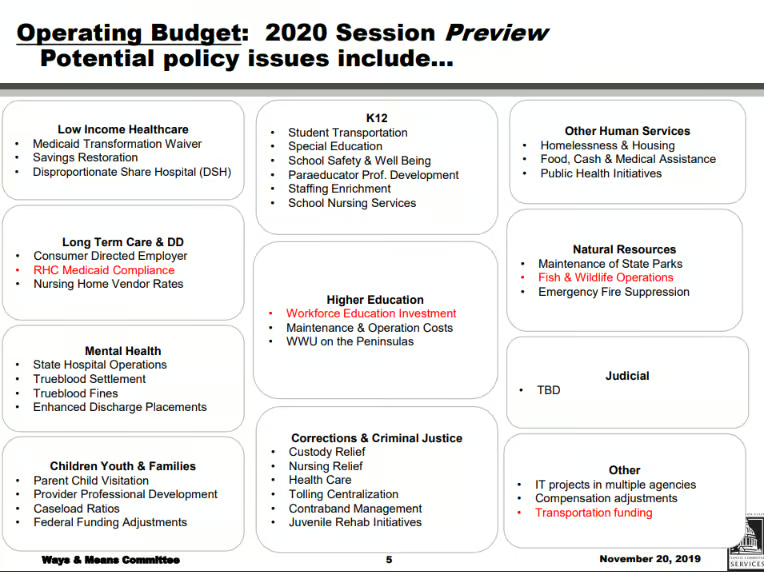

Additionally, the slide below (from the Ways and Means staff presentation) provides a preview of policy issues that may be important in the upcoming session.