12:55 pm

March 11, 2026

The conference committee’s operating budget proposal relies heavily on one-time resources, questionable accounting assumptions, and the new income tax.

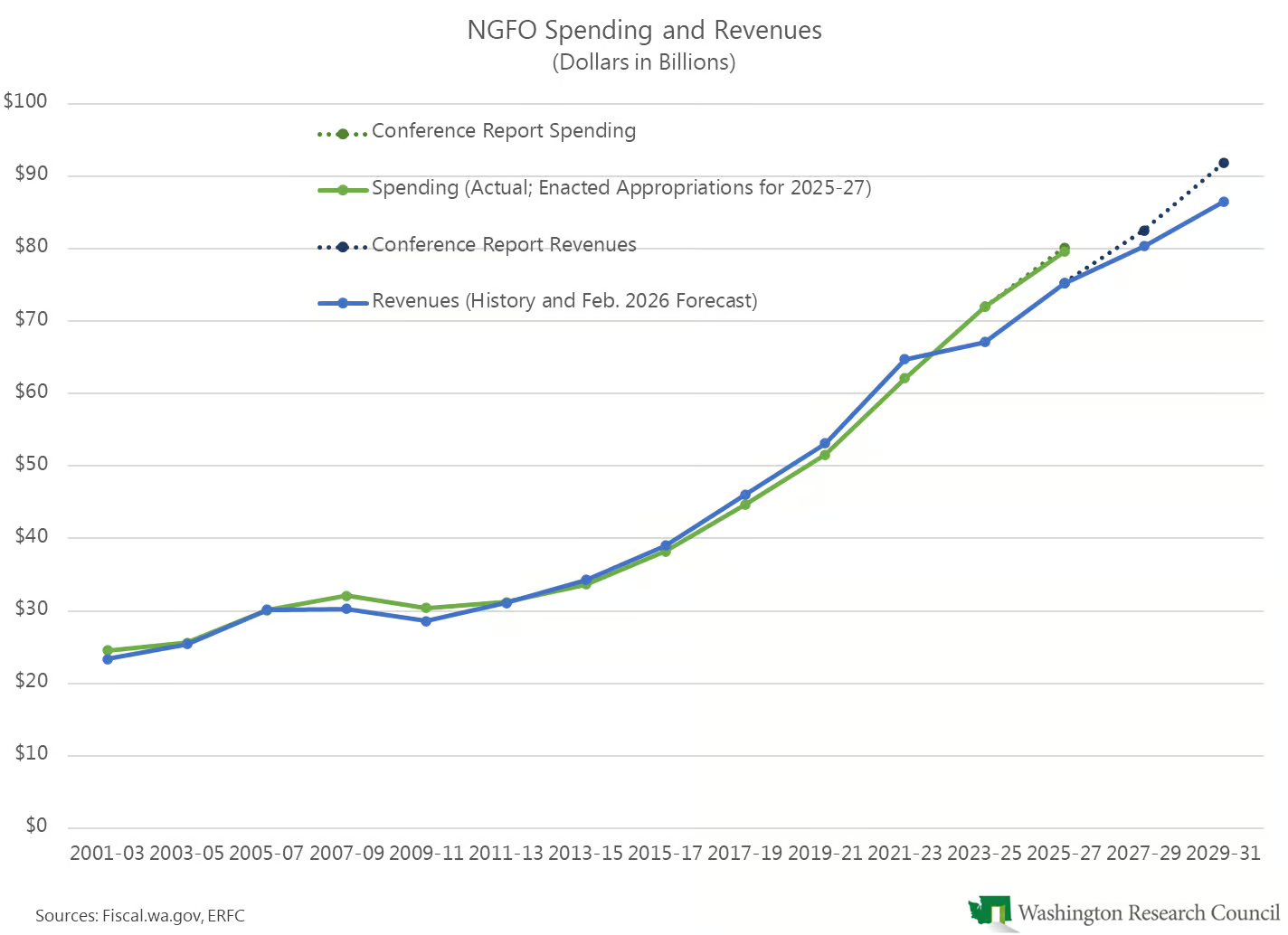

The proposal would increase appropriations from funds subject to the outlook (NGFO) by $2.348 billion (3.0%) over enacted 2025–27 appropriations. Revised 2025–27 appropriations would be $80.206 billion, which would be 11.4% higher than actual 2023–25 spending. This level of appropriations would be higher than in either the House- or Senate-passed budgets (by $272.3 million and $60.0 million, respectively).

Of the increase, $1.727 billion is at the maintenance level (the cost of continuing current services, adjusted for enrollment and inflation) and $621 million is net new policy.

Major tax changes included in the proposal include:

- SB 6346, which would impose an income tax. This would reduce revenues by $55.4 million in 2025–27 and increase revenues by $2.292 billion in 2027–29. The revenues assumed in the proposal reflect the fiscal note for Rep. Berg’s striking amendment. That version of the bill was passed by the House yesterday, but there were additional floor amendments that are not included in the fiscal estimate. Some of these will reduce the revenues assumed in the budget.

- SB 6231, which would apply the sales tax to data center refurbishments. This would increase revenues by $63.0 million in 2025–27 and $140.5 million in 2027–29.

- SB 6228, which would increase business and occupation (B&O) taxes for prescription drug warehousing and reselling. This would increase revenues by $24.0 million in 2025–27 and $141.7 million in 2027–29.

- HB 2487, which would clarify that only entities paying the insurance premiums tax may claim a B&O exemption. This would increase revenues by $55.6 million in 2025–27 and $17.2 million in 2027–29.

- SB 6347, which would roll back the estate tax rate increases that were adopted last year. This would decrease revenues by $44.8 million in 2025–27 and $389.9 million in 2027–29. Importantly, the budget assumes the version of the bill that passed the Senate, meaning that the inflation-adjustment glitch remains fixed.

The proposal assumes substantial one-time resources. It would:

- Direct all capital gains revenues in 2025–27 to the NGFO. (Normally, to manage revenue volatility, the portion above $500 million a year goes to the common schools construction account.) This would increase NGFO revenues by $395 million in 2025–27.

- Transfer $880 million from the budget stabilization account (BSA, or the rainy day fund) to the NGFO in 2025–27 for general use. Another $141 million would be appropriated from the BSA for fire costs. (The proposal assumes that in FY 2029, $880 million would be transferred from the LEOFF 1 surplus to the BSA.)

- Transfer a net of $387.7 million from other accounts to the NGFO. This includes $375 million from the public works assistance account.

Additionally, this proposal balances thanks to unusual accounting assumptions. First, reversions (appropriations that are not ultimately spent) are assumed to be 1% of spending in FY 2026 and 0.9% thereafter. As I’ve written, this is the amount assumed in the official outlook for Gov. Ferguson’s proposal, but it is much higher than normal. Higher reversions mean larger ending balances.

Second, like the House-passed budget, the conference proposal assumes an unusually high level of prior period adjustments. Prior period adjustments are normally included in the outlook’s resources section to take actual experience into account. These adjustments are normally assumed to be $41 million a biennium. The conference report assumes they will be $250 million a biennium. This also has the effect of increasing the ending balances.

Given these assumptions, the conference report would leave an unrestricted NGFO ending balance of $231 million in 2025–27 and $563 million in 2027–29. (Note, though, that the ending balance in FY 2028 would be negative $878 million.) Total reserves would be 3.2% of revenues in 2025–27 and 7.8% of revenues in 2027–29. Appropriately, the second biennium does not assume 4.5% annual revenue growth, which would have provided $2.027 billion in phantom revenues.

This balance is extremely tenuous:

- Excluding the questionable accounting assumptions, the ending balance would be negative $786 million in 2025–27 and negative $1.472 billion in 2027–29.

- Even given the assumptions, the budget doesn’t balance in FY 2028.

- The four-year balance relies on the income tax revenues. The tax could be overturned by voters or the Supreme Court. Plus, as a new tax, collections could be quite different than anticipated.

- The 2027–29 ending balance is very low. It assumes that spending will grow by just 2.8% in that biennium compared to the proposed 2025–27 appropriations. Assuming the $563 million ending balance would be spent down, spending would grow by 3.5%. Washington hasn’t had biennial spending growth that low since the Great Recession. The estimated spending in the second biennium reflects the state’s best current estimate of how much appropriations in the budget proposal will cost in the next biennium. However, they are expressly not allowed to include any estimate of the cost of collective bargaining agreements that have not yet been approved. The CBAs with state and nonstate employees that are agreed to for 2027–29 will almost certainly cost more than $563 million.

As we have shown, the reason the state had a shortfall in 2025 and this year was that in 2023–25, the Legislature adopted budgets that increased appropriations by 15.8% at a time when revenues were expected to grow by just 3.5%. Actual spending in 2023–25 exceeded revenues by $4.842 billion. This budget proposal would widen that gap: appropriations for 2025–27 would exceed revenues by $4.894 billion.

If you believe that appropriations will only grow by 2.8% in 2027–29, then spending would be $103 million below revenues in 2027–29. But, as noted above, that seems unlikely. Average spending growth going back to 2003–05 is about 10.6%. If state spending is allowed to grow just at that average in 2027–29 and 2029–31, the gap between spending and revenues will continue to grow. The income tax as written does not solve the budget problem.

Tags: 2026 supplemental