9:33 am

March 4, 2026

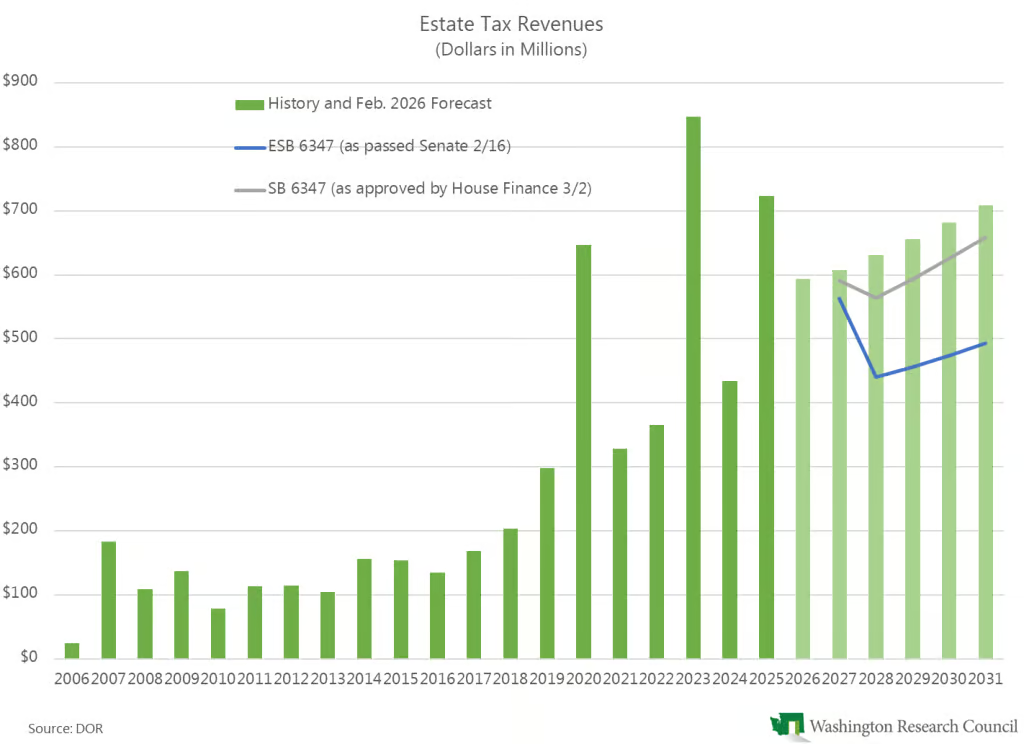

Last year the Legislature increased estate tax rates and fixed a long-term problem with the inflation adjustment for the exclusion amount (ESSB 5813). This year, the Senate has passed ESB 6347, which would roll back the tax rate increases in ESSB 5813. Beginning with estates of people dying on or after July 1, 2026, the tax rates would revert to the prior rates. For example, the top rate is currently 35%; it would revert to 20%.

This change would reduce revenues by $44.8 million in 2025–27 and $389.9 million in 2027–29. Both the Senate- and House-passed supplemental operating budgets assume this version of the bill and this revenue impact.

On Monday, the House Finance Committee approved a version of SB 6347 that would make the same rate changes and additionally undo the inflation adjustment change from ESSB 5813. Compared to current law, this version of the bill would reduce revenues by $17.3 million in 2025–27 and $129.0 million in 2027–29.

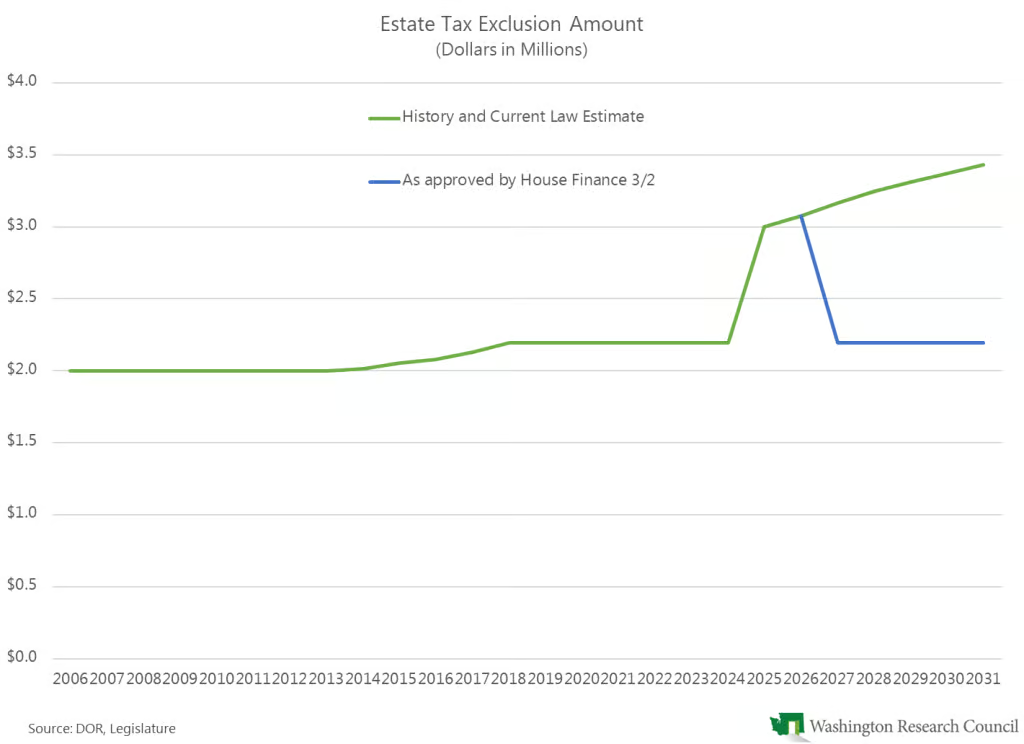

In 2013, the Legislature decided to adjust the estate tax exclusion annually for inflation. It specified that the inflation adjustment was the consumer price index for the Seattle-Tacoma-Bremerton metropolitan area, which was calculated by the U.S. Bureau of Labor Statistics (BLS) at the time. However, that index is no longer calculated by BLS. Consequently, the exclusion was stuck at $2.193 million beginning in 2018.

ESSB 5813 fixed the glitch by making the exclusion amount $3.0 million for estates of people dying between July 1, 2025 and Jan. 1, 2026 and then adjusting the amount annually using the consumer price index for the Seattle metropolitan area, meaning the area sample including Seattle and surrounding areas. This wording will allow the inflation adjustment to continue even if BLS changes the name of its sample for the area in the future.

The Finance version of SB 6347 would drop the exclusion amount back down to $2.193 million and again direct that the inflation adjustment is the consumer price index for the Seattle-Tacoma-Bremerton metropolitan area. Effectively, this means that there would never be an inflation adjustment to the exclusion amount.

If the Legislature decides to make a policy choice to keep the exclusion amount at $2.193 million permanently, it should remove reference to an inflation adjustment from statute. It should not return to statute a reference to an index that we know no longer exists.