11:34 am

April 21, 2025

We estimate that the maintenance level (the cost of continuing current services, adjusted for enrollment and inflation) shortfall is about $8.6 billion over the outlook period (FY 2025, 2025–27, and 2027–29).

The 2025–27 operating budget problem is not a revenue shortfall, it is the result of legislative spending choices over the past several years. Indeed, revenues for funds subject to the outlook (NGFO) are expected to increase by $4.5 billion from 2023–25 to 2025–27 and by $5.5 billion from 2025–27 to 2027–29. Nevertheless, the Legislature is proposing historically large tax increases.

These tax increases are not being proposed to avoid massive cuts to services.

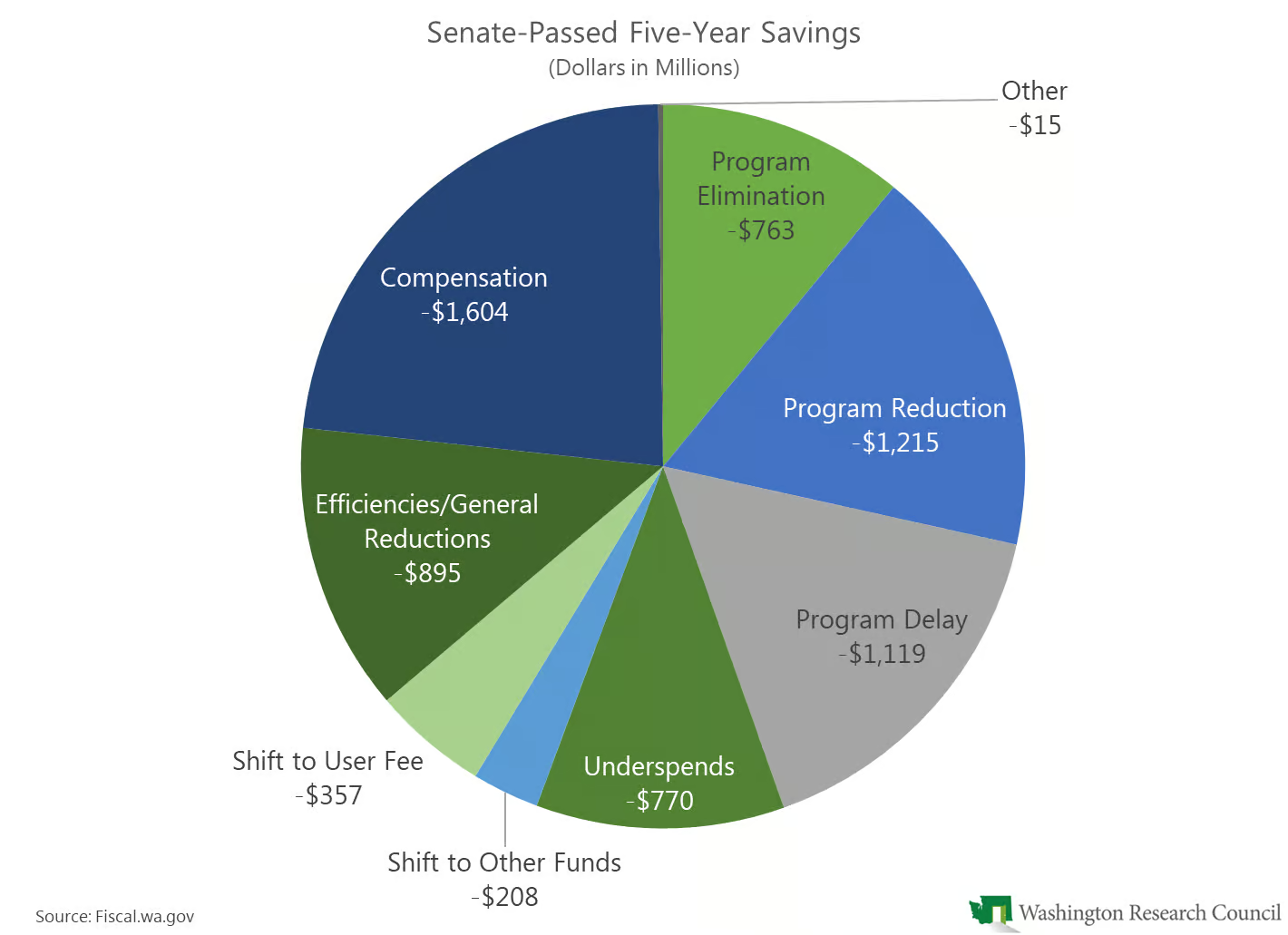

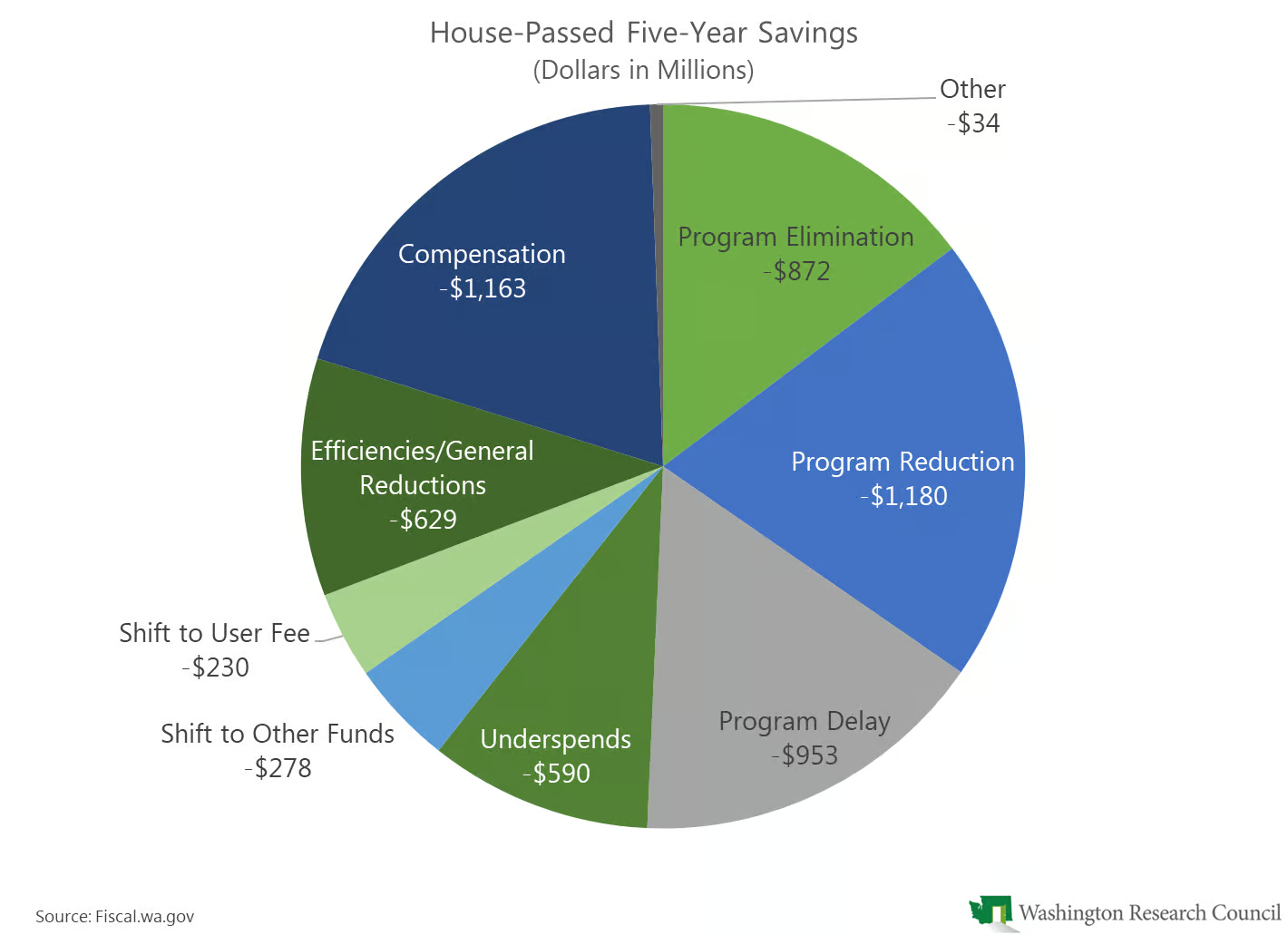

First, even with the tax package, both the Senate- and House-passed budgets assume budgetary savings. Over the outlook period, the Senate-passed budget assumes $6.946 billion in savings, and the House-passed budget assumes $5.928 billion in savings. Those savings would go a long way to addressing the shortfall.

However, both budgets would also add new policy spending over the outlook period: $10.4 billion in the Senate and $11.0 billion in the House. The net increase in spending would be $3.5 billion in the Senate and $5.1 billion in the House. It is mainly this net increase that “requires” the $13.4 billion tax package. The budget proposals do not propose raising taxes in lieu of cutting spending—they would do both. (I wrote about the major spending increases in 2025–27 here and the major savings items in 2025–27 here.)

Second, given the overall increase in spending, the proposed savings in the budgets reflect the trade-offs inherent in the budget process. The Legislature is signaling that it no longer prioritizes the programs it would reduce and prefers to fund the new policy increases instead. Additionally, many of the assumed savings are not actual reductions but shifts to the future or to other fund sources.

The charts below show the composition of the five-year savings in each budget. Actual cuts to programs (elimination or reductions) would account for about 28% of the Senate savings and 35% of the House savings. (Again, these cuts to programs represent a change in legislative priorities.) Other savings categories include program delays, compensation, general efficiencies, shifts out of the NGFO, and underspends (programs that didn’t require the level of appropriations they received).

Third, the size of the tax package is much larger than is necessary to fund even the proposed spending level.

Tags: 2025-27