12:21 pm

July 2, 2026

The Department of Revenue reported last month that capital gains tax collections for tax year 2025, which were collected in April and May 2026, totaled over $1.5 billion. (This is not the final number. All taxpayers must submit estimated payments in April, but taxpayers with filing extensions will finalize their payments in October 2026.)

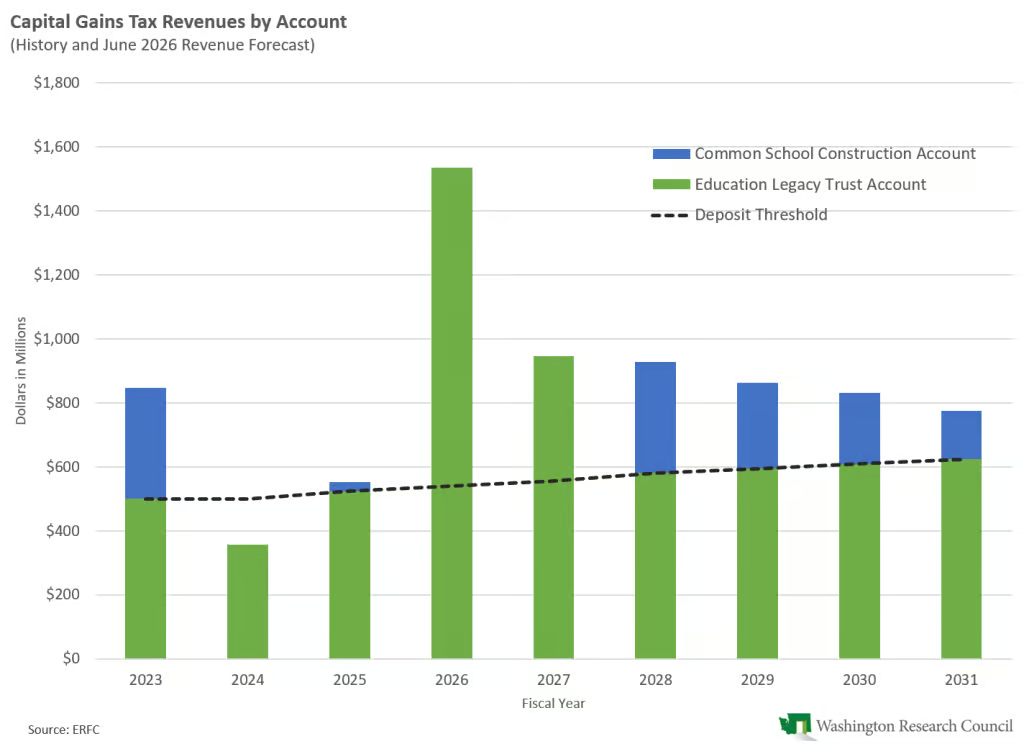

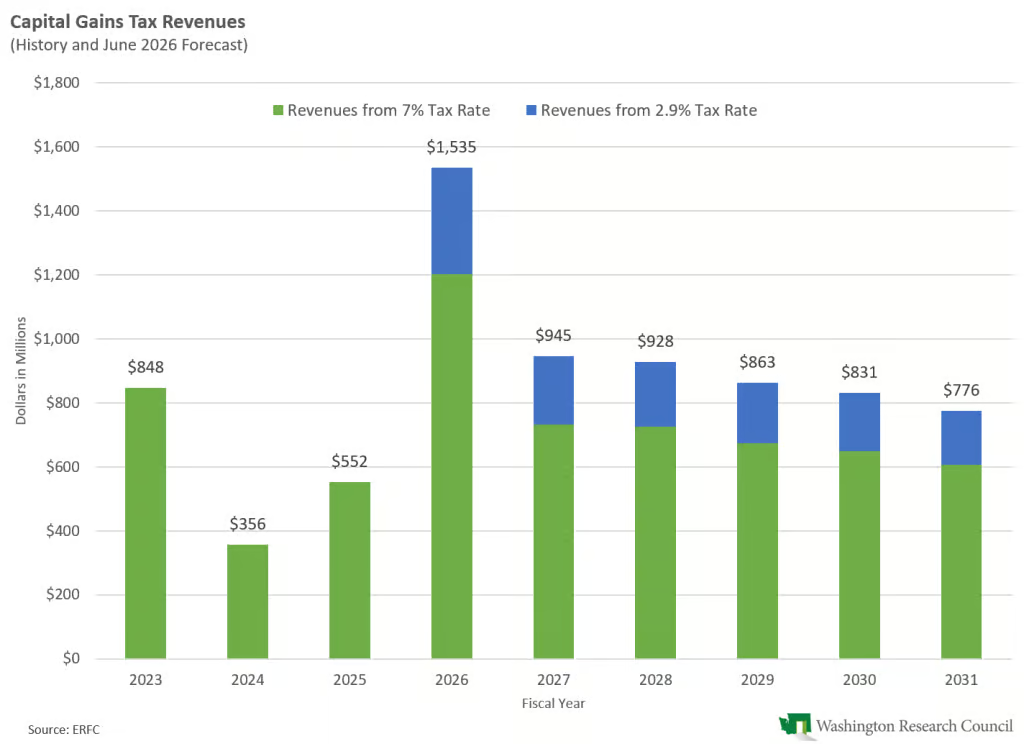

According to the Economic and Revenue Forecast Council (ERFC), capital gains tax revenues in fiscal year 2026 are estimated to total $1.535 billion. (FY 2026 includes final changes related to tax year 2024 and the initial collections for tax year 2025.) The FY 2026 estimate is 178% higher than FY 2025 collections.

Tax year 2025 is the first year in which there is an additional 2.9% tax rate on capital gains exceeding $1 million. (The tax rate is 7% for gains that are $1 million or less and 9.9% for gains that are over $1 million. The $1 million threshold is not adjusted for inflation.) The ERFC estimates that the additional 2.9% tax rate accounts for $331.9 million (21.6%) of total capital gains tax revenues in FY 2026.

It’s not clear why FY 2026 tax collections are so much higher than FY 2025 collections. The additional 2.9% tax is a part of the story, but revenues would have also increased significantly without it. Note that the 2025 increase to the capital gains tax rate was effective for tax year 2025, so taxpayers did not have an opportunity to realize gains before the tax took effect. It’s possible taxpayers delayed realizing gains in tax year 2024 in case the capital gains tax was repealed by I-2109 that year.

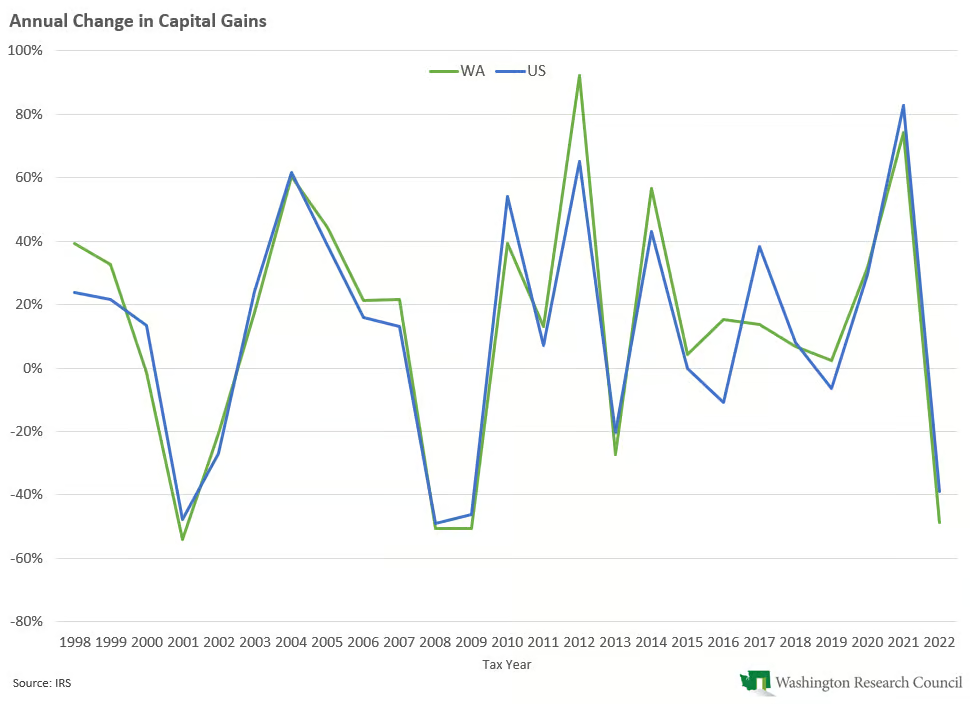

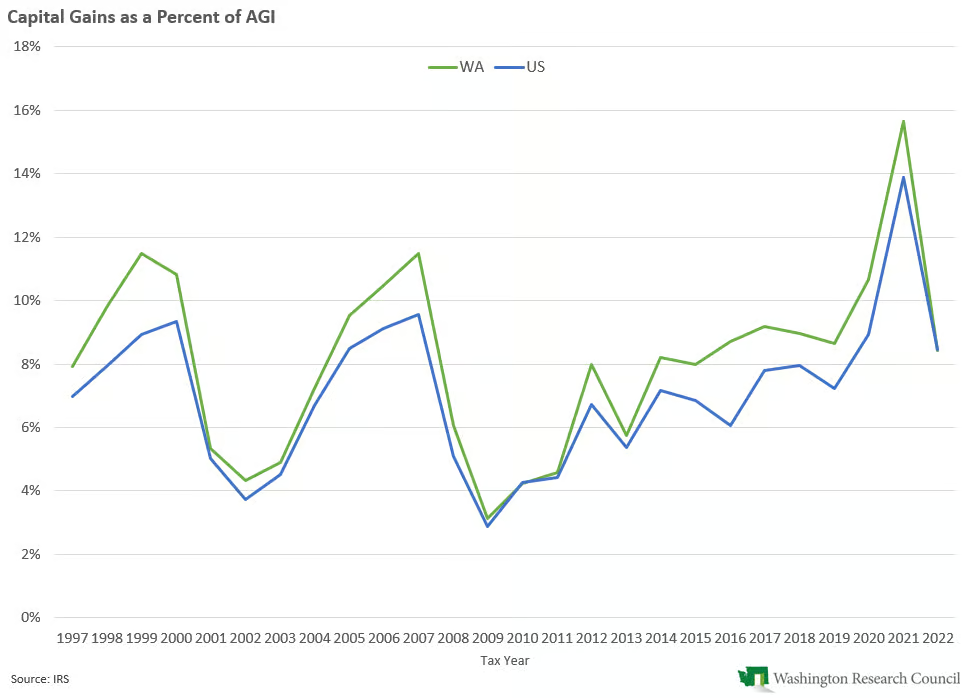

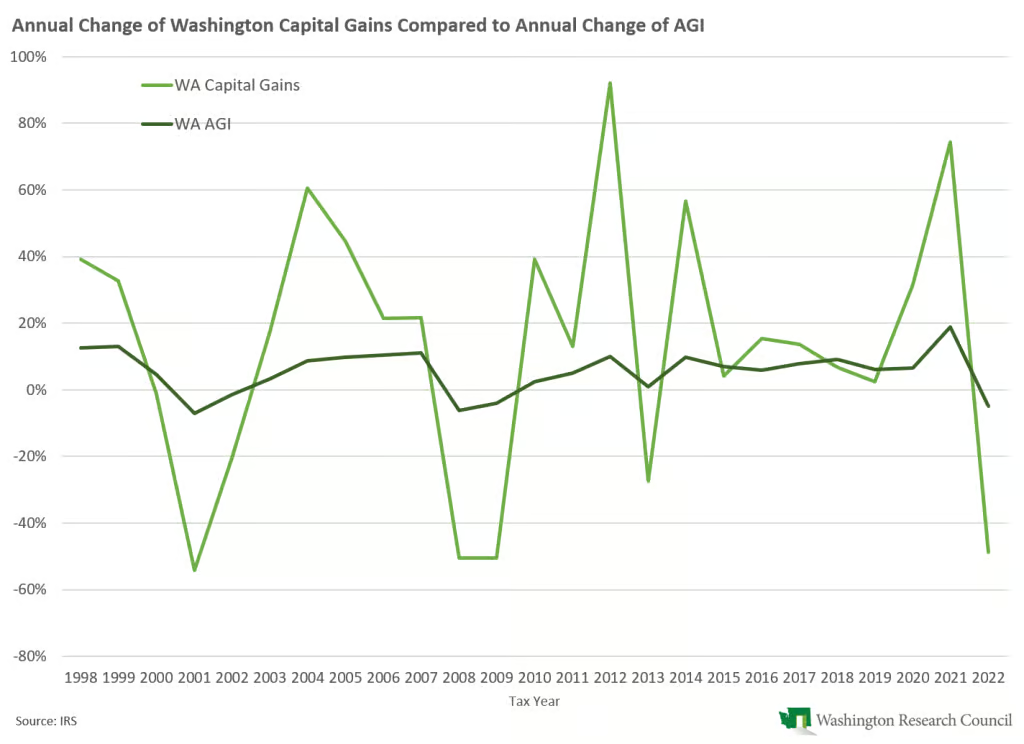

Historically, the annual change in capital gains realized by Washington residents has largely mirrored the annual change in U.S. realizations. However, capital gains of Washington residents as a percent of Washington adjusted gross income (AGI) has typically exceeded the capital gains share of U.S. AGI. (2022 is the most recent year of data, which was the first year of the Washington capital gains tax.)

Ultimately, capital gains taxes are very volatile, as capital gains realizations can depend on the stock market, expected changes in tax rates, and taxpayer behavior. The chart below shows the annual change of capital gains realizations (as reported on Washingtonians’ federal tax returns) compared to the annual change of total adjusted gross income of Washingtonians.

This volatility is visible in Washington capital gains tax collections in the four years the tax has been in place. When revenues are volatile, they are hard to forecast. Further, revenue volatility makes it harder to craft sustainable budgets. Revenues can be high one year and low the next; consequently, the more volatile overall revenues are, the more a state should keep in reserves.

Washington’s capital gains tax is mainly deposited in the education legacy trust account (ELTA). Although the ELTA is a fund subject to the outlook (NGFO), money in the ELTA does not feed into constitutionally-required transfers to the budget stabilization account. To help manage the volatility of the tax, the capital gains tax statute requires any collections over $500 million a year (adjusted for inflation) to be deposited in the common school construction account (CSCA). Thus, extraordinary revenues are used for one-time projects.

However, the 2026 supplemental operating budget temporarily changed the statute to keep all capital gains tax revenues in the ELTA for 2025–27. This means that there is an estimated $1.385 billion that will stay in the ELTA (to be used for ongoing spending) rather than going to school construction. As I noted on Monday, this improves the NGFO balance sheet in the near term.

That said, using these unexpected revenues to add ongoing spending would not be sustainable. As Sen. Robinson said at the revenue forecast meeting last week, “We obviously have very positive revenue with the capital gains tax for the very short term, which, again, will help some in the short term, but it doesn’t solve longer-term budget shortfalls. And, if you took that out, the forecast is generally down.”