1:39 pm

September 8, 2023

In a post this week, the Tax Policy Center (a joint venture of the Urban Institute and Brookings Institution) writes,

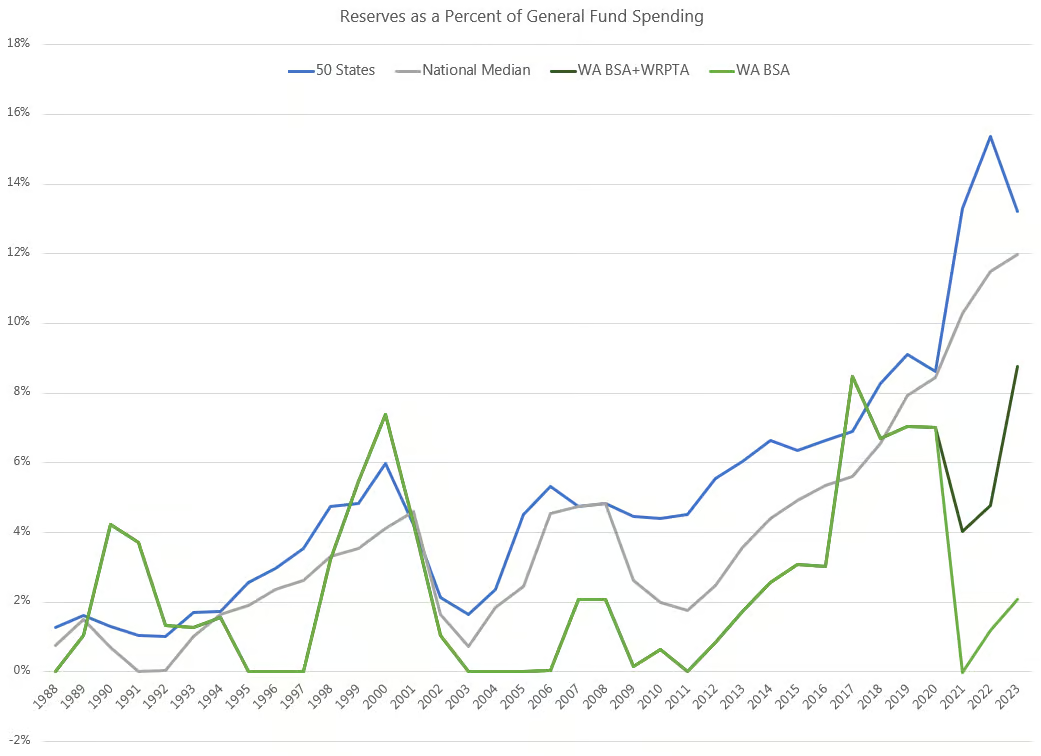

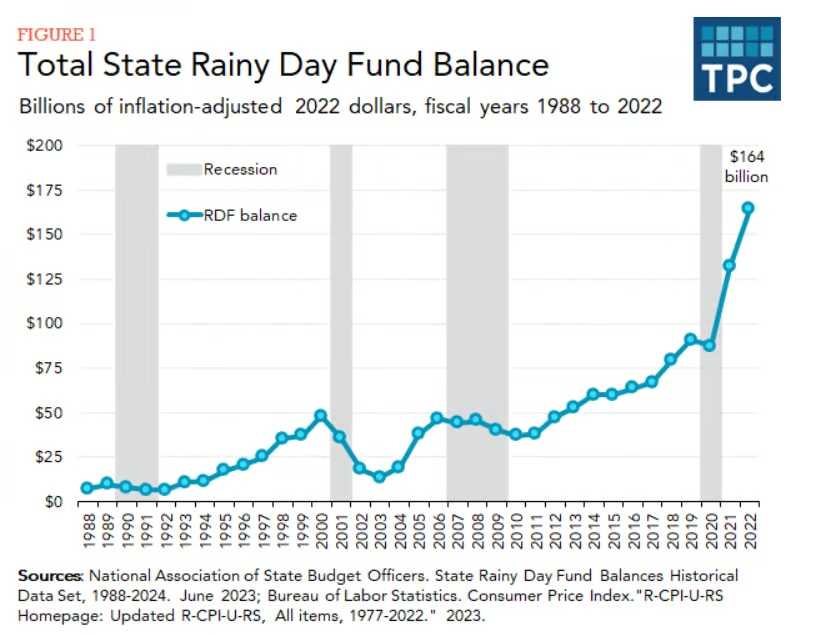

As a share of total general fund spending, total state rainy day fund balances have climbed steadily since the Great Recession, now totaling 15.4 percent of state spending in fiscal year 2022, the highest share ever recorded.

Measured as a share of their respective spending, Wyoming (96 percent), Alaska (48 percent), New Mexico (38 percent) and California (34 percent) had the highest state rainy day fund balances. Besides New Jersey, Washington (1.2 percent), Illinois (1.6 percent), Hawaii (3.7 percent), and New York (3.9 percent) had the lowest fund balances.

These figures are actual data from 2022 from the National Association of State Budget Officers. However, the data understate Washington’s reserves because they only consider the budget stabilization account (BSA). They don’t include the Washington rescue plan transition account (WRPTA).

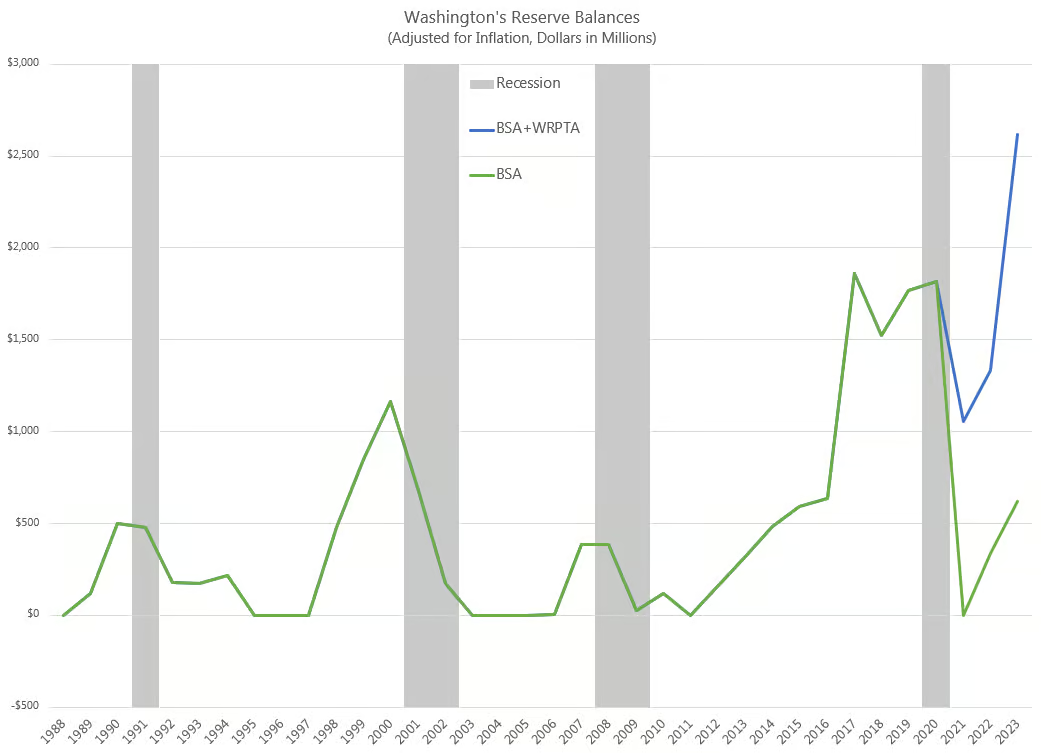

In 2021, the Legislature—despite having no shortfall—transferred the entire balance of the BSA ($1.820 billion) to the general fund–state (GFS). Then, it transferred $1.0 billion of that to the new WRPTA, where it could be accessed more easily than if it had stayed in the constitutionally-restricted BSA. The balance of the WRPTA grew to $2.1 billion in 2023, but the Legislature transferred $1.302 billion of that to the GFS in the 2023–25 budget. In 2021, 2022, and 2023, the WRPTA had a higher balance than the BSA. The credit ratings agencies have recognized it as a reserve account for the state.

As the Tax Policy Center notes, Washington’s BSA balance in 2022 was just 1.2% of general fund spending. This was the second lowest among the states. However, including both BSA and WRPTA funds, Washington’s reserves were 4.8% of general fund spending (the sixth lowest). (In 2023, including both the BSA and the WRPTA, Washington’s reserves were an estimated 8.8% of general fund spending—the 12th lowest.)

Although we’re still in the bottom half of the states, there’s no universal rule of thumb for the appropriate level of reserves. Many states need to have higher levels of reserves than Washington because they have more volatile revenue structures. Also note that this analysis excludes unrestricted ending fund balances, which have made up a substantial part of total reserves for Washington in recent years. Including the BSA, WRPTA, and unrestricted balance in funds subject to the outlook (NGFO), Washington’s reserves at the end of 2025–27 are estimated to be 8.1% of revenues, which is healthy but short of the Treasurer’s recommended 10%.

Additionally, the Tax Policy Center writes, “For now, though, states are in a far stronger fiscal position than they were after exiting the previous two economic downturns. In real dollars, total state balances two years after the prior two economic downturns were $13 billion (2003) and $38 billion (2011), compared to $164 billion today.” They include the following chart, which shows that total rainy day balances dropped during recessions—except the 2020 recession.

I’ve recreated this chart for Washington below. Washington’s reserves follow the same pattern as total state rainy day funds—except in the 2020 recession. While total state rainy day fund balances increased by $42.7 billion from 2019 to 2021, Washington’s (including the BSA and WRPTA) decreased by $619 million. Only eight other states reduced their rainy day funds over that period and only Alaska’s decrease ($1.2 billion) was deeper than Washington’s. As I noted above, this reduction to reserves came even as Washington faced no budget shortfall.

Finally, in the chart below, note the progress Washington has made on building up its reserves since the Great Recession. Certainly, there have been choices made over the years that have unnecessarily reduced the level of reserves. But our state has instituted valuable budget sustainability practices, both in the constitution and in statute, that are bearing fruit.