11:32 am

May 30, 2025

Gov. Ferguson has acknowledged that there will be unintended consequences from the tax bills approved this year. Nevertheless, he signed the bills—but for one partial veto. Given the way the Legislature structured the tax bills, it was impossible for Gov. Ferguson to veto many of their individual provisions.

Generally, the governor of Washington may veto entire bills or sections of bills. He does not have line-item veto power. According to Article III, Section 12 of the state constitution,

If any bill presented to the governor contain several sections or appropriation items, he may object to one or more sections or appropriation items while approving other portions of the bill: Provided, That he may not object to less than an entire section, except that if the section contain one or more appropriation items he may object to any such appropriation item or items.

The tax bills do not contain appropriation items, so Gov. Ferguson could only veto full sections of the bills. For example, in ESSB 5814 (applying the sales tax to certain services), Gov. Ferguson could not veto Sec. 101(3)(k)—which applies the sales tax to advertising—while leaving the rest of Sec. 101 (which applies the sales tax to several other services) intact.

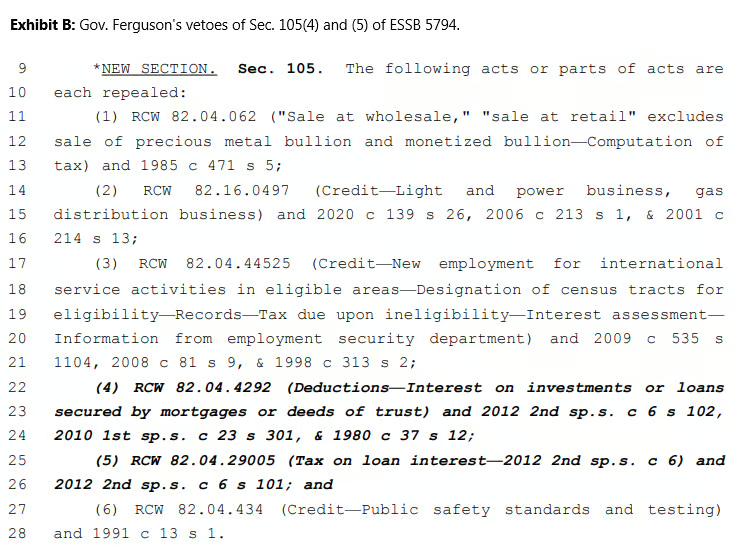

So how could Gov. Ferguson veto Sec. 105(4) and (5) of ESSB 5794 (repealing several tax “preferences”) while leaving the other parts of Sec. 105?

In 1997, the state Supreme Court held,

The Legislature’s designation of a section is conclusive unless it is obviously designed to circumvent the Governor’s veto power and is “a palpable attempt at dissimulation.” But where, as here, we discern legislative drafting that so alters the natural sequences and divisions of a bill to circumvent the Governor’s veto power, we reserve the right to strike down such maneuvers.

(Citations omitted.)

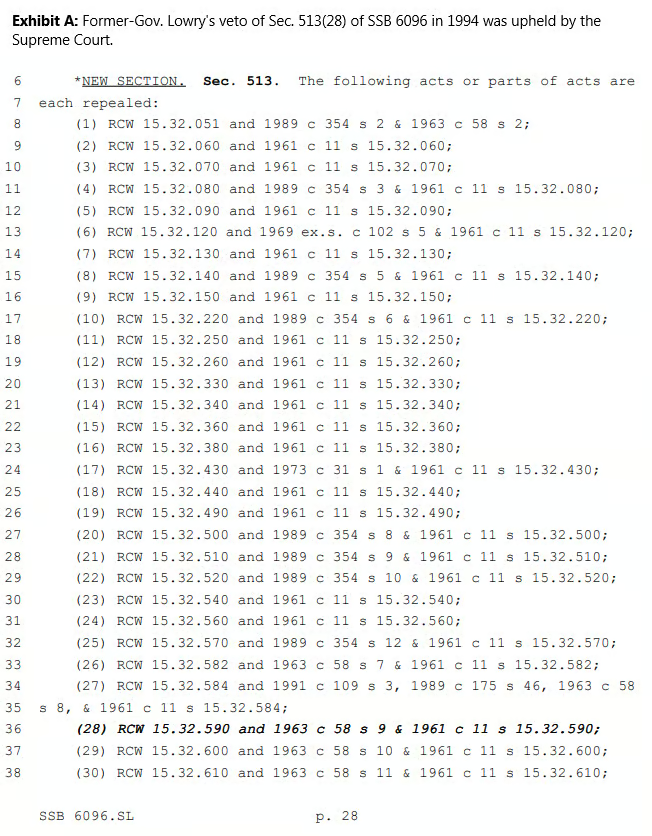

The 1997 case was about former-Gov. Lowry’s partial veto of SSB 6096 in 1994. He had vetoed Sec. 513(28), even though the subsection wasn’t an appropriation. Sec. 513 is a list of several acts that the bill was repealing (see Exhibit A). By vetoing Sec. 513(28), Lowry was vetoing the repeal of one specific act.

The Supreme Court said, “We uphold Governor Lowry’s veto of the subsections here because the 103 ‘subsections’ of a single section of the 1994 legislation involved repeal of whole sections of the Revised Code of Washington and were de facto ‘sections’ of legislation to which the veto applies.”

As shown in Exhibit B below, Gov. Ferguson’s vetoes of Sec. 105(4) and (5) of ESSB 5794 seem to match the circumstances around Lowry’s veto. Thus, it seems that they would pass constitutional muster if challenged.

However, I do wonder about one of Gov. Ferguson’s operating budget vetoes. The Supreme Court has also held, about appropriations items, “Read together, Lowry and Locke hold that unless the legislature clearly attempts to circumvent the governor’s veto power, we must presume that a legislatively designated ‘full subsection’ constitutes a whole, indivisible appropriation item.”

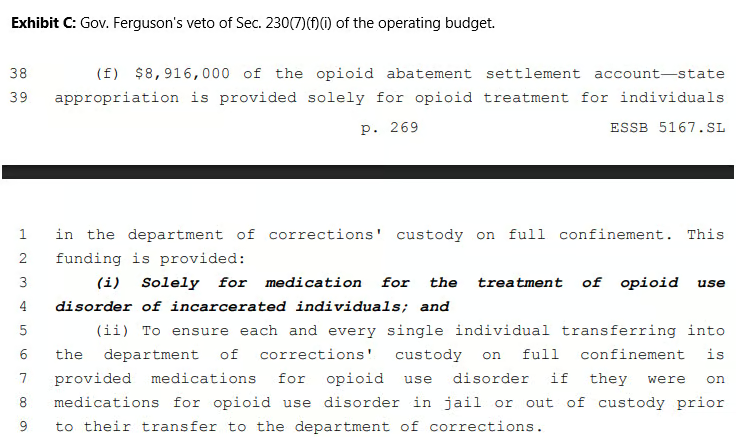

Gov. Ferguson’s veto of Sec. 230(7)(f)(i) of the operating budget seems like it might fall afoul of that, if challenged in court.