12:54 pm

June 22, 2021

The capital gains tax bill (ESSB 5096) specifies that the first $500 million of tax collections each year will be deposited in the education legacy trust account (ELTA) and any remainder each year will be deposited in the common school construction account (CSCA). (The amount deposited in the ELTA will be adjusted by inflation each year.)

The 2021–23 operating budget assumes that the tax will increase state revenues to funds subject to the outlook (NGFO) by $415.0 million in 2021–23 and $840.0 million in 2023–25. According to the Department of Revenue (in the final, revised fiscal note), in FY 2023, the tax is expected to increase ELTA revenues by $500.0 million and CSCA revenues by $27.0 million.

The net impact to the NGFO is $415.0 million (instead of $500.0 million) because the bill also provides a business & occupation (B&O) tax credit for amounts that would be subject to both the B&O tax and the capital gains tax. This policy reduces general fund–state revenues by $77.0 million and workforce education investment account revenues by $8.0 million. (Both accounts are part of the NGFO.)

The bill is estimated to increase revenues to the ELTA by $1.028 billion in 2023–25 and $1.070 billion in 2025–27. It is estimated to increase revenues to the CSCA by $134.0 million in 2023–25 and $188.0 million in 2025–27.

The CSCA (fund 113) was established by Article IX, section 3 of the state constitution, “to be used exclusively for the purpose of financing the construction of facilities for the common schools.” Fund sources for this account include timber sales from school and state lands and the interest from the permanent common school account.

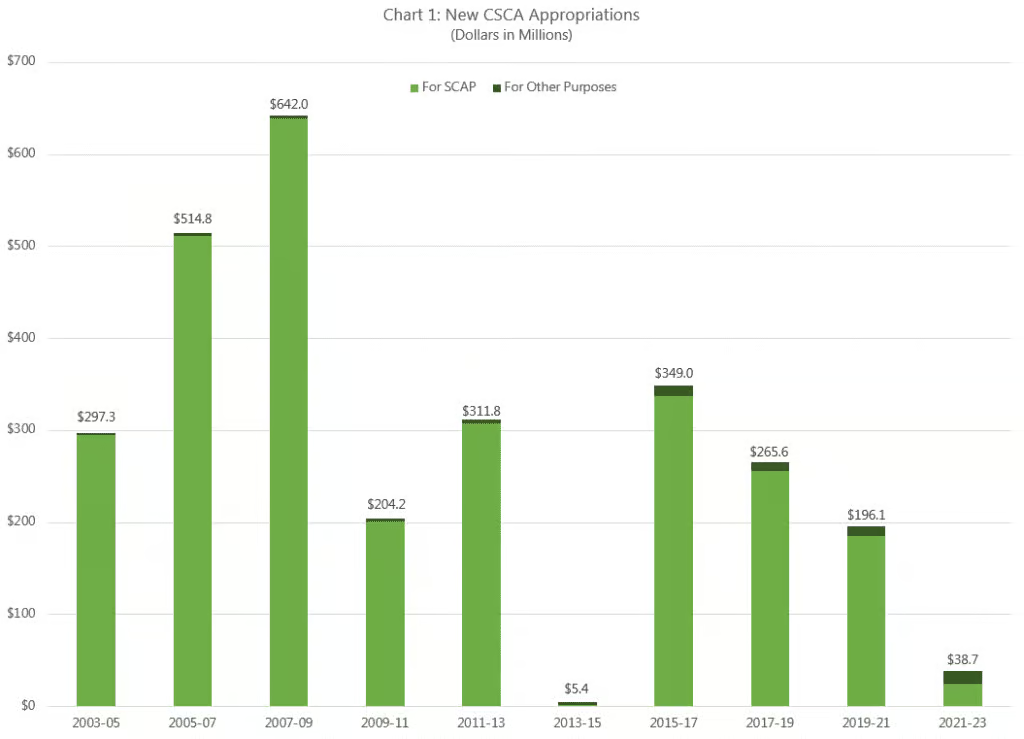

Most of the state’s appropriations from the CSCA are for the school construction assistance program (SCAP), as shown in Chart 1. In 2021–23, $25.0 million of the CSCA was appropriated for the SCAP. The state building construction account (i.e., bonds) funds $702.7 million of the SCAP in 2021–23. Although the state building construction account has funded most of the SCAP in recent biennia, the CSCA funded most of the program prior to the Great Recession (see Chart 2). (In 2007–09, $133.9 million from the education construction account and $103.1 million from the education savings account were transferred to the CSCA.)

The state uses the SCAP to help school districts fund new construction projects (and modernization of existing schools). According to the Office of Superintendent of Public Instruction, “The amount the state contributes varies by district as a result of the state funding assistance percentage, and by project due to eligible recognized construction costs.” Further, “to receive state funding assistance, a school district must raise revenues to demonstrate local support for the proposed project.” (These local revenues are typically bonds.)

The capital gains revenues would be a substantial boost to the CSCA—if they are ultimately collected. As we noted in our policy brief on the enacted operating budget, the courts could determine that the capital gains tax is unconstitutional, or it could be repealed by initiative. And even if the tax is upheld, it is a highly volatile revenue source. If the capital gains revenues dip below the level dedicated to the ELTA, none would go to the CSCA.

Categories: Budget , Tax Policy.