11:30 am

February 19, 2026

The Senate passed the income tax bill (SB 6346) on Monday. I wrote about the bill as introduced here and here. Amendments were adopted by the Ways and Means Committee and on the Senate floor, some of which will have significant fiscal impacts.

Some of the amendments made by the Ways and Means Committee include:

- The small business B&O tax credit provision was increased so that about $300,000 of business income would be exempt, and the credit would fully phase out at about $600,000 of income. Under current law, the credit exempts about $125,000 of business income and phases out at about $250,000. As introduced, SB 6346 would have increased the credit to exempt about $250,000 of income, with a full phase out at about $500,000.

- The charitable deduction increased from $50,000 to $100,000. (This amount is not adjusted for inflation.)

- A deduction was added for amounts deposited in a merchant marine capital construction fund.

- The distribution for public defense was increased. Originally, counties would have received 5% of the income tax revenues. Now, 7% of the revenues are dedicated to a new local government public defense funding stabilization account. Of these local public defense revenues, 10% will go to cities and the remainder will go to counties.

Some of the amendments approved on the Senate floor include:

- Some of the changes made in ESSB 5814 last year would be repealed. ESSB 5814 extended the sales tax to more services. As passed by the Senate, the income tax bill would undo those changes, except advertising services would still be subject to sales tax. (The provisions of ESSB 5814 that increased nicotine taxes would remain in place.) These changes would be effective Jan. 1, 2030.

- Charitable donations deducted from the capital gains tax are no longer added back into Washington base income for purposes of the income tax.

- Income from a non-grantor trust that was funded with an incomplete gift is included in Washington base income for residents. (Non-grantor trusts are trusts in which the person who established the trust does not control it. For federal income tax purposes, the income of a grantor trust is included in the grantor’s individual income taxes. Non-grantor trusts are treated as separate entities from the grantor.)

- The definition of “substantially underpaid” is changed. Originally, the bill would have assessed a penalty of 5% of the amount of the underpaid tax, if estimated tax payments were less than 80% of the actual tax due. As passed by the Senate, the 5% penalty applies if estimated tax payments are less than the tax shown on the income tax return, unless the estimated tax payments are 90% of the tax shown on the return or 100% of the tax shown on the most recently filed tax return.

- The internal revenue code is defined to mean the federal internal revenue code in effect on Jan. 1, 2026. Earlier versions of the bill would have allowed the Department of Revenue (DOR) to update the definition to subsequent dates by rule.

- DOR is allowed to require additional income reporting through rulemaking, including a Washington schedule K-1 form.

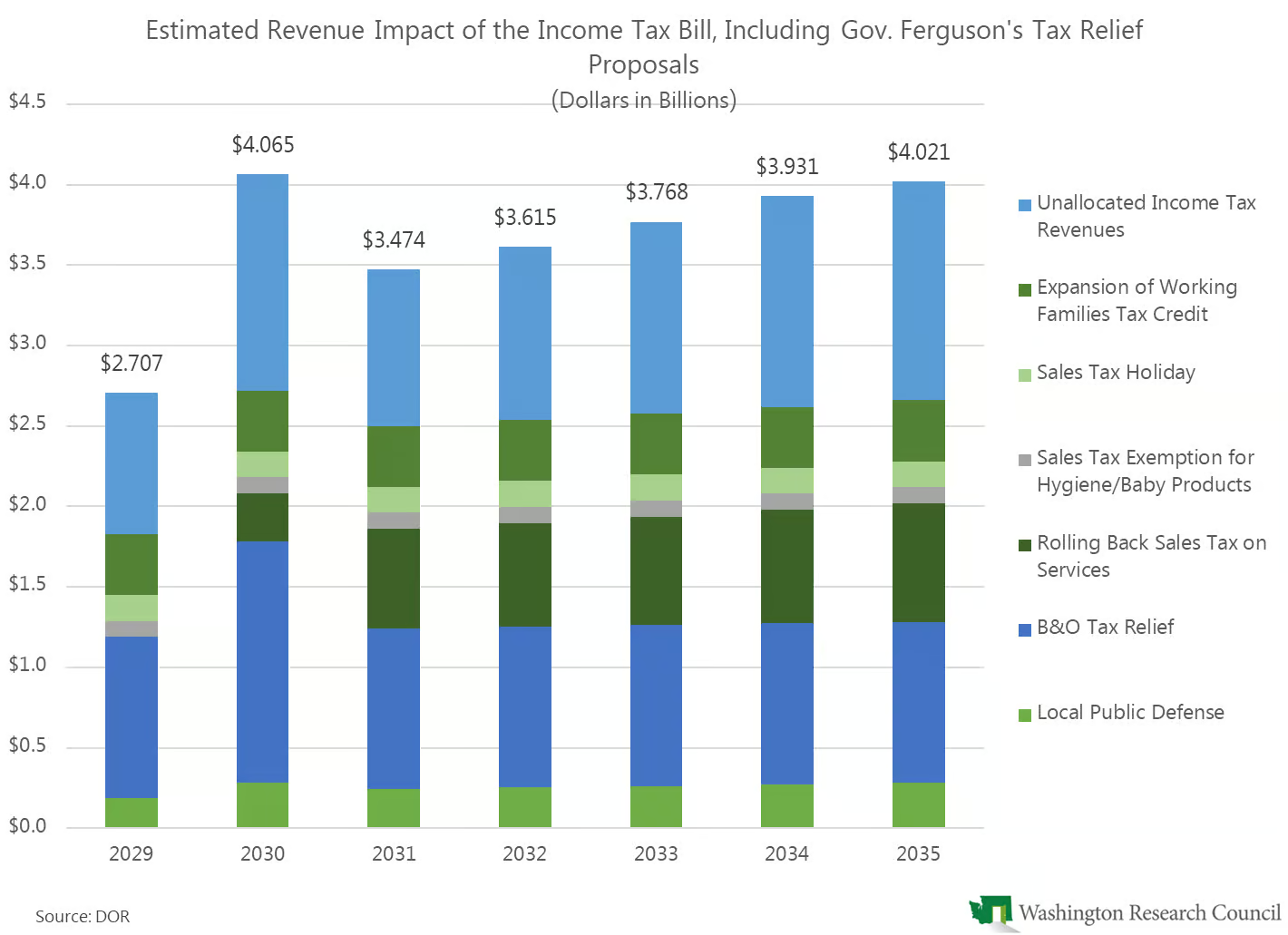

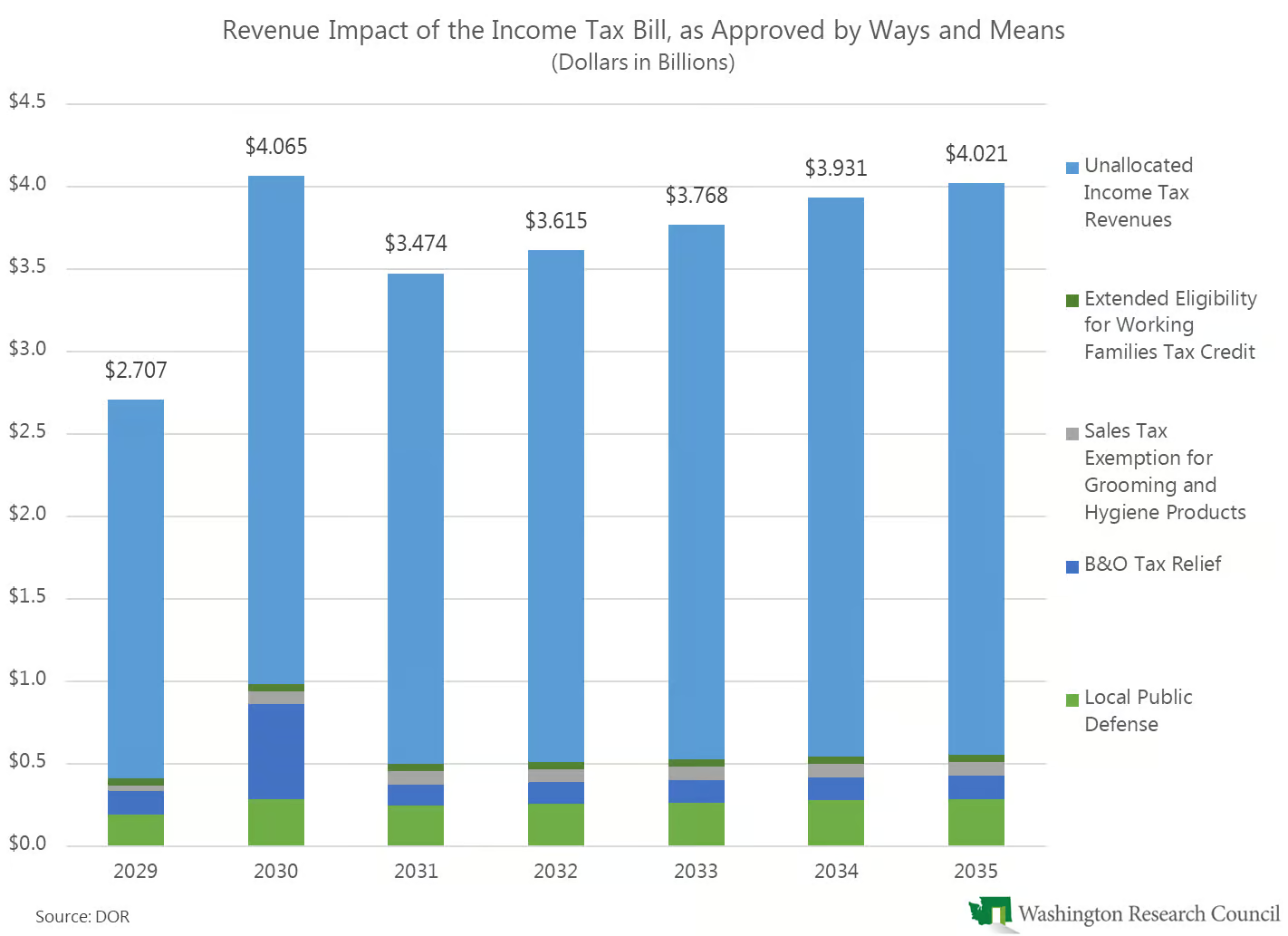

A fiscal note for the version passed by the Senate is not yet available, but there is a fiscal note for the version approved by Ways and Means. As approved by Ways and Means, the income tax would increase revenues by $2.707 billion in 2027–29, $7.539 billion in 2029–31, and $7.383 billion in 2031–33. Over the six-year period, this is a reduction of $65 million compared to the original bill.

The increased B&O tax credit in the Ways and Means version would add $95.4 million in tax relief over the six-year period compared to the original bill. The distributions for public defense would increase by $349.3 million over the six-year period compared to the original bill.

(According to DOR, the estimate jumps in fiscal year 2030 because estimated tax payments are not required for tax year 2028. Consequently, FY 2029 revenues include initial tax payments for TY 2028. FY 2030 includes final TY 2028 payments, four quarters of estimated payments for TY 2029, and one quarter of estimated payments for TY 2030. Beginning in FY 2031, fiscal year collections include one fewer quarter of estimated payments. For example, FY 2031 revenues include final payments for TY 2029, three quarters of estimated payments for TY 2030, and the first quarter of estimated payments for TY 2031.)

It’s unclear how the changes made on the Senate floor will affect revenues. The changes made related to ESSB 5814 will certainly reduce state revenues significantly. My extremely rough estimate, based on the ESSB 5814 fiscal note, is that the provisions would reduce revenues by about $600 million a year.

Meanwhile, on Tuesday, Gov. Ferguson proposed several other tax relief ideas during a press conference. I have not seen any formal, written estimates of his proposal. Based on his statements at the press conference, he proposes:

- Using $1 billion annually to increase the small business B&O credit so that it exempts $2.5 million of income,

- Using $380 million annually to expand the Working Families Tax Credit (both the number of people who qualify and the amount of the credit),

- Using $200 million to exempt both hygiene and baby products (including diapers) from the sales tax, and

- Using an unspecified amount to provide two sales tax holidays.

He said that his tax relief proposals would total $1.9 billion a year, suggesting that he assumes the sales tax holidays would reduce revenues by $320 million a year.

Additionally, the governor said that he supports the changes to ESSB 5814 and the early sunset of the temporary B&O tax surcharge that are included in the income tax bill as passed by the Senate. He also supports the rollback of the estate tax rates.

The following chart uses the fiscal note for the version of the income tax bill that was approved by Ways and Means as a base, then adds my very rough estimate of the changes related to ESSB 5814 and the governor’s proposed tax relief. Until there is an official fiscal note of the version that passed the Senate and more detailed information on the governor’s proposals, this is meant to give a ballpark idea of how these new tax relief ideas could fit into the income tax revenues.