2:13 pm

April 13, 2023

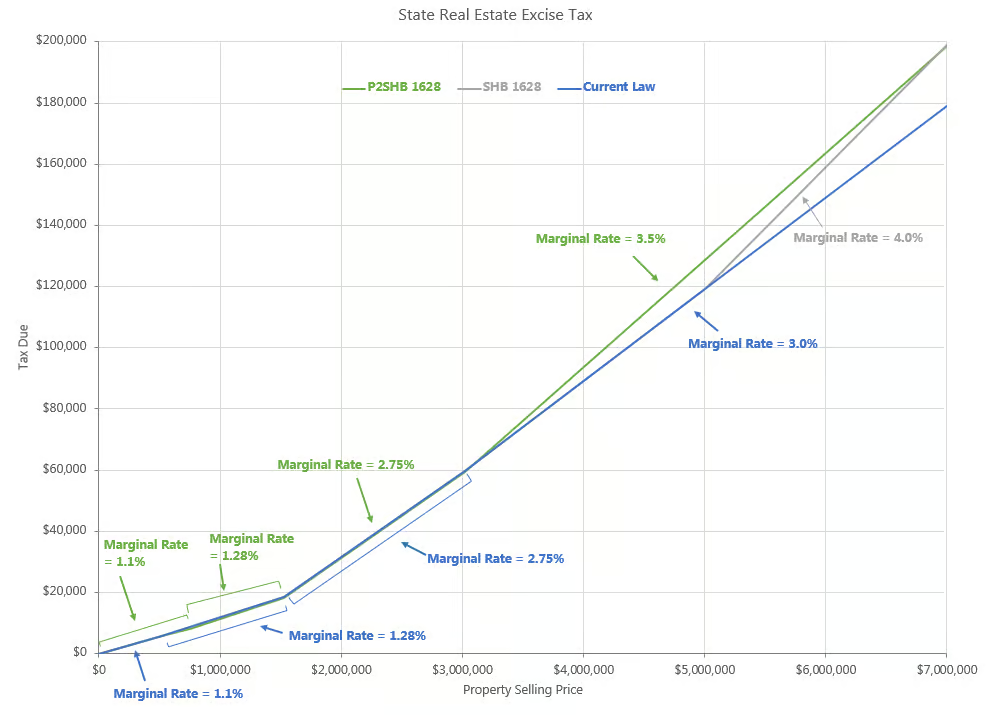

Tomorrow morning SHB 1628 is scheduled for executive session in the House Finance Committee. SHB 1628 would increase the real estate excise tax (REET). (I wrote about the original version here.) As approved by the House Committee on Local Government in February, the bill would increase the top REET rate to 4.0% for the portion of a property’s selling price that is over $5 million. The current top rate is 3.0% for the portion of the selling price that is more than $3.025 million.

House Finance will consider a proposed substitute bill. P2SHB 1628 would make several changes to the tax rates. It would increase the amount of the selling price subject to the lowest rate (1.1%) and it would make the top rate 3.5% on the portion of the selling price that is more than $3.025 million. Compared to current law, this would slightly reduce taxes due on properties selling for less than $3,106,000 and increase taxes due on properties selling for more than $3,106,000. (The rate changes would be effective beginning Jan. 1, 2025.)

P2SHB 1628 would temporarily not increase the rate for commercial properties. For calendar years 2025 and 2026, the portion of the selling price for a commercial property that is over $3.025 million would continue to be subject to a rate of 3.0%.

Both SHB 1628 and P2SHB 1628 would allow cities and counties to impose an additional 0.25% REET for affordable housing purposes. P2SHB 1628 would additionally allow counties to pledge the revenues from this additional REET to repay bonds issued to finance affordable housing construction and acquisition.

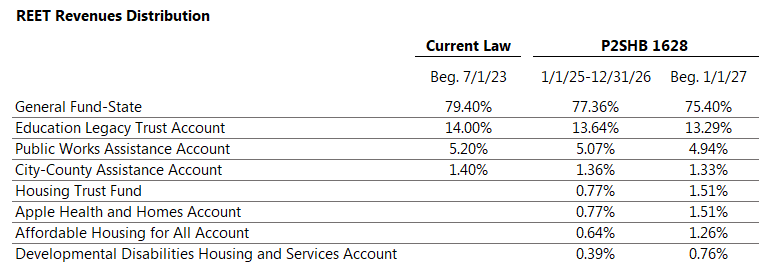

Under current law, REET revenues are deposited in four different accounts. P2SHB 1628 would deposit REET revenues in the current four accounts plus four more, as shown in the table below. Under the bill, beginning in fiscal year 2026, at least $5 million of the REET revenues deposited in the housing trust fund would have to be used for “facilities housing low-income migrant, seasonal, or temporary farmworkers.”

A draft fiscal note for P2SHB 1628 estimates that the changes would increase revenues to all accounts by $22.2 million in 2023–25, $177.2 million in 2025–27, and $405.4 million in 2027–29. REET revenues to funds subject to the outlook (NGFO) would decrease by $1.6 million in 2023–25, $8.4 million in 2025–27, and $1.1 million in 2027–29.