1:09 pm

February 9, 2023

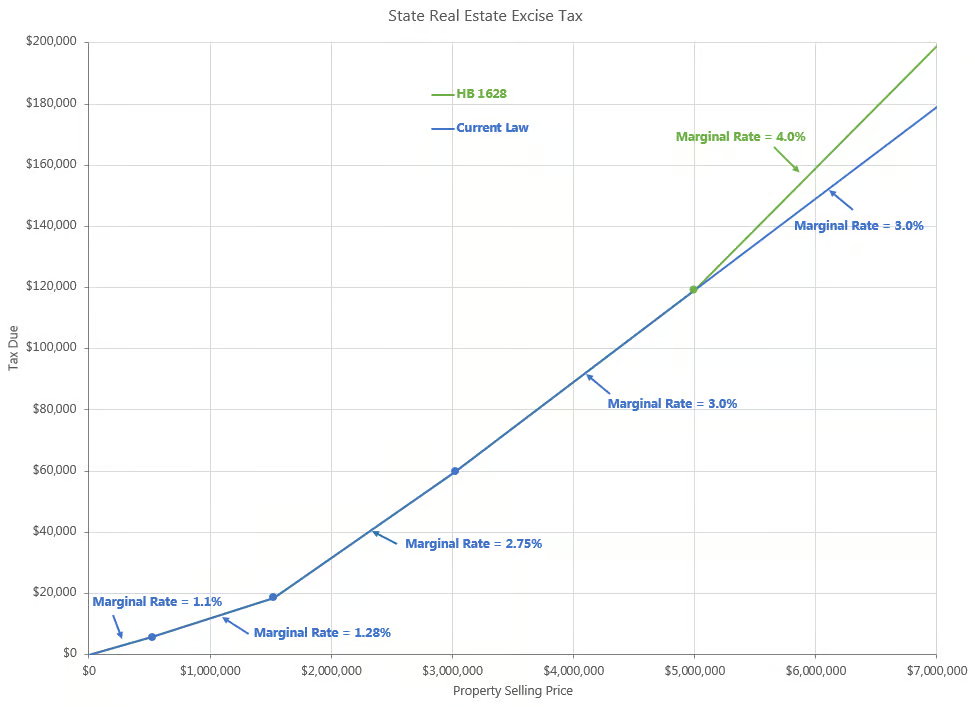

Until 2020, the real estate excise tax (REET) was a flat 1.28% tax on the selling price of real estate. In 2019, the Legislature graduated the rate, which reduced the rate for some taxpayers and increased it for others. (We wrote about the change in this policy brief.)

Under current law, the maximum rate is 3%, which applies to the portion of the selling price that is more than $3.025 million. HB 1628, which is scheduled for executive session in the House Committee on Local Government tomorrow, would apply the 3% rate to the portion of the selling price that is more than $3.025 million and equal to or less than $5.0 million and add a 4% rate for the portion of the selling price that is more than $5.0 million. This change would be effective Jan. 1, 2025.

REET collections under the current rate structure are split between the general fund–state (GFS), education legacy trust account (ELTA), public works assistance account (PWAA), and city-county assistance account (CCAA). By my reading of the bill, HB 1628 would leave those distributions alone.

HB 1628 would require the Department of Revenue (DOR) to calculate the increase in REET collections due to the 4% rate, compared to what collections would have been at the current 3% rate. (By my reading, this would be the area between the green and blue lines in the chart below.) The amount of this difference would be deposited into four different accounts:

- 30% to the Washington housing trust fund,

- 30% to the apple health and homes account,

- 25% to the affordable housing for all account, and

- 15% to a new developmental disabilities trust account.

(The new developmental disabilities trust account would be used for housing programs for people with developmental disabilities.)

A partial fiscal note posted on Feb. 7 interprets the bill differently. The fiscal note assumes that there would be substantial revenue reductions to the GFS, ELTA, PWAA, and CCAA (totaling -$122.4 million in 2023–25 and -$1.891 billion in 2025–27). Under this analysis, the housing accounts would receive $163.3 million in 2023–25 and $2.521 billion in 2025–27. However, DOR has told me that they will be issuing a new fiscal note that will take a different interpretation. I’d guess that the reductions to the four current accounts will go away and the increases to the four new accounts will be smaller. If the Legislature chooses to move forward with this bill, it should consider modifying the language to be more clear about which revenues should be deposited in which account.

Finally, currently cities and counties may impose various REETs (see RCW 82.46.010, 82.46.035, 82.46.070, and 82.46.075). (Here is the current list of the local REETs in effect, by locality.) HB 1628 would allow cities and counties to impose an additional 0.25% REET for construction or acquisition of affordable housing and for affordable housing operations. According to the Feb. 7 fiscal note, HB 1628 would increase local government revenues by $222.4 million in 2023–25 and $449.8 million in 2025–27.