2:04 pm

July 18, 2024

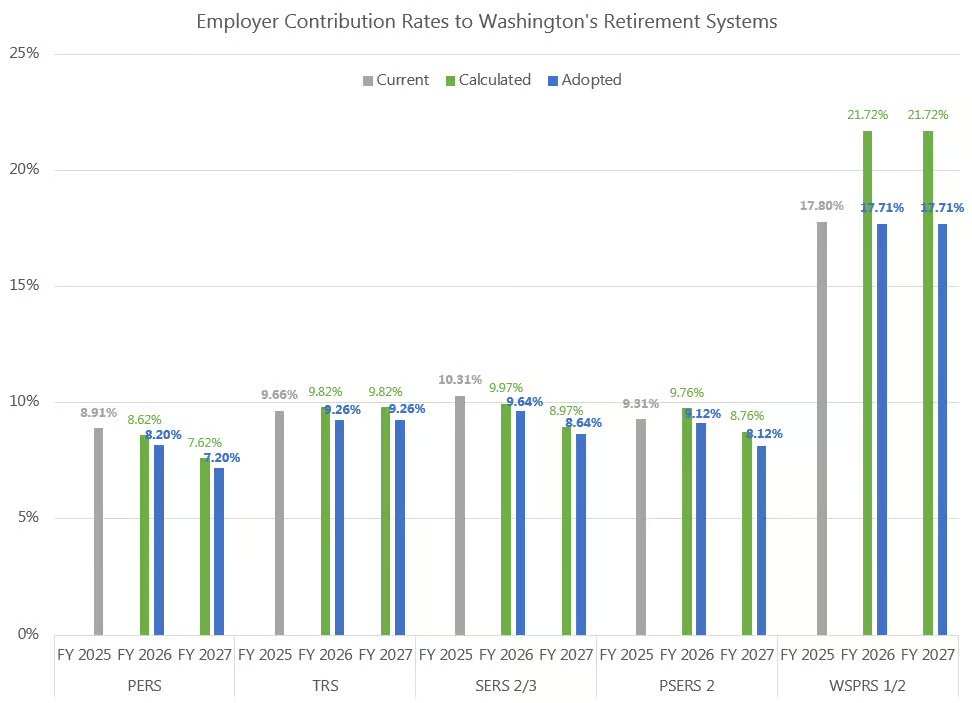

Yesterday the Pension Funding Council (PFC) adopted state pension rates for 2025–27. The employer contribution rates will decline for each pension system from FY 2025 to FY 2026, and they will either decrease further or stay the same in FY 2027 (depending on the system). For example, the employer contribution rate for the public employees’ retirement system (PERS) is currently 8.91%. Under the adopted rates, it will decrease to 8.20% in FY 2026 and to 7.20% in FY 2027.

As a result, the Office of the State Actuary (OSA) estimates that the general fund–state (GFS) savings for 2025–27 (compared to the current rate) will be $205 million. Non-GFS state accounts would save an estimated $123 million, and local government employers would save an estimated $258 million.

However, the adopted rates are lower than the rates calculated by the OSA in the preliminary 2023 Actuarial Valuation Report. (The calculated rates represent the contributions required to fund future benefits.) According to the OSA, the adopted rates (option 2B in the presentation from yesterday’s meeting) represent the average of current rates and the estimated rates for 2027–29. Thus, the option “emphasizes the management of rate volatility at the potential expense of weakened plan solvency.” If the PFC had adopted the calculated rates, the GFS would have saved an estimated $61 million in 2025–27.

The OSA also noted that they expect all retirement plans to have funded ratios of at least 100% within five years. (It’s not yet clear how the newly adopted rates will affect that estimate.) Currently, the combined funded status of all the plans is 96%, based on the current assumed investment return of 7%. (The higher the investment return, the lower contributions need to be to maintain solvency.)

Importantly, for the first time, the 2023 Actuarial Valuation Report shows what the funded status of the plans would be if the assumed investment return was based on a portfolio of low-default-risk fixed income securities (with an investment return of 3.9% for open plans and 4% for closed plans). Under this scenario, which is required to be presented by new standards of practice from the Actuarial Standards Board, the state’s retirement plans would be only 62% funded.

As the OSA explains, “By comparing the funded status under current law funding policy to the [low-default-risk obligation measure] basis, we can provide a sense for how much future accrued benefit payments rely on returns from higher risk investments.”

Categories: Budget , Employment Policy.