1:33 pm

May 21, 2021

One of the major new policy bills enacted this year is E2SSB 5237, the Fair Start for Kids Act. The bill makes several enhancements to child care and early learning. Some of these include:

- Expanding eligibility for Working Connections Child Care (WCCC, phased in from FY 2022–2028) and reducing copays (phased in through FY 2026).

- Increasing child care provider rates so that they are at the 85th percentile of market.

- Expanding eligibility for the Early Childhood Education and Assistance Program (ECEAP). Under the bill, until SY 2030–31, children will be eligible for ECEAP if their families have incomes at or below 36% of the state median income. Beginning in SY 2030–31, children will be eligible if family income is at or below 50% of the state median income. (Currently, children are eligible if family income is at or below 110% of the federal poverty level. According to the bill, 36% of state median income for a family of three is roughly 130% of the federal poverty level.)

- Increasing ECEAP provider rates, including by 10% for SY 2021–22.

- Implementing a birth to three ECEAP for children with family incomes at or below 50% of the state median income, effective FY 2027.

Additionally, legislation in 2010 made ECEAP an entitlement, with full implementation originally planned for SY 2018–19. This date has been changed over the years; before E2SSB 5237, full implementation was planned for SY 2022–23. E2SSB 5237 moves full implementation to SY 2026–27.

The bill doesn’t include a dedicated funding source, but effective May 7, 2021, the education legacy trust account (ELTA) may permanently be used for early learning and child care programs. The ELTA is subject to the four-year balanced budget requirement.

Meanwhile, the bill creates the fair start for kids account, which may only be used for child care and early learning. Effective July 25, 2021, the fair start for kids account will also be included in the four-year balanced budget requirement.

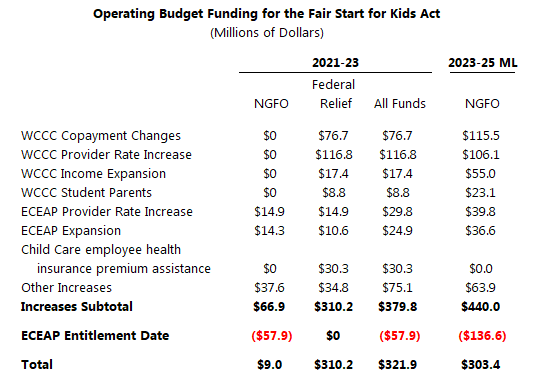

The 2021–23 operating budget (as passed by the Legislature) increases appropriations from all funds by $321.9 million to implement E2SSB 5237. That includes savings of $57.9 million from delaying implementation of the ECEAP entitlement. As the table shows, only $9.0 million of the total comes from the NGFO (funds subject to the outlook). The funding mainly comes from federal coronavirus relief.

The budget bill states, “The legislature finds that the state lacked the fiscal capacity to make [child care] investments and the additional federal funding has provided the opportunity to supplement state funding to expand and accelerate child care access, affordability, and provider support as the state navigates the COVID-19 pandemic and its aftermath.”

The federal relief is one-time money, which makes it a questionable funding source for an ongoing program. On top of that, the cost of implementing E2SSB 5237 will continue to rise over the next several years. For example, the budget documents include an estimate of how much new NGFO policy items will cost in 2023–25. The net cost is estimated to be $303.4 million in 2023–25 (including savings of $136.6 million from the entitlement delay). All of that will have to come from the NGFO.

And that doesn’t capture the cost of the ECEAP entitlement or various other new policies that don’t take full effect until after FY 2025. There is not yet a final fiscal note for E2SSB 5237, but the partial fiscal note estimates that (for example) the cost of the WCCC income expansion and copay changes will range from $89.8 million–$250.3 million in 2023–25. That range is estimated to jump to $443.2 million–$1.099 billion in 2025–27. Additionally, the ECEAP entitlement is estimated to cost $156.4 million in 2025–27.

The Legislature intends to use the newly enacted capital gains tax to pay for these child care and early learning programs after the federal relief is gone. Sen. Christine Rolfes told Washington State Wire in March, “The improvements in the first year of the plan are funded partially with federal funds that we’re getting specifically for child care purposes . . . . When the capital gains tax kicks in, that picks up the slack for the one-time funds and the federal funds.”

Under the capital gains tax bill (ESSB 5096), the first $500 million collected each year will go to the ELTA. The budget assumes the capital gains tax will increase NGFO revenues by $415.0 million in 2021–23 and $840.0 million in 2023–25. As Opportunity Washington writes, two lawsuits have now been filed that argue that the tax is unconstitutional.

Categories: Budget.