11:01 am

April 28, 2026

As the Seattle Times reported on Wednesday, Moody’s has changed its estimation of Washington’s credit outlook from stable to negative. Now, Fitch has followed suit. (S&P did not change its outlook this month, but in October, S&P moved Washington’s outlook down from positive to stable.) None of the three ratings agencies have reduced Washington’s credit rating at this point. (Washington’s bonds are rated Aaa by Moody’s, AA+ by S&P, and AA+ by Fitch.)

According to Moody’s,

The negative outlook reflects the increased likelihood that the state will rely on sizable one-time budget balancing measures over the next 12–18 months, continuing a trend of General Fund expenditures outpacing recurring revenues. The persistent operating imbalances and projected narrowing of budgetary reserves amid still solid economic and revenue conditions underscore the depth of the state’s structural budget challenges and reduce its financial flexibility to absorb unexpected revenue or expenditure shocks.

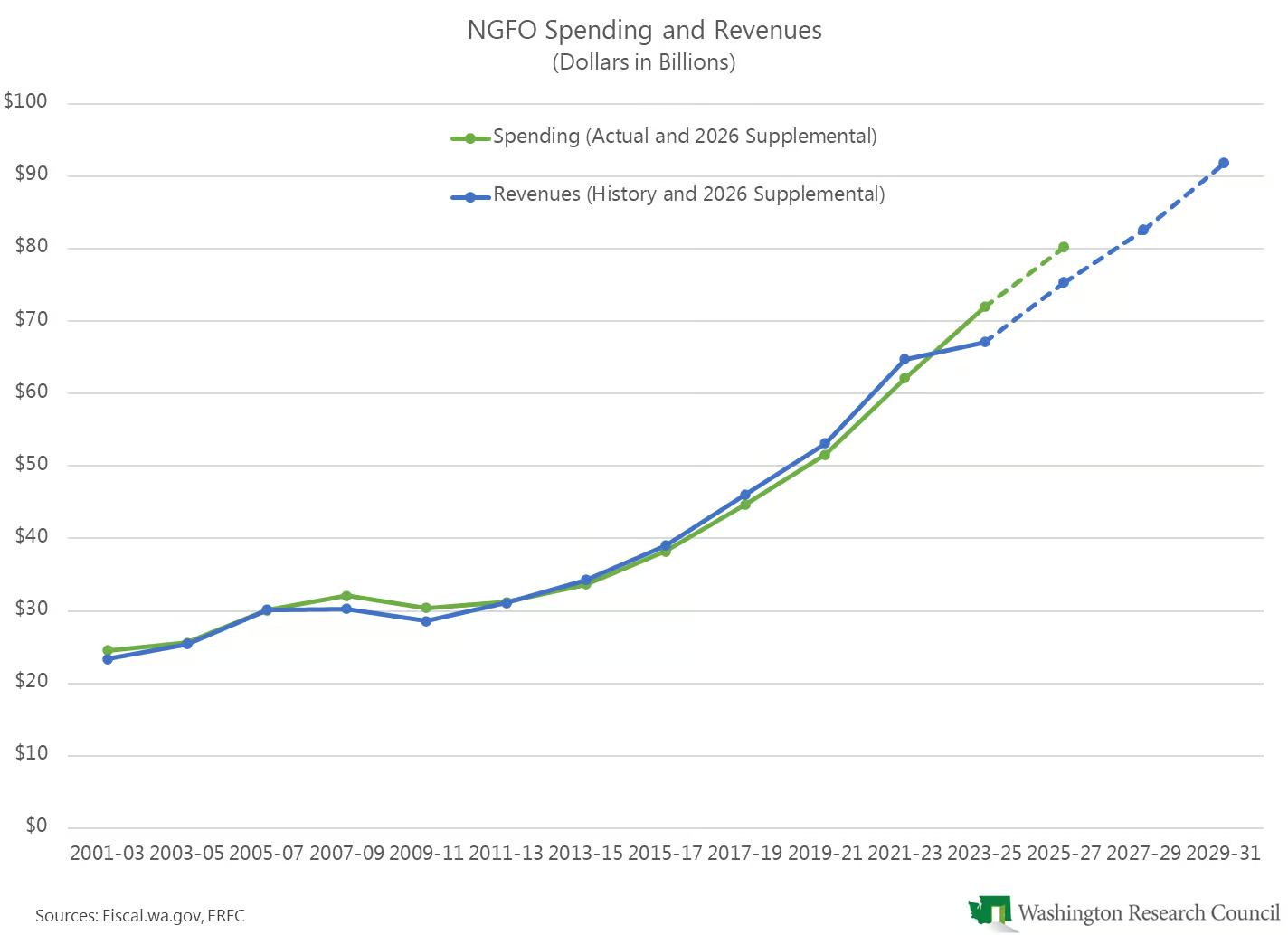

Indeed, Washington’s revenues were expected to increase even before the state adopted historically large tax increases last year and this year. Nevertheless, the state has tapped the rainy day fund and has been relying on unusually large transfers from other accounts to the general fund to balance the budget. As we showed in 2024, the reason we have been experiencing a budget problem is that the state spent far in excess of revenues in 2023–25. In the final accounting, spending in 2023–25 exceeded revenues by $4.8 billion—even as revenues were increasing. The tax increases the past two years were used to add new spending, not to close the ongoing gap between spending and revenues.

Moody’s could downgrade Washington’s credit rating should there continue to be “Protracted structural budget imbalances requiring significant reserve draws and/or other one-time budget solutions.” Further, regarding income tax revenues (that the state expects to collect beginning FY 2029), Moody’s writes, “sustained reliance on one-time budget balancing measures while awaiting its availability would be credit negative.” (As we have written, even if the income tax is collected as planned, it would not solve the problem.)

The use of the rainy day fund this year is a recurring theme in the three ratings reports. Fitch writes, “The Outlook revision to Negative from Stable reflects weakening of financial resilience due to budgeted drawdowns from the state’s Budget Stabilization Account (BSA) in the current biennium and risks around the state’s plan to restore reserves and structural balance.”

S&P writes, “The 2026 supplemental budget uses $880 million from its budget stabilization account (BSA) to help resolve its 3% budget gap. Given that this is a structural budget pressure, we believe that reducing resources that can be used during an economic downturn limits the state’s flexibility.” S&P also states that it “will monitor if the state still plans to fully replenish formal reserves in the next biennium.”

To that point, Moody’s claims, “While recent legislation authorized a $0.88 billion transfer of pension surplus resources to the BSA, this is not expected until fiscal 2029.” The 2026 supplemental notes that it is the intent of the Legislature to make this transfer on the last day of FY 2029, but this will be a policy decision for the 2027 Legislature. It is not actually authorized by any legislation at this point.

Although S&P continues to consider Washington’s outlook stable, they write, “We believe the state’s focus on resolving structural pressures is key to credit stability, and if the state does not prioritize its robust financial management practices to achieve balance, our view of its credit profile could weaken.” Further, “we believe the state’s proactive approach will allow it to make changes to control expenditures, if needed, but if management significantly relies on one-time solutions to resolve future gaps, this could have negative credit implications.”

As we wrote last year and this year, the state has taken a band-aid approach to the 2025–27 budget. The budgets have balanced due to a combination of new taxes, one-time resources, and unusual accounting assumptions. Although both budgets have included some spending reductions, they were offset by new spending on other priorities. The state has not yet tried reducing net spending.

Since 2021, the state has increased appropriations for new policy by a net of $15.5 billion (in addition to spending increases due to inflation and caseloads):

- $3.087 billion for 2021–23 in 2021,

- $6.189 billion for 2021–23 in 2022,

- $4.744 billion for 2023–25 (and -$1.179 billion for 2021–23) in 2023,

- $1.033 billion for 2023–25 in 2024,

- $1.024 billion for 2025–27 (and -$56.9 million for 2023–25) in 2025, and

- $620 million for 2025–27 in 2026.