11:16 am

March 9, 2026

Typically, federal and state tax codes automatically adjust various provisions—like exclusion and deduction amounts—for inflation. This helps to prevent bracket creep. As the Tax Foundation defines it, bracket creep “occurs when inflation, rather than real increases in income, pushes people into higher income tax brackets or reduces the value they receive from credits and deductions.”

For example, for Washington’s capital gains tax, the standard and charitable deduction amounts are annually adjusted for inflation using the Seattle area consumer price index (CPI).

In Washington, the estate tax brackets have never been adjusted for inflation. That bracket creep was exacerbated from 2018 to last year, when the Legislature finally acted to fix the statutory inflation adjustment for the exclusion amount, which had been pointing to a defunct consumer price index. This year, the Senate passed a version of SB 6347 that would roll back last year’s estate tax rate increases but leave the inflation adjustment fix alone.

As I wrote last week, the House Finance Committee passed a version of SB 6347 that would bizarrely return the defunct inflationary adjustment to statute. Of the Senate version, Rep. Street said, “This bill only rolls back the rates without looking at the exemption and CPI and that has a very negative impact to the amount of money brought in by this policy, especially looking forward into the future. I don’t think the state’s in a fiscal position to do that.”

Meanwhile, the version of the income tax bill that was passed by the Senate Feb. 16 would adjust the $1 million standard deduction annually using the Seattle area consumer price index. This matches the policy in the capital gains tax statute. However, the income tax charitable deduction would not be adjusted for inflation. Consequently, there would be an increasing divergence over time between the amount of real charitable giving that is exempt from the capital gains tax compared to the income tax.

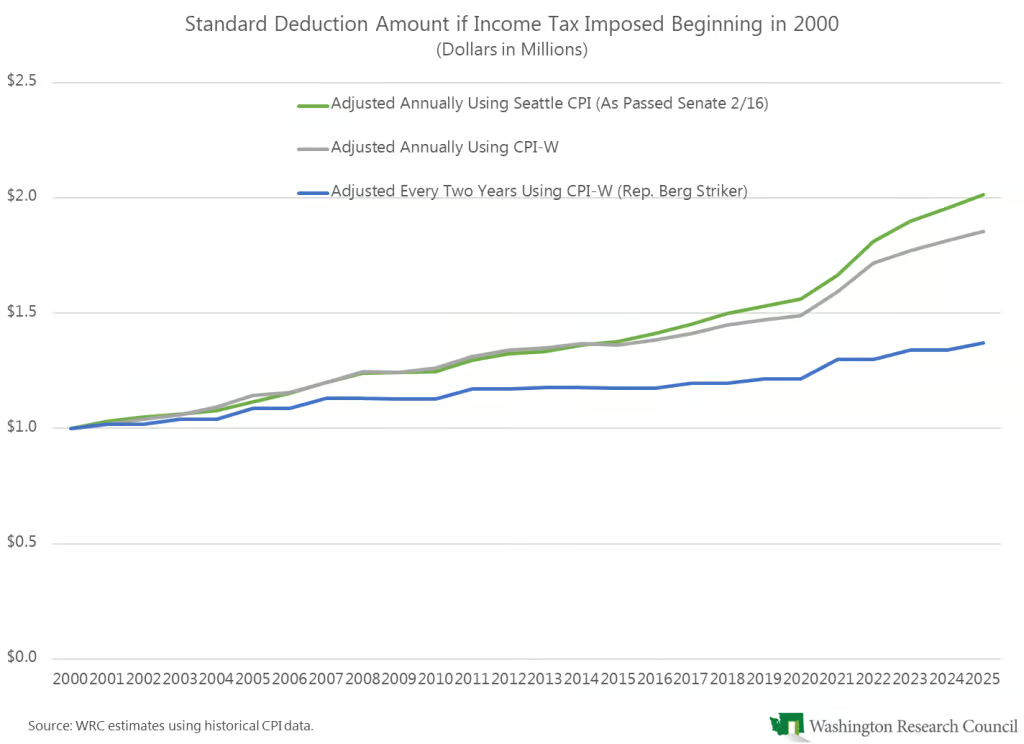

Further, as I noted on Friday, the income tax striking amendment proposed by Rep. Berg would change the inflation adjustment to the consumer price index for all urban wage earners and clerical workers (CPI-W). It would also make the adjustment only every other year.

The CPI-W has grown more slowly than Seattle CPI in recent years. If that trend continues, tying the inflation adjustment to CPI-W instead of Seattle CPI would mean more revenues for the state. As the chart shows, making the adjustment only every other year instead of annually would significantly erode the real value of the deduction.

There is no fiscal note for Rep. Berg’s striker yet, but the change to the inflationary adjustment is likely meant to increase the estimated revenues to the state.