3:17 pm

April 16, 2025

Increases to the capital gains tax and estate tax rates are included in the new tax package proposed by House and Senate Democrats. (I wrote about their B&O and sales tax proposals earlier.) SB 5813 and HB 2082 are identical; fiscal notes are not yet available.

Capital Gains Tax

The current capital gains tax rate is 7%. SB 5813 and HB 2082 would impose an additional 2.9% tax on the portion of gains exceeding $1 million. (This would effectively be the same rate proposal that was floated by Senate Democrats in December.)

Section 101 of the bills impose the additional tax. Section 301 specifies, “Section 101 of this act applies to taxes imposed in calendar year 2025 for collection in calendar year 2026.” This is probably just clarifying the difference between the tax year and the collections year, but it could also be read as indicating that the additional tax is only in effect for one year. Regardless, fiscal year 2026 would be the first year of collections at the higher rate.

Note, though, that the Department of Revenue has reported that total capital gains revenues declined from $780.4 million for tax year 2022 to $416.7 million for tax year 2023 (-46.6%). The amount collected from the top 10 taxpayers declined by 67.3%.

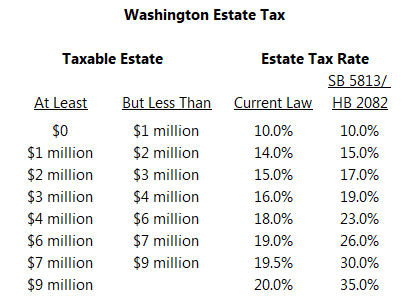

Estate Tax

SB 5813 and HB 2082 would keep the estate tax brackets the same as they are under current law, but the bills would increase the marginal tax rate for every bracket except the first one, beginning with deaths on Jan. 1, 2025.

Currently, the estate tax rate ranges from 10% to 20%. The marginal tax rate for the top bracket—taxable estates of at least $9 million—is 20% under current law and would increase to 35% under the bills. According to the Tax Foundation, Washington and Hawaii currently have the nation’s highest marginal estate tax rate.

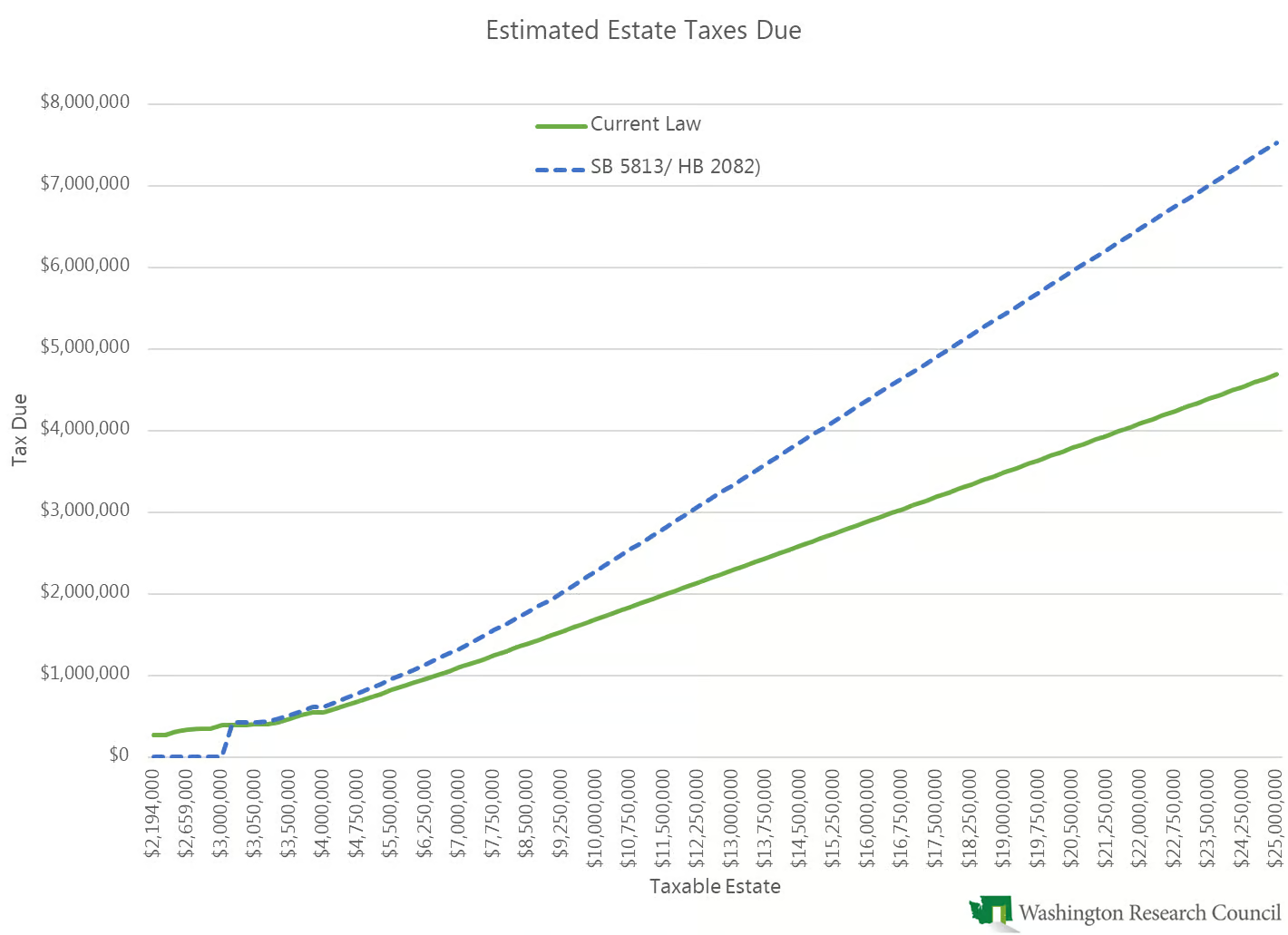

Additionally, under current law, $2.193 million may be excluded from the estate tax. By statute, the exclusion amount is supposed to be adjusted for inflation annually. This has not happened since 2018, because the statute ties the inflationary adjustment to a defunct index. SB 5813 and HB 2082 would increase the exclusion amount to $3.0 million for deaths occurring in calendar year 2025. Beginning in CY 2026, the exclusion amount would be adjusted for inflation, using the consumer price index for all urban consumers for the Seattle metropolitan area.

All told, the bills would reduce estate taxes for taxable estates between $2.193 million and $3 million. Taxes would increase for all estates of at least $3 million. For example, a $10 million taxable estate would pay $590,000 more under the bills than under current law. A $100 million taxable estate would pay $14.1 million more under the bills than under current law.

Tags: 2025-27