11:35 am

February 12, 2025

State revenues for funds subject to the outlook (NGFO) are currently expected to increase by $5.040 billion from 2023–25 to 2025–27. The estimated budget problem for 2025–27 is the result of legislative spending choices. Nevertheless, several tax increases have been introduced in the Legislature and proposed by former Gov. Inslee and the Senate Democratic Caucus. (I wrote about the various ideas in previous posts: B&O tax increases, payroll tax, wealth tax, capital gains tax, property tax growth limit, real estate excise tax, and new taxes on self-storage units and firearms.)

Assuming the revenue estimates are correct (this is especially questionable with the wealth tax), seven of the tax proposals would be Washington’s largest tax increases in over 30 years (at least).

This analysis is based on the estimated revenue from the tax increase in the first biennium in which it was to be fully implemented, and it uses the revenues estimated at the time the legislation was adopted (adjusted for inflation).

I reviewed Department of Revenue summaries of enacted tax legislation (available to 2003), agency fiscal notes (available to 2001), and legislative budget notes from the Legislative Evaluation and Accountability Program (available to the late 1970s, but the fiscal estimates for new tax legislation is spotty earlier than 2001). The earliest tax increases for which there is publicly available, relatively reliable fiscal impact information are from 1994.

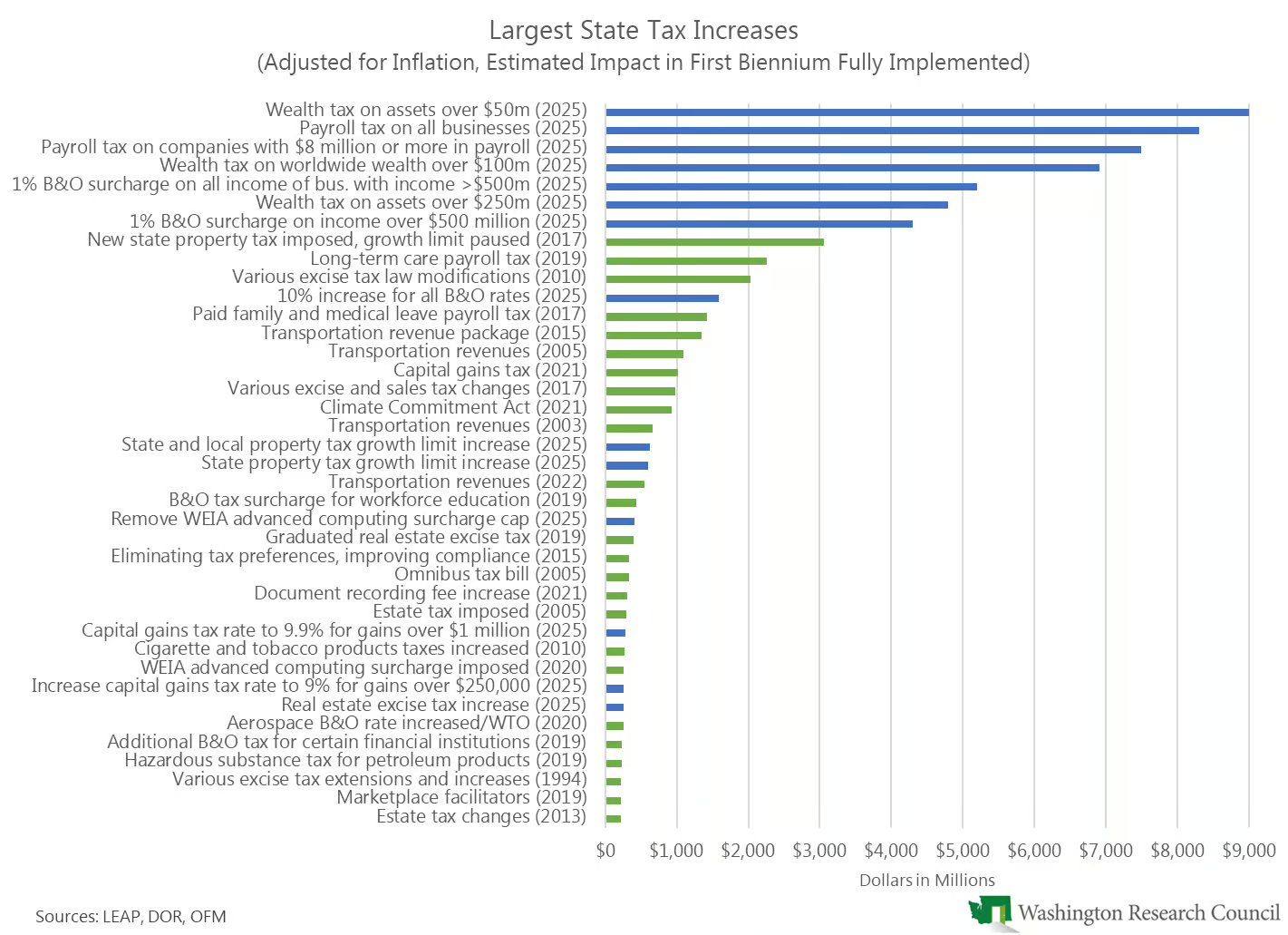

The chart shows the inflation-adjusted tax increases since 1994 that have exceeded $200 million. The years shown are the year of enactment; the blue bars are the taxes being considered this year. I’ve included transportation revenue packages (which include both taxes and fees) and document recording fees (which are used for homelessness programs).

The largest tax increase that has been enacted is the second property tax (and pause of the property tax growth limit) that was adopted in 2017. Adjusted for inflation, that bill was estimated (in 2017) to increase revenues by $3.056 billion in 2019–21. Seven of the new taxes under consideration would considerably exceed the revenue from that largest tax increase:

- Wealth tax on assets over $50 million, by 194.5%

- Payroll tax on all businesses, by 171.6%

- Payroll tax on companies with $8 million or more in payroll, by 145.5%

- Wealth tax on worldwide wealth over $100 million, by 126.2%

- 1% B&O tax surcharge on all income of businesses with income over $500 million, by 70.2%

- Wealth tax on assets over $250 million, by 57.1%

- 1% B&O tax surcharge on income over $500 million, by 40.7%

Note that the Senate Democratic Caucus tax ideas document had estimated that increasing the state and local property tax growth limit to a maximum of 103% would increase revenues in 2027–29 by $329 million. Now, a fiscal note has been published for HB 1334, which would increase the state and local limit to 100% plus population change and inflation, up to 103%. It estimates that the bill would increase revenues by $618.0 million in 2027–29. (Similarly, HB 1356, which would make the same change, but for the state only, is estimated to increase revenues by $602.4 million in 2027–29.)

Finally, I also considered the inflation-adjusted revenue estimates for each tax increase as a percentage of the total revenues expected at the time. When total revenues were significantly lower, a smaller tax increase would have a bigger impact. In most cases, using this measure (instead of the absolute value) doesn’t move the tax increases around that much. However, the 1% B&O surcharge on taxable income over $500 million would increase NGFO revenues by 5.60% but the 2017 property tax changes were estimated to increase NGFO revenues by 5.61%. Thus, in terms of the percentage increase to underlying revenues, six of the taxes proposed this year would exceed the 2017 state property tax increase.

Categories: Tax Policy.Tags: 2025-27