2:10 pm

January 23, 2025

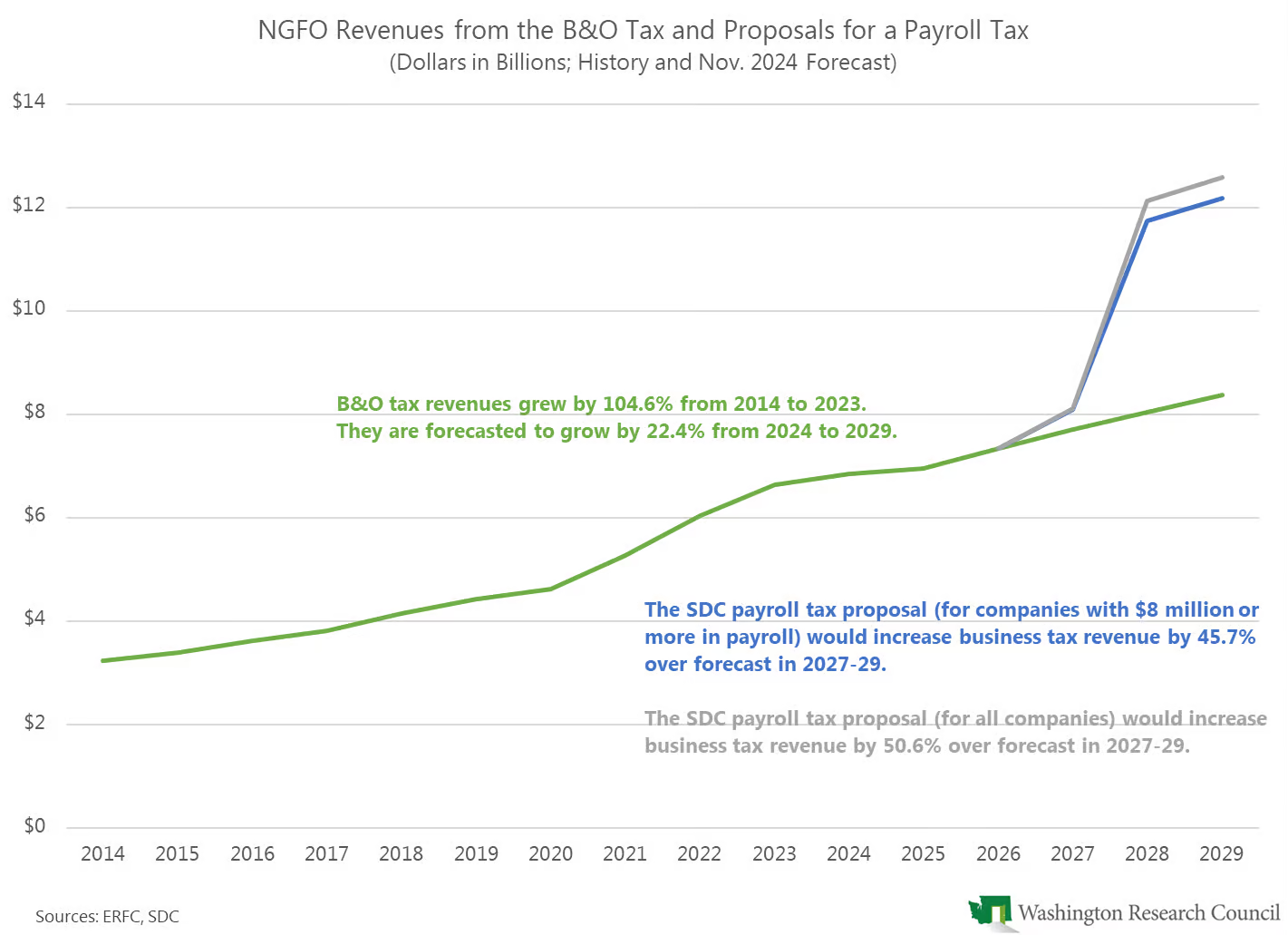

Some revenue options being considered by the Senate Democratic Caucus (SDC) were made public last month. (I wrote earlier about their business and occupation tax ideas.) The largest tax on employers on their list is a payroll tax of 6.2%.

The tax would be paid by employers on the total compensation “paid to employees making above the Social Security threshold.” (It’s not clear from the description if the tax would be on all compensation to an employee making more than the threshold or on the portion paid above the threshold.)

Their main proposal would be to impose the tax on companies with $8 million or more in Washington payroll. They estimate that it would increase revenues by $380 million in 2025–27 and by $7.5 billion in 2027–29.

An alternative proposal would apply the tax to all businesses. This would increase revenues by an estimated $410 million in 2025–27 and by $8.3 billion in 2027–29.

Either version would be a massive increase in business taxes. Revenues from the business and occupation (B&O) tax are currently forecasted to be $16.417 billion in 2027–29. Compared to the Nov. 2024 B&O revenue forecast, revenues from the B&O tax plus the payroll tax would increase by 45.7% in 2027–29 (for the main proposal) or by 50.6% in 2027–29 (for the alternative proposal).

Removing a cap?

The SDC is framing this proposal as a way to “remove the cap on employer payroll taxes.” This seems to be an attempt to make the tax seem like a natural extension of taxes that are already paid. This framing is not an accurate description of the tax.

The SDC document states that the 6.2% rate is “similar to what employers already pay for Social security and PFML on compensation below that threshold.” That’s true for Social Security, but not for paid family and medical leave (PFML):

- Under federal law, there is a cap on the amount of earnings on which Social Security taxes are paid. The cap is adjusted annually for inflation; in 2025, it is $176,100. Employers and employees each pay Social Security taxes on that amount, at a rate of 6.2%.

- Washington’s PFML program is also funded by a payroll tax on employees and employers. The tax is paid on earnings up to the Social Security cap, but the total rate is 0.92%. In 2025, employers pay 28.48% of the tax and employees pay 71.43%.

Imposing a 6.2% payroll tax on compensation paid to employees making above the Social Security cap would not constitute removing the cap. First, it’s not clear that the state tax would be only on the amount of compensation above $176,100. Second, the additional money would not go to the Social Security program, and there’s no indication from the SDC document that any additional funding would go to the PFML program. Instead, this is a new tax that would most likely be used for general spending programs.

The SDC also says that the proposal “is similar to Seattle’s JumpStart payroll tax.” We wrote about the highly concentrated and volatile nature of Seattle’s payroll expense tax (PET) here. In 2025, businesses are subject to the PET if they have total Seattle payroll expense of at least $8.8 million and at least one employee with annual compensation of at least $189,371. (The tax is applied to all compensation, not just the amount over the threshold.) The tax rate varies from 0.746% to 2.557%, depending on the business’s payroll expense and the amount of the employees’ compensation.

There is no public bill language yet. Aside from technical questions about, for example, what income it would apply to and how it would interact with Seattle’s tax, Legislators should consider how such a tax would affect Washington’s competitiveness. (The business tax burden in Washington is already above the national average, and Washington’s tax competitiveness already ranks sixth worst in the country.) Additionally, given the volatility of the tax, the state would need to increase reserves for budget sustainability purposes.

Categories: Tax Policy.