1:14 pm

October 1, 2019

The Pension Funding Council (PFC) met yesterday to discuss pension funding recommendations from the state actuary. Currently, in determining pension contribution rates, the actuary assumes that state investments will yield a 7.5 percent rate of return. In 2011, the investment rate of return assumption was 8 percent. Since then, the Legislature has stepped it down to more accurately reflect the level of risk. The higher the rate of return, the fewer contributions need be made to cover promised future benefits, but there’s no guarantee what the rate of return will be in any given year. (See our 2011 and 2012 reports on the topic for more.)

Yesterday, the state actuary recommended that the state reduce the rate of return assumption to 7.4 percent. Doing so would increase general fund–state (GFS) spending by $100.5 million in 2021–23 and by $100.4 million in 2023–25. Although state costs would increase now, taking this action would save money over the long-term. The actuary said that it would improve “the stability of future pension costs.” (Note that the actuary recommended 7.4 percent in 2017 as well. Instead, the PFC adopted the 7.5 percent rate and included a statement in the adopted motion “that the long-term Annual Investment return assumption adopted here be considered a step toward the recommendation of the State Actuary to reduce the Annual Investment Return assumption to 7.40%.”)

Senators Rolfes and Braun wanted to adopt the recommendation, but Representatives Ormsby and Stokesbary argued against it. Given the possibility of a recession in the next few years, they expressed caution about preemptively dedicating state funds when they might be needed for something else. David Schumacher, the director of the Office of Financial Management, suggested that deciding the question right now—a year ahead of when the Legislature will be determining the 2021–23 budget—would be premature.

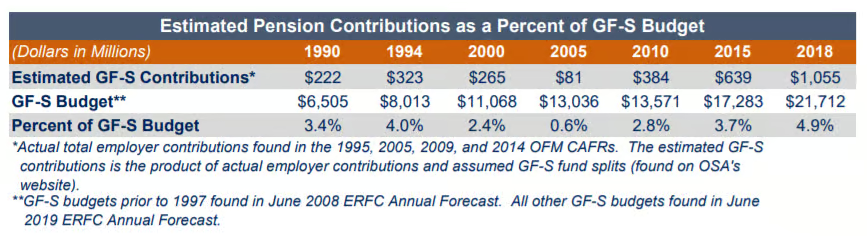

Additionally, the actuary’s office released the 2019 Report on Financial Condition and Economic Experience Study this summer. It includes information that was used in making its recommendation. It reports the positive news that pension contribution rates have been increasing since 2009–11. (However, 2019–21 “showed slowing growth and even decreases for some systems.”) Contribution rates have been increasing because there was underfunding in the past, plan members are living longer, and expectations for future investment returns have decreased.

Washington’s pension plans are 86 percent funded, as the chart below shows. The report notes, “The actuarial community has not agreed on a funded ratio threshold that determines a plan as ‘healthy’; however, we consider all open plans as well as LEOFF Plan 1 on target for full funding.”

All told, “the recent adoption of adequate contribution rates to cover the increasing longevity of members and the lower assumed rate of investment return has put the retirement systems in a better position for the future.”

Going forward, the report expects “both the contribution rates and the estimated GF-S pension contributions as a percent of GF-S will improve affordability since we expect contribution rates to decline to long-term levels.” In particular, “employer contributions will decline once PERS 1 and TRS 1 reach a fully funded status, which is projected to occur in FY 2026 for TRS 1 and in FY 2028 for PERS 1.”