12:21 pm

May 7, 2026

The workforce education investment account (WEIA), created in 2019 and overhauled in 2020, is a fund subject to the outlook. Revenues may be used for “higher education programs, higher education operations, higher education compensation, state-funded student aid programs, and workforce development including career connected learning.” Certain business and occupation (B&O) tax dollars fund the WEIA.

New data from the Department of Revenue (DOR) shows that one revenue source, the advanced computing surcharge, is paid by just 50 taxpayers.

Workforce education investment surcharge (also known as the advanced computing surcharge)

The first source of revenues for WEIA is a workforce education investment surcharge that is imposed on “select advanced computing businesses.” These are businesses that are members of an affiliated group in which at least one member is engaged in advanced computing. The affiliated group must also have annual worldwide gross revenue of more than $25 billion to be subject to the surcharge.

“Advanced computing” is defined as “designing or developing computer software or computer hardware,” including:

- Modifications to computer software or computer hardware,

- cloud computing services, or

- operating as a marketplace facilitator, an online search engine, or online social networking platform.

By statute, if a business is part of an affiliated group that has a member who is engaged in advanced computing, all business activities are subject to the surcharge so long as they are also subject to the B&O service and other activities rate or the new 3.1% B&O tax rate for payment card processing.

Statute specifies that “select advanced computing businesses” do not include:

- Commercial mobile service,

- Operation and provision of access to transmission facilities for wired telecommunications networks, or

- Financial institutions.

Further, regardless of whether a business is a select advanced computing business, the workforce education investment surcharge does not apply to health care provider clinics (as of July 1, 2022) or hospitals.

The workforce education investment surcharge is imposed on top of the B&O service and other activities 1.5% tax rate. Through Dec. 2025, the surcharge was 1.22% and the combined surcharge paid by members of an affiliated group was capped at $9 million a year. Beginning Jan. 1, 2026, the surcharge is 7.5% and the cap is $75 million a year. (These changes were part of ESHB 2081, which was enacted last year.)

Meanwhile, EHB 2487, adopted this year, specifies that if 50% or more of worldwide income of an affiliated group is from the payment of insurance premiums, then the annual cap is $25 million a year. Additionally, the bill specifies that the surcharge does not apply to insurers, health maintenance organizations, or health care service contractors that pay insurance premium taxes. These changes are retroactive, so the reduction of the cap is effective Jan. 1, 2026, and the exemption from the surcharge is effective Jan. 1, 2022. (According to the fiscal note for EHB 2487, “The tax impact resulting from the exemption changes to the ACS for insurers is negative; however, it is estimated to impact less than three taxpayers and cannot be disclosed.”)

All revenues from the workforce education investment surcharge are deposited in the WEIA.

Additional tiers for the B&O service and other activities tax rate

The second source of revenues for WEIA is a share of B&O service and other activities tax revenues. As part of the 2020 WEIA overhaul, a 1.75% service and other activities rate was added for businesses with $1 million or more in annual gross income that are not subject to the workforce education investment surcharge. Of the revenues from the 1.75% rate, 14.3% were directed to the WEIA.

ESHB 2081 added a third service and other activities rate tier. Beginning Oct. 1, 2025, the 1.75% rate applies to businesses with annual gross income of at least $1 million but less than $5 million. A new 2.1% rate applies to businesses with $5 million or more in gross income. Now, 14.3% of revenues from both the 1.75% rate and the 2.1% rate are directed to the WEIA. (The rate is 1.5% for businesses with less than $1 million in income, hospitals, and businesses that pay the workforce education investment surcharge.)

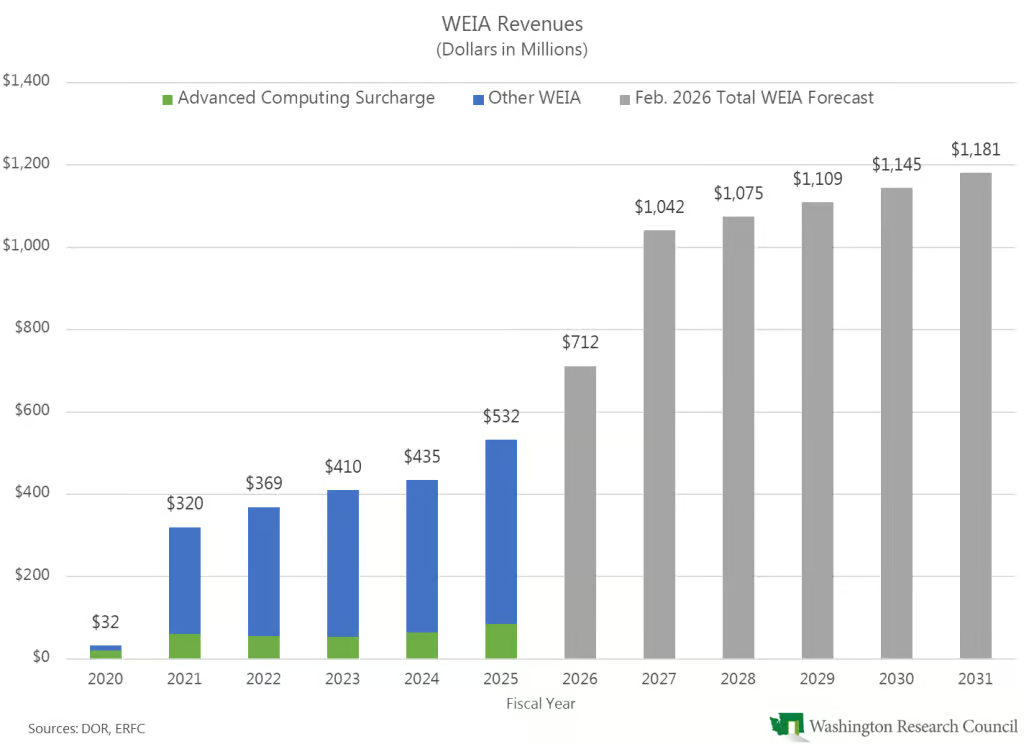

WEIA revenue history and forecast

In FY 2025, before the surcharge rate and cap increase, and before the addition of the 2.1% B&O rate, WEIA revenues totaled $532 million. Based on the Feb. 2026 revenue forecast, WEIA revenues are expected to be $1.042 billion in FY 2027 (the first fiscal year in which the rate and cap increases are effective for all 12 months).

The advanced computing surcharge has so far been a fairly small percentage of overall WEIA revenues. That is expected to change significantly as the higher surcharge rate and cap are reflected in collections. For example, in FY 2025, surcharge revenues were $84 million (15.9% of WEIA revenues). In 2025, DOR estimated that the surcharge rate and cap increase in ESHB 2081 would increase revenues by $394.4 million in FY 2027. At the time, DOR had estimated that the addition of the 2.1% B&O rate would increase WEIA revenues by just $70.7 million in FY 2027.

It’s not clear how the relative position of the two WEIA revenue sources may have changed in the Feb. 2026 forecast, but the surcharge could account for over 40% of WEIA revenues going forward. If DOR’s 2025 estimate holds, going forward, annual surcharge revenues alone would exceed total annual WEIA revenue collections in the pre-2025 years.

Who pays the advanced computing surcharge?

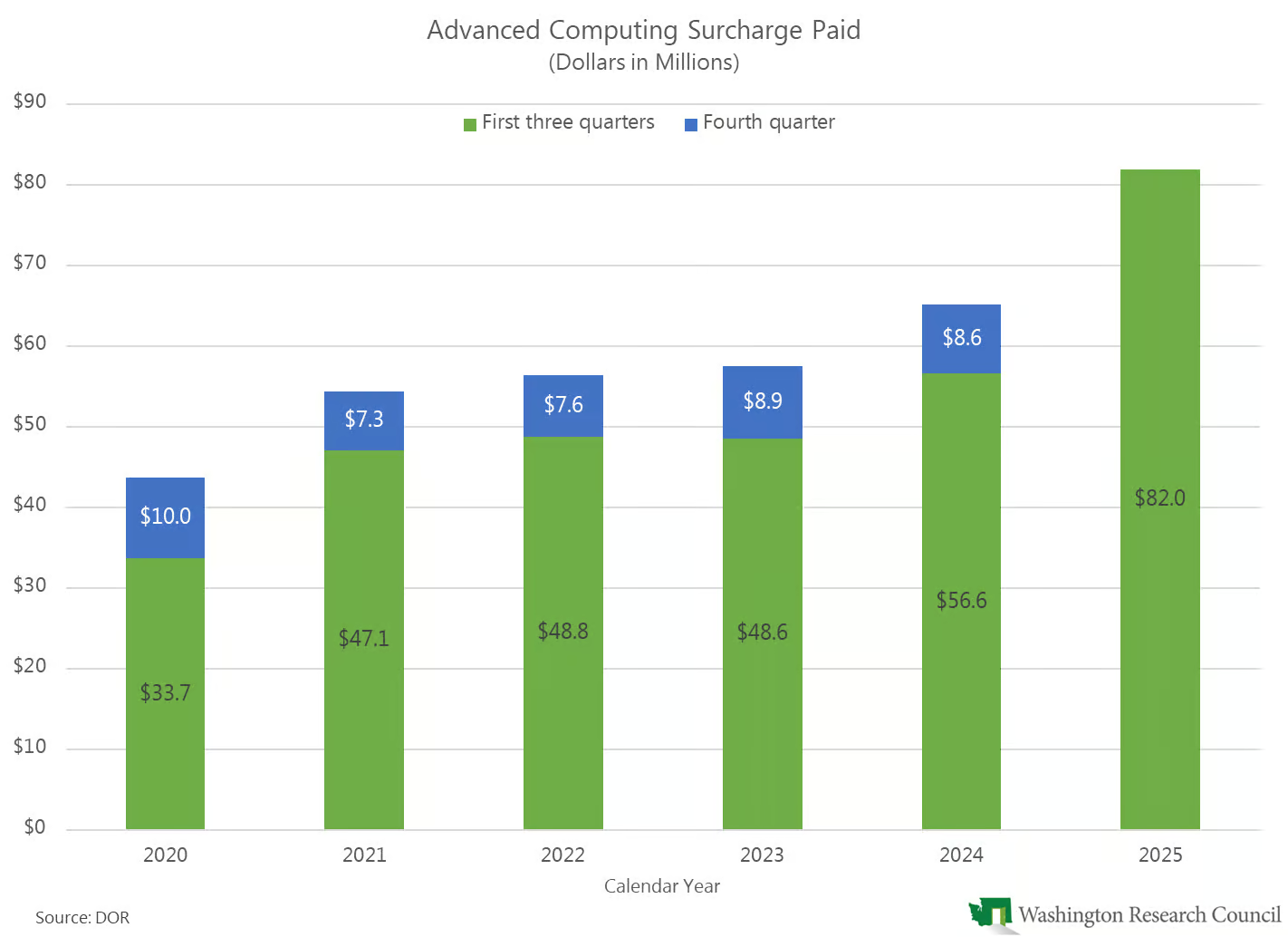

DOR has published quarterly revenues from the advanced computing surcharge through the third quarter of calendar year 2025. Taxes due increased substantially in 2025 compared to the same three quarters in prior years, and that’s before the increase to the surcharge rate and cap take effect.

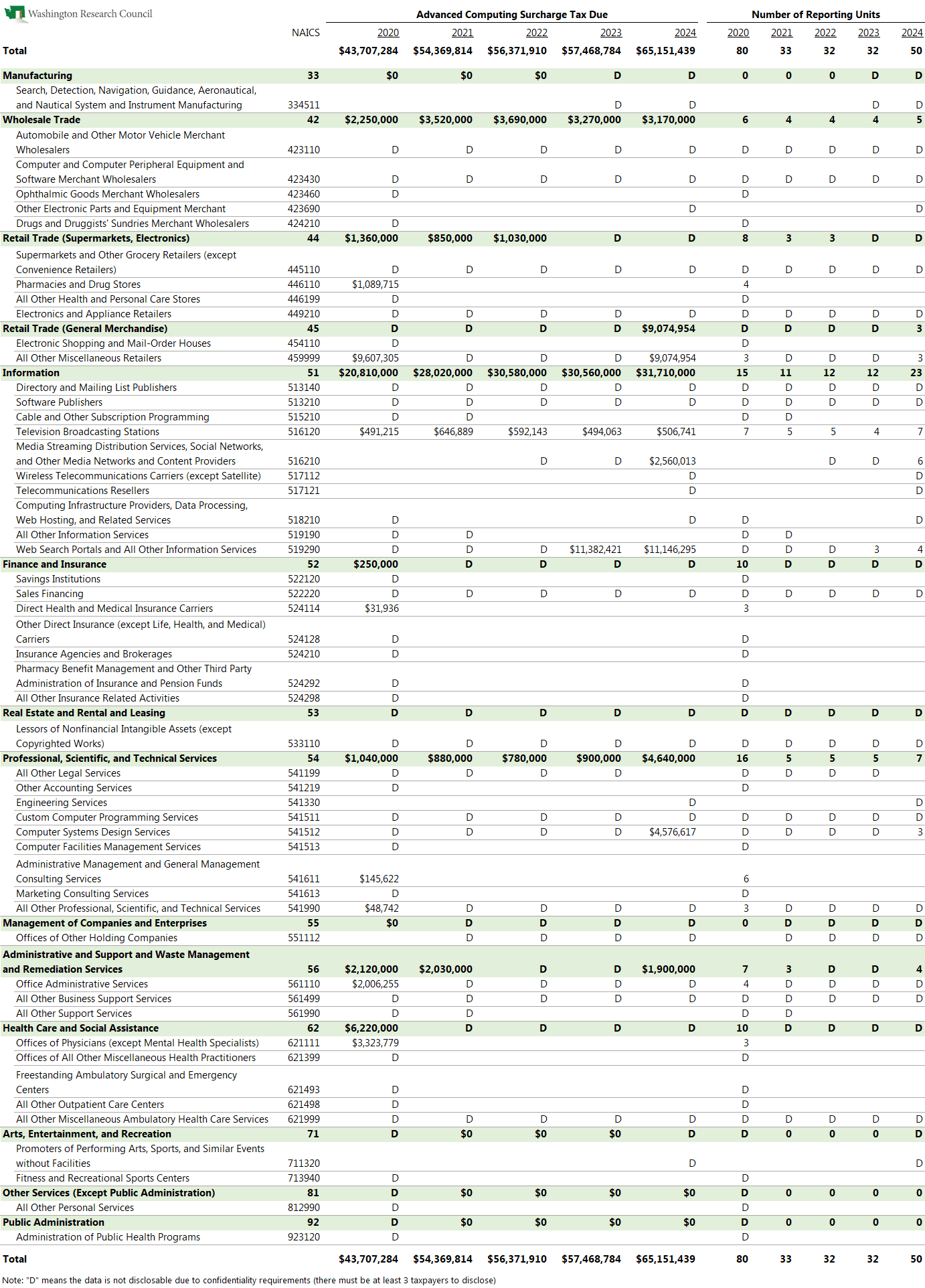

Published revenue data includes advanced computing surcharge taxes due and number of taxpayers by six-digit NAICS code. (In the DOR data, the taxpayer is the company that files the return; all members of an affiliated group count as one.) However, at the six-digit NAICS level, there are many industries for which these data cannot be disclosed because there are fewer than three taxpayers. Additionally, the published data does not include the total number of taxpayers each year.

DOR has provided me with some additional data for calendar years 2020, 2021, 2022, 2023, and 2024. (Again, these are all before the increases to the surcharge rate and cap take effect.) The new data shows the surcharge due and number of taxpayers by two-digit NAICS—by combining data into broader categories, more information is disclosable. (There is still a substantial amount of non-disclosable information.) DOR also provided the number of taxpayers constrained by the cap.

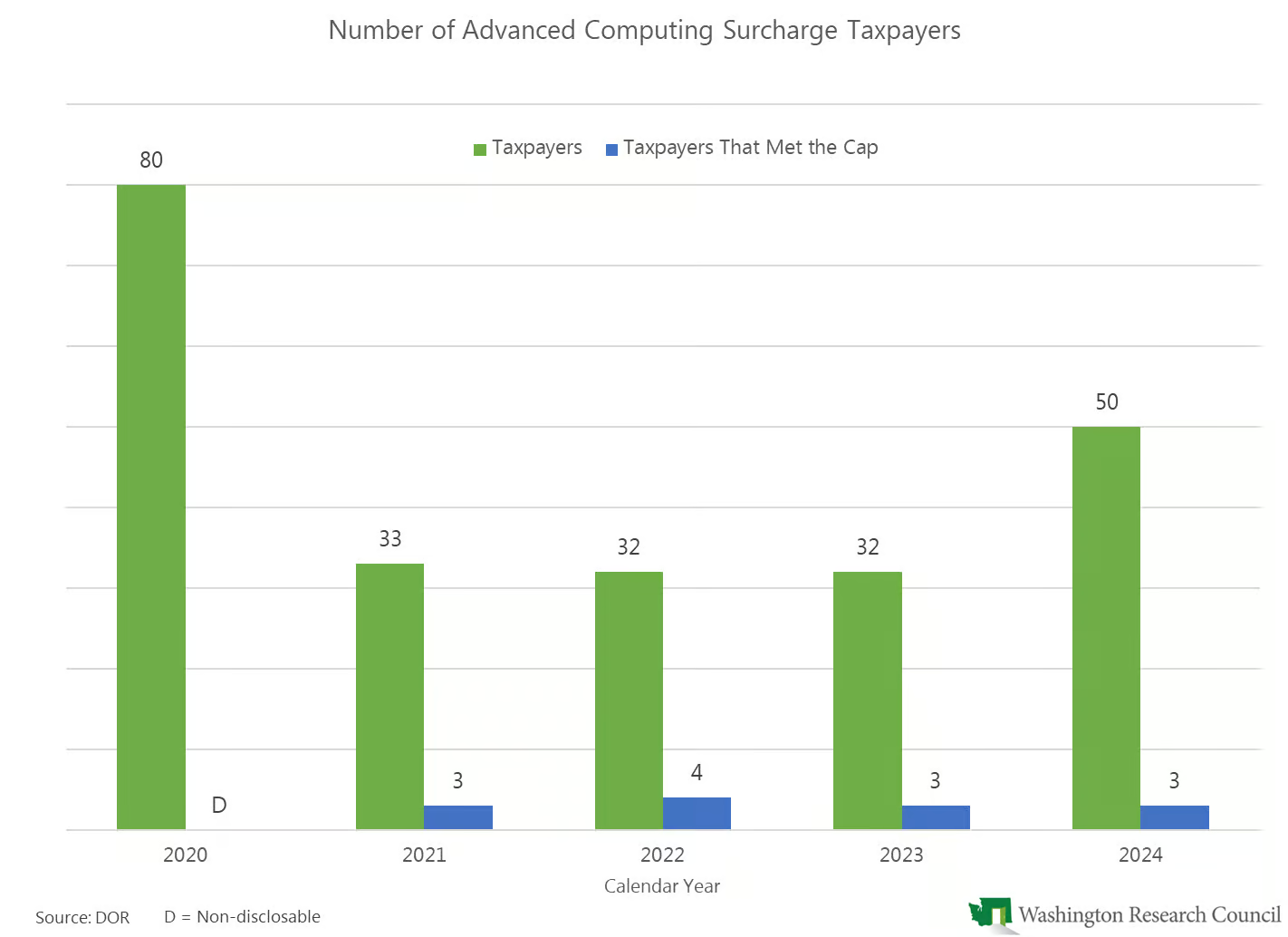

In 2020, there were 80 taxpayers, and the surcharges paid by fewer than three of them were constrained by the $9 million cap. In 2025, there were 50 taxpayers, and the surcharges paid by three of them hit the cap.

The table below combines data DOR gave me at the two-digit NAICS level with six-digit NAICS level data available publicly. (When there is a “D” in the table, it means that there are one or two taxpayers.) In 2024, the information sector had the most taxpayers (23) and the highest amount paid ($31.7 million). Of that, seven television broadcasters paid $506,741, and four web search portals and other information services paid $11.1 million. In 2024, three miscellaneous retailers (6.0% of the total number of taxpayers) paid $9.1 million (13.9% of the total surcharges collected).

Recall that to be subject to the surcharge, just one member of an affiliated group needs to be engaged in advanced computing. The reporting unit for the affiliated group in the DOR data is categorized by its primary NAICS code (even if the group has business activities across multiple NAICS).

Consequently, businesses in some perhaps unexpected industries are paying the advanced computing surcharge. For example, surcharge payers in 2024 included:

- At least one supermarket,

- At least one electronics and appliance retailer,

- At least one automobile wholesaler,

- Seven television broadcasters, and

- At least one promoter of performing arts, sports, and similar events.