11:54 am

December 7, 2020

In 2019, the Legislature created a new long-term care insurance program that will be paid for with a payroll tax (effective Jan. 1, 2022). This year, the Legislature passed a constitutional amendment, ESJR 8212, to enable the premiums to be invested, just as several other state funds are. Voters rejected the resolution last month.

As a consequence, premiums may need to be increased to maintain the solvency of the long-term services and supports account. Had the resolution passed, higher expected investment returns over the long run would have lessened the need for higher payroll taxes.

The Office of the State Actuary commissioned an actuarial study of the long-term services and supports account from Milliman in October that included estimates of what would happen if ESJR 8212 failed.

The long-term care statute specifies that the tax rate must be “no greater than” 0.58%. At the same time, “the pension funding council must set the premium rate at the lowest amount necessary to maintain the actuarial solvency of the long-term services and supports trust account.” In our policy brief on the payroll tax, we noted that these two requirements could be at odds.

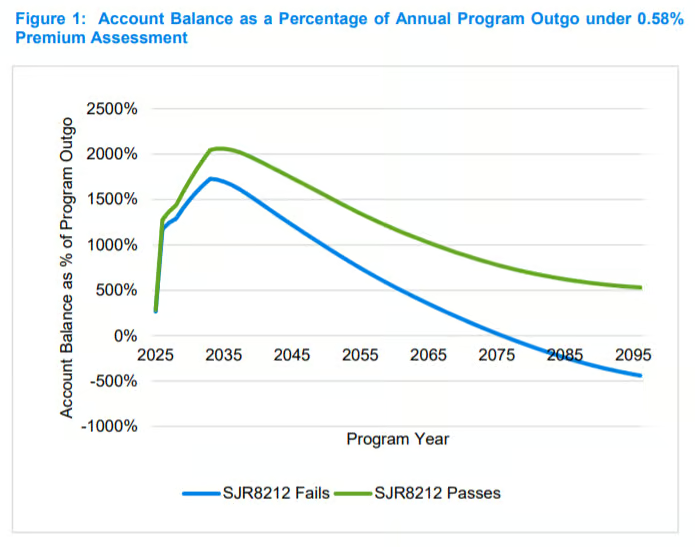

And lo, Milliman estimates that with the failure of ESJR 8212, the payroll tax will need to be between 0.64% and 0.69%. Further, “We project a 0.58% premium rate to be insufficient to keep the program solvent for 75 years if SJR8212 fails, as the program’s account balance decreases below program outgo for this scenario. Alternatively, the 0.58% assessment is sufficient under the scenario where SJR8212 passes.” (The chart is from the Milliman report.)

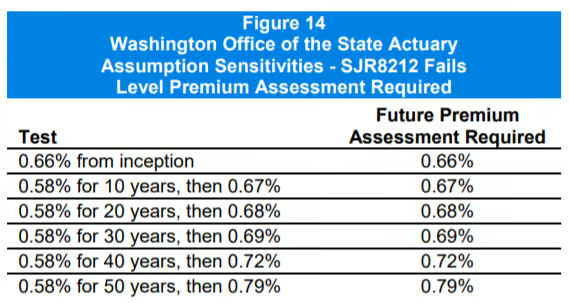

Milliman also writes, “The more years the program waits to ‘course correct,’ the higher the new premium rate is required to be to keep the program solvent through its remaining years.” The chart below illustrates what would happen to tax rates if the initially planned 0.58% rate is in place for various time frames, as opposed to jumping immediately to 0.66%.

According to Austin Jenkins of NW News Network, the state actuary said (after the election), “Put another way, in today’s dollars, the program is expected to require an additional $15 billion of revenue to cover the next 75 years of benefits and expenses.”

A draft report from the Long-Term Services and Supports Trust Commission notes that the failure of ESJR 8212

does not create an urgent need for action, as even at the 0.58% premium rate, Trust revenues are projected to exceed benefits for the first few decades of the program. But without the ability to secure higher investment returns, changes to various aspects of program design, such as benefit structure or eligibility, will be needed in the medium term to support the program’s long-term solvency.

The Commission met on Dec. 3 and agreed to ask the Legislature to pass the constitutional amendment and put it to voters again in 2021.

Categories: Tax Policy.