11:03 am

November 21, 2022

New data from the National Association of Insurance Commissioners (NAIC) show—unsurprisingly—that long-term care (LTC) insurance coverage jumped in Washington in 2021.

The 2019 legislation establishing the state’s LTC program exempted people with private LTC insurance policies from the state program. This provision was amended in 2021 to specify that individuals had to purchase private LTC insurance by Nov. 1, 2021 in order to qualify for an exemption. As we showed in a policy brief on the program last year, this deadline prompted a rush on the private LTC market. Ultimately, about 475,000 exemptions have been granted by the state.

The NAIC reports annually on private LTC coverage in the U.S. According to the most recent LTC insurance experience report, 319,647 Washingtonians had private LTC insurance at the end of 2021. That is an increase of 79.7% over 2020, when 177,922 had LTC insurance. (See chart 1.) The NAIC data include plans that are purchased individually and as part of a group. They include people with stand-alone LTC policies and people with life insurance or annuities that have LTC benefit riders. Of the policies included in the NAIC report, stand-alone policies accounted for 87.7% of total LTC policies in Washington in 2021.

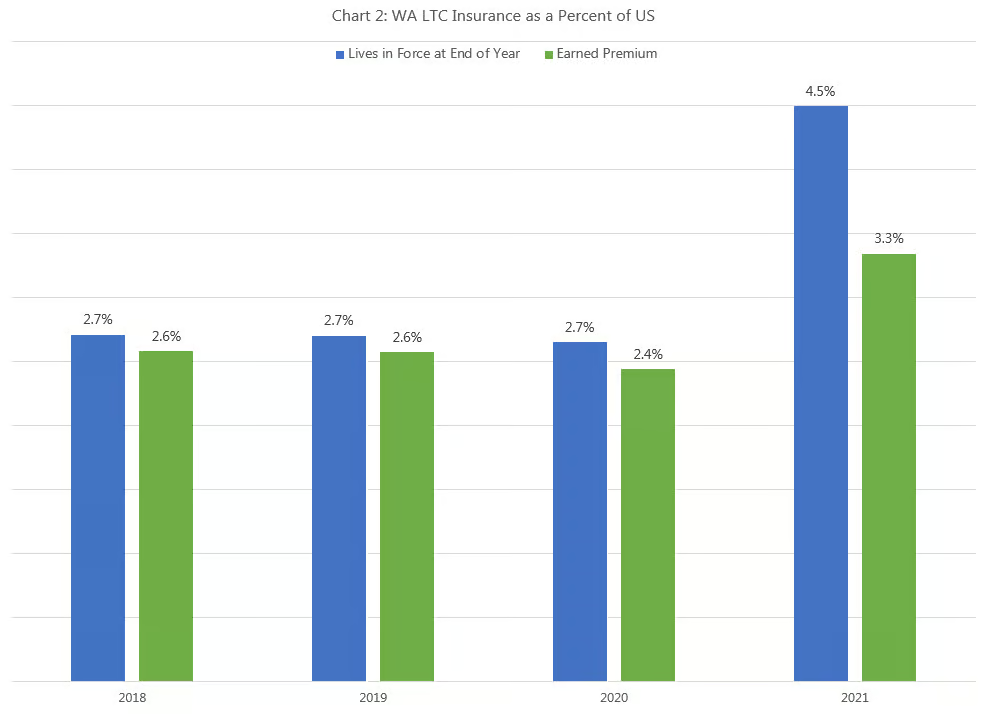

As a percent of U.S. LTC policies, Washington represented 4.5% of lives in force at the end of 2021 (up from 2.7% previously). Premiums paid on Washington LTC policies increased from 2.4% of the U.S. total in 2020 to 3.3% in 2021. That Washington’s share of premiums did not increase by as much as Washington’s share of policies suggests to me that Washingtonians chose lower-cost policies last year. (See chart 2.)

In 2020, among the states, Washington had the 14th highest number of people with LTC policies; Washington ranked 6th highest in 2021. (Adjusted for population, Washington ranked 22nd in 2020 and 5th in 2021.) Washington’s increase in policies in 2021 was by far the largest among the states, at 141,725. (The next largest increase was California’s 47,638.)

It is clear that private LTC insurance take-up increased dramatically in Washington last year. But the 319,647 policies reported by the NAIC is significantly lower than the 475,000 people who received exemptions from the state program. There is currently no requirement that exempted people provide proof of private insurance to the state. It is plausible that some people told the state they had private insurance when they didn’t, or that they purchased private insurance but dropped the policies before the end of the year, after receiving an exemption.

There’s another possible explanation for the discrepancy. The NAIC data may not include all life or annuity policies with LTC benefit riders: If the value of LTC benefits is less than 10% of the total benefits in the package, companies may assume that the LTC portion is “incidental” and not include it in the LTC experience report. For example, last year several organizations in Washington offered their employees LTC coverage as part of a life insurance plan with a LTC benefit through Chubb Insurance. (These included, e.g., the Washington Federation of State Employees and the City of Seattle.) But it does not appear that Chubb reported any such policies in the 2021 LTC experience report, suggesting that they considered the LTC portion of any policies to be incidental. Thus, it’s possible that people who purchased this sort of policy may not be included in the NAIC data, which could help explain the gap between the policies in the NAIC report and the number of exemptions from the state program.

Meanwhile, the 2022 supplemental operating budget required the Long-Term Services and Supports (LTSS) Trust Commission to make recommendations to the Legislature on various aspects of the state’s LTC program.

At the Nov. 10 meeting of the commission, it voted to recommend a requirement that people with exemptions “provide proof that they had purchased a qualifying LTC policy prior to 11/2021 and that they have maintained their policy through the present day.” The recommendation does not spell out what the consequences would be for people who cannot prove they have private policies, but the actuarial analysis of the proposal assumes that this group would simply be folded back into the state plan. (A workgroup considered and rejected an option that would have assessed a penalty on people who received exemptions but did not maintain their private coverage.)

Categories: Health , Tax Policy.