1:41 pm

October 25, 2022

In 2020, after passage of Washington’s long-term care (LTC) program but before any premiums were assessed, Milliman prepared an actuarial study of the program for the state. It estimated that the statutory premium rate of 0.58% would “be insufficient to keep the program solvent for 75 years under the current law.”

Given that and widespread interest in opting out of the program, the Legislature made several changes to the program earlier this year, including delaying its start by 18 months.

Milliman has now updated the 2020 study. The 2022 actuarial study accounts for changes made to the law by the Legislature, actual data on who has opted out of the program, and clarifications from the state as to program provisions.

The 2020 study had estimated that, given the constitutional limit on investing funds in stocks, the premium for the program would need to be between 0.61% and 0.71%. The estimated necessary premium range has dropped in the 2022 study. Now, Milliman estimates that the premium will need to be between 0.52% and 0.63%.

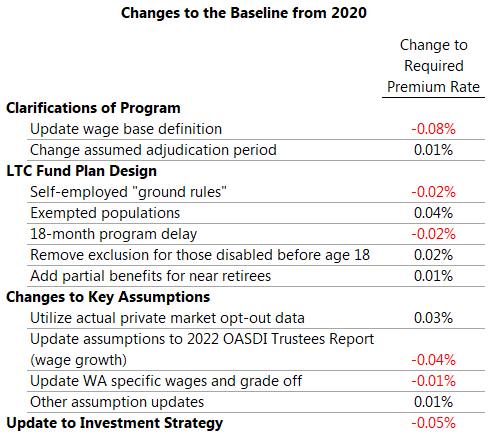

The table shows the impact of various policy and assumption changes since 2020. A few notes:

- The 18-month program delay reduces the required premium because wages are expected to increase over the period, but the starting level of benefits will be the same as originally planned.

- The actual data on private market opt-outs increases the premium because, overall, the people who opted out earn higher wages than the people who stayed in the program.

- A lower premium is needed because the 2022 study assumes higher investment returns than the 2020 study had, pursuant to the Washington State Investment Board’s recent investment strategy.

With a 0.58% premium rate, Milliman now estimates (given all the assumptions in the report) that the program would be solvent over the 75-year period. (However, the program would be insolvent at that rate under some scenarios.) According to Milliman, the estimates of the required premium are “highly sensitive to the underlying modeling assumptions.” The assumptions with the greatest sensitivity are the assumptions for wage growth and the consumer price index (CPI).

In recent years, wage growth has been 16% higher in Washington than in the nation. Milliman assumes this higher wage growth for the first 10 years and then removes the differential over the next 25 years. By year 35, the wages in the model match the national average wages. Milliman “chose to grade off the Washington-specific wage adjustment given Washington average income and nationwide average income have historically been closer together with the exception of approximately the last 10 years.” For the report, wages are assumed to grow by 3.55%. If wage growth is instead 4.77%, the necessary LTC premium would decrease by 0.17%. If wage growth is 2.35%, the premium would need to increase by 0.35%.

For CPI, Milliman used the long-term CPI estimate from the Office of the State Actuary (2.75%) for the first seven years, then graded it down to the national projection of 2.40%. If CPI is actually 0.5% higher, premiums would need to rise by 0.14%. If it is 0.5% lower, premiums could decrease by 0.10%.

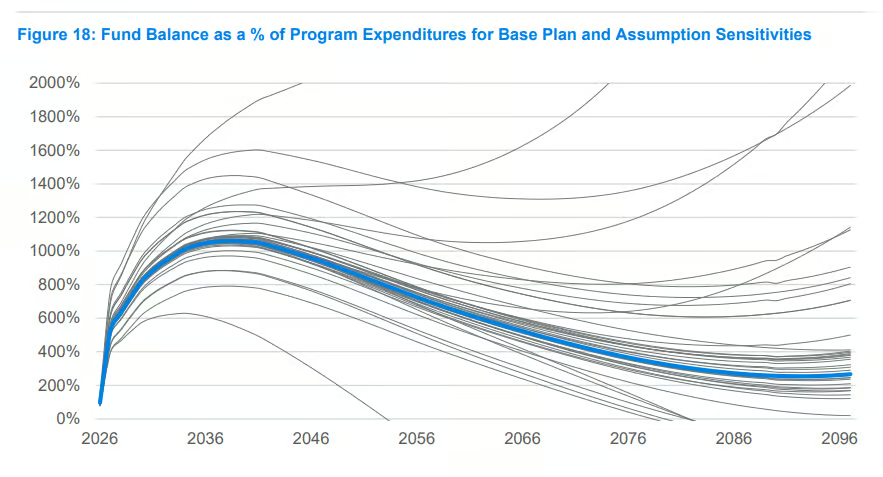

The chart below (from the 2022 report) shows the wide range of possible outcomes, given assumption sensitivities: “Many sensitivity tests are projected to have a positive fund balance throughout the 75-year window, while other tests result in depleted fund balances, including an extreme test where the fund balance is depleted in year 2054.” (The “base plan” in the chart assumes a premium of 0.57%.)

Altogether, this new actuarial report suggests that the premium rate set in statute may be sufficient to maintain solvency. That’s an improvement from the 2020 projections. Nevertheless, even at the 0.58% rate, the premium will be a significant tax increase for employees, as I wrote last week.

As we wrote last year, the state should reconsider this program before premiums begin to be assessed (currently scheduled for July 1, 2023). But if the program remains in law, the state should approve a constitutional amendment that would allow the program’s funds to be invested in stocks. (Voters rejected such an amendment in 2020.) This would help to prevent future tax increases because higher investment returns would improve solvency. The 2022 actuarial study estimates that, under a scenario in which funds could be invested in stocks, the required premium could be reduced by 0.03%.

Categories: Employment Policy , Tax Policy.