12:03 pm

November 13, 2024

A bill has been introduced in Seattle City Council to impose a 2% capital gains tax on the sale or exchange of long-term capital assets. The bill is being discussed today as part of Seattle’s budget process, and it looks like the Select Budget Committee could vote on it next week.

The bill is mostly identical to the state capital gains tax, aside from the tax rate. The Seattle bill would keep the same standard deduction and the same exemptions.

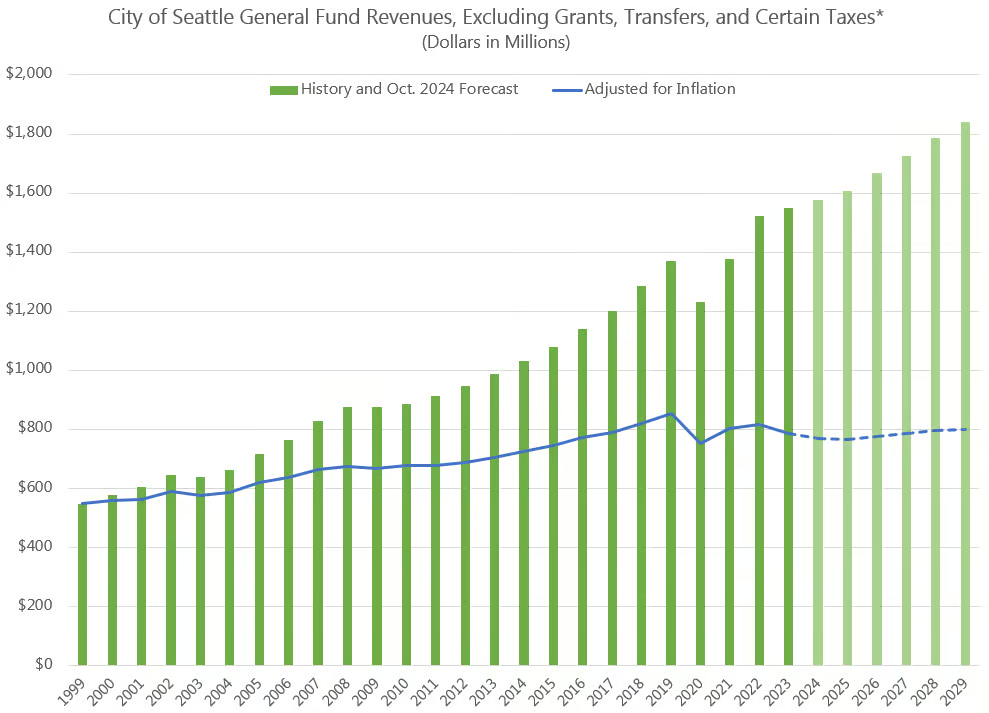

If adopted, the Seattle capital gains tax would take effect Jan. 1, 2026. Seattle’s Office of Economic & Revenue Forecasts (OERF) estimates that the tax could increase city revenues by $16 million to $51 million a year. For context, general fund revenues (excluding grants, transfers, payroll expense tax, admission tax, short term rental tax, and sweetened beverage tax) were $1.551 billion in FY 2023. (See the chart below.)

According to the OERF, in 2023, 816 taxpayers in Seattle paid the state capital gains tax. Of those, the top 20% paid 85.7% of the state capital gains tax revenues paid by taxpayers in Seattle. As the OERF notes, “These findings highlight the fact that the capital gains tax is extremely heavily concentrated and strongly affected by the decisions of a very limited number of taxpayers.”

Indeed, “A 2% Seattle city tax on top of the Washington State 7% tax and the progressive federal tax with rates of 15%/20%/28% would imply a 6.5% to 9% increase in tax burden (depending on the capital gains amount and thus the federal tax rate).” Consequently, taxpayers “may be motivated to move and relocation is easier between local jurisdictions than moving out of state or to a different country. The long term effect of the tax on economic activity in city will likely be negative, but it’s hard to quantify.”

The fiscal note for the bill adds, about the $16–$51 million estimated range, “it does not contemplate a more drastic scenario where all otherwise eligible taxpayers avoid the tax by way of declaring a domicile outside the City, but this is clearly a risk for a tax imposed at a municipal level.”

Altogether, the OERF notes, “revenues from capital gains tax imposed in Seattle city are very likely to fluctuate significantly for year to year and from forecast to forecast.” To address the volatility of capital gains taxes, jurisdictions should save some revenues in good years in order to smooth out spending in years when revenues are lower.

Under current law, the City must deposit 0.5% of general fund tax revenues into the revenue stabilization fund. Additionally, the City transfers 50% of any unplanned year-end general fund balance to the revenue stabilization fund. The revenues from the proposed capital gains tax would go to the general fund, so they would feed into the reserve fund. That said, if the capital gains tax is adopted, the City may want to increase reserve targets to account for the increased volatility of the tax code.

A separate bill being considered by the City Council states that capital gains tax revenues would be used “to support rental assistance to rent burdened households, down payment assistance to low, moderate, and workforce households, and food assistance to food insecure households.” More specific allocations would be made by future resolution or budget.

The Seattle Metropolitan Chamber of Commerce has more on the city’s budget and recent tax increases here.