10:52 am

November 14, 2024

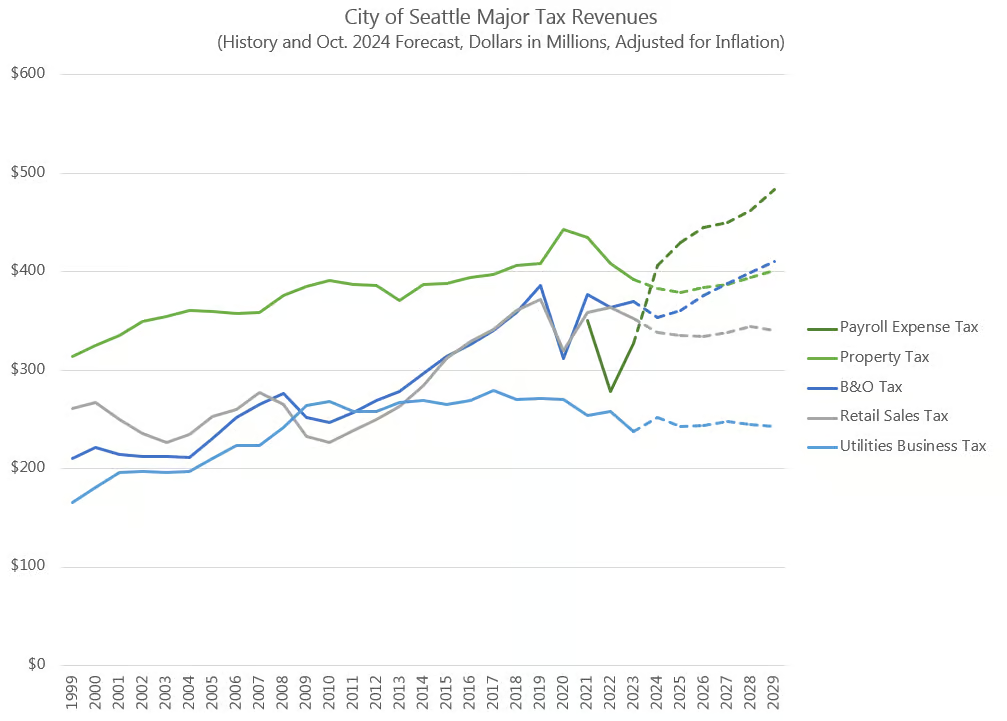

A bill (CB 120912) has been introduced in the Seattle City Council that would make several changes to the city’s payroll expense tax (PET). We wrote in detail about the tax, which is highly concentrated and volatile, in a policy brief last year.

The tax is levied on compensation paid in Seattle to employees, and the tax rate varies based on the company’s total Seattle payroll expense and the amount of an employee’s compensation. Businesses with higher total payroll expense pay higher rates, and businesses pay higher rates on employees with higher compensation. Since we published our policy brief, the Seattle City Council increased the rates. Beginning in 2024, the tax rate ranges from 0.746% to 2.557%. (Before, the rates ranged from 0.7% to 2.4%.)

In the first three years of collections, the PET was the city’s fourth-largest tax source. In 2024 and thereafter, Seattle’s Office of Economic and Revenue Forecasts (OERF) estimates that the PET will be the city’s largest tax source.

As originally imposed, the PET is scheduled to sunset on Dec. 31, 2040. The bill that is now being considered by the City Council would make the PET permanent.

CB 120912 would also repeal the current PET oversight committee, which, according to the bill’s fiscal note, has never met. Note that the Mayor’s proposed budget would appropriate $100,000 for an evaluation of the programs supported by the PET and the tax’s impacts on jobs and businesses in Seattle. (A proposed amendment would remove this funding—see page 12 here.)

Additionally, CB 120912 would add new allowable uses for PET revenues, including contributions to a new “Payroll Expense Tax Revenue Stabilization Account” (PET RSA). Recognizing the volatility of the tax, the PET RSA “is intended to cushion the City from unanticipated shortfalls in Payroll Expense Tax revenues.” The proposed bill would set a target PET RSA balance of 10% of forecasted revenues.

Having a reserve would improve the sustainability of budgets relying on the PET. As the OERF said in its presentation of the October revenue forecast, there is a “high level of uncertainty regarding payroll expense tax revenue estimates,” reflecting “the underlying tax base uncertainty due to stock price movements as well as forecasting uncertainty due to short collection history.”

Categories: Tax Policy.