1:43 pm

July 2, 2020

Yesterday the Select Budget Committee of the Seattle City Council approved the “payroll expense tax” introduced by Councilmember Mosqueda. (I wrote about the original proposal here.) According to the Seattle Times, the full council will vote on the proposal on Monday.

The budget committee also approved the spending plan associated with the tax, with amendments. It did not act on the proposal to make appropriations from the emergency fund and revenue stabilization fund for 2020 (which would be repaid later with proceeds from the new tax).

Kevin Schofield of Seattle City Council Insight reports that four amendments to the tax ordinance were adopted. (The text of the ordinance on the Council’s website has not yet been updated to reflect these changes.) The amendments added a tier to the tax, removed the sunset clause (originally the tax would have expired Dec. 31, 2030), changed the “maintain a level playing field” provision, and added to the definition of “compensation.”

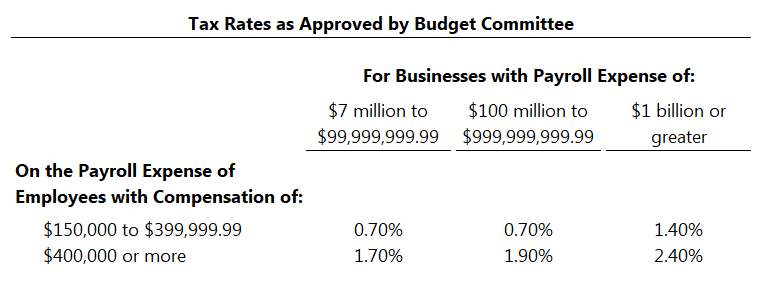

With the amended tax rates (see the table), the revenue estimate increased from $173.5 million to $214.3 million in 2021.

The original proposal included a provision on “maintaining a level playing field,” which stated, “The City intends to work with King County and the State of Washington to consider amendments to the tax . . . in the event that businesses become subject to future significant progressive taxes at the county or state level.” As amended, the provision reads,

To maintain a level playing field and to provide predictability for the businesses impacted by the payroll expense tax . . . the Council intends to monitor proposals for any taxes imposed by King County or the State of Washington to ensure: a) businesses in its jurisdiction are not subject to additional payroll taxes imposed [by the City], b) filings are consolidated and streamlined to reduce administrative burden on taxpayers and Finance and Administrative Services, and c) a sustainable, progressive funding source is maintained for the items [in the spending plan].

While this suggests that the Council would repeal or reduce the city tax if a county or statewide one is enacted, the language does not require it to do so.

The definition of “compensation” was originally “remuneration as that term is defined in RCW 50A.05.010.” The amendment added “net distributions, or incentive payments, including guaranteed payments, whether based on profit or otherwise, earned for services rendered or work performed, whether paid directly or through an agent, and whether in cash or in property or the right to receive property.”

The Seattle Times reports that Mayor Durkan “worries a new Seattle tax could cause companies to relocate elsewhere in King County.” Further, a spokeswoman said the mayor “doesn’t think City Council should expedite one of the largest taxes ever proposed in Seattle, especially in the midst of an economic downturn not seen since the Great Depression.”

Categories: Tax Policy.