12:10 pm

June 16, 2021

Although the state did not have a budget shortfall to address this year, the Legislature raised taxes (including a new capital gains tax) and drained the rainy day fund. It also significantly increased spending.

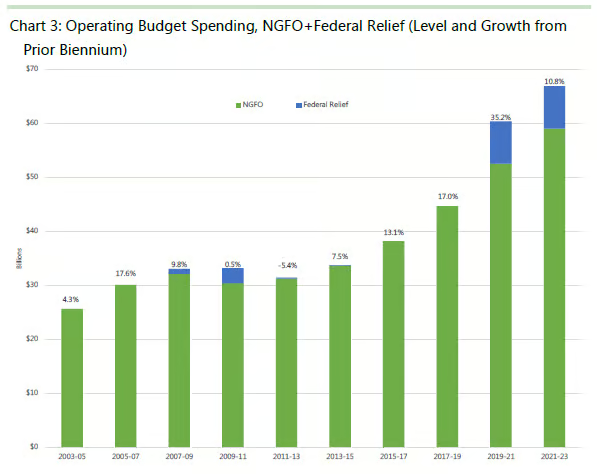

The enacted 2021–23 operating budget (including vetoes) appropriates $59.067 billion from funds subject to the outlook, an increase of 12.4% over revised 2019–21 appropriations. In addition, the state has appropriated or allocated $15.749 billion of federal relief funds over 2019–21 and 2021–23.

The budget passed by the Legislature balances over four years. But there are seven particularly troubling aspects of this budget:

- NGFO spending is increased substantially, even though federal relief money can be used to address many spending needs related to the pandemic.

- The budget uses one-time federal relief money to start a new child care and early learning program.

- The cost of the new child care program bow waves beyond the four-year budget outlook.

- The budget misses an opportunity to deal with the unfunded liability in the Teachers’ Retirement System plan 1 by merging two closed plans (though putting money toward the problem is better than nothing).

- It imposes a capital gains tax even as state revenues continue to rise beyond pre-pandemic levels and includes capital gains tax revenues in the balance sheet even though they may never materialize due to legal and ballot challenges.

- It drains the budget stabilization account (the BSA, or the rainy day fund), despite strong revenue growth and large amounts of federal relief.

- It creates a bad precedent in moving BSA funds to an unrestricted “shadow” reserve account.

These actions call into question the sustainability of the budget. By acting as if there was a budget problem this year, legislators may have created challenges for the years ahead.

Read the report here.

Tags: 2021-23