1:30 pm

April 29, 2022

The U.S. District Court for the Western District of Washington has dismissed the class action lawsuit that asked the Court to find the state’s long-term care program (WA Cares) “unlawful and unenforceable under ERISA, federal, and state law.” (The link to the ruling is via this AP story.)

The Court held that it does not have jurisdiction in the case because WA Cares is “not governed or preempted by ERISA” and because it involves a state tax, which much be challenged in state courts (pursuant to the federal Tax Injunction Act).

One factor in determining whether the WA Cares premium is a tax subject to the Tax Injunction Act is the ultimate use of the assessment. Is it “expended for general public purposes, or used for the regulation or benefit of the parties upon whom the assessment is imposed”?

In answering that question, the judge makes some unexpected points.

The Court writes,

WA Cares premiums are mandated by the Washington Legislature, as opposed to an agency or commission with delegated authority, can be appropriated by the Legislature for another purpose (subject to the requirement that notice with statutorily-specified content be provided by mail to all qualified individuals, see RCW 50B.04.100(3)), and will be used to directly benefit all members of the public who paid premiums for the requisite period and meet the criteria for receiving LTC services.

So, the Court determined that the premiums are a tax in part because the revenues could be used for another purpose (not just for WA Cares benefits). In footnote 11, the Court adds,

Plaintiffs’ contention that WA Cares premiums may not be used for other purposes relies on a misinterpretation of RCW 50B.04.100(2), which states: “The revenue generated pursuant to this chapter shall be utilized to expand long-term care in the state. These funds may not be used either in whole or in part to supplant existing state or county funds for programs that meet the definition of approved services.” This provision does not preclude WA Cares revenue from being used outside the LTC arena; rather, it seeks to preserve other sources of LTC funding, like Medicaid, by prohibiting the use of WA Cares benefits as a substitute for them.

This is an interesting and (I think) novel point. My reading of RCW 50B.04.100 (sections 2 and 3) had been that the long-term services and supports (LTSS) trust account (in which the WA Cares premium revenues are deposited) must be used on long-term care programs (either WA Cares or another LTC program), but not on general state spending. The judge is suggesting that the state could also use LTSS moneys on non-LTC items, as long as the LTSS trust account funds the WA Cares benefits and funding for other long-term care programs is maintained.

Additionally, footnote 11 raises a point that had not occurred to me. RCW 50B.04.100(2) forbids the LTSS revenue from being “used either in whole or in part to supplant existing state or county funds for programs that meet the definition of approved services.” The footnote argues that this “seeks to preserve other sources of LTC funding, like Medicaid, by prohibiting the use of WA Cares benefits as a substitute for them.” If Medicaid LTC spending can’t be supplanted, then how can program proponents argue that WA Cares will save the state money by reducing Medicaid spending?

Which brings me to footnote 12 of the order, which states, “Plaintiffs argue that defendants identify only an ‘indirect’ benefit from WA Cares, namely ‘keeping a very small percentage of individuals off of Medicaid.’ Such benefit seems direct, not indirect, and characterizing the percentage as ‘small’ ignores the legislative findings underlying WA Cares.”

The footnote then lists several items from the bill’s findings section, including, “Based on caseload and demographic estimates, WA Cares is predicted to save the Medicaid program $898,000,000 in 2051–53.”

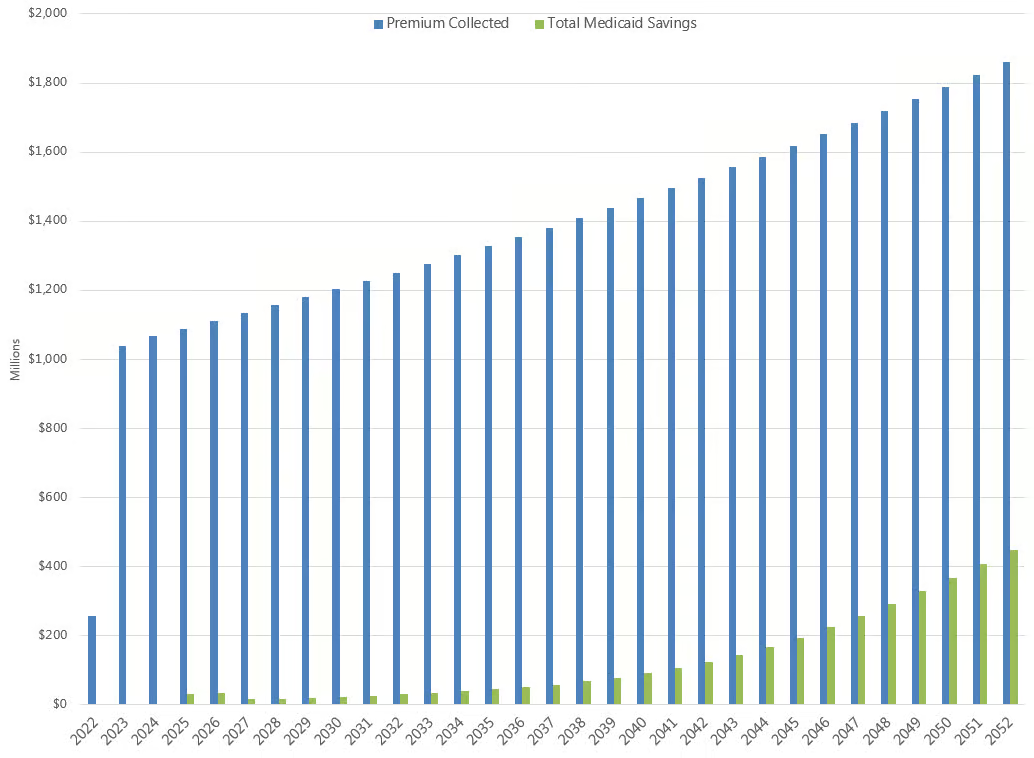

To be sure, $898 million is a lot of money (though half of such savings would go to the state and half would accrue to the federal government, unless they were to grant a waiver). However, as we wrote in a policy brief last year, the amount saved by Medicaid is “miniscule compared to state spending on long-term care and to the payroll taxes that will be collected.” The state had estimated that WA Cares would reduce Medicaid spending in Washington (both the state and federal share) by a total of $3.742 billion for the period from 2022 through 2052. For context, total long-term care spending in the current biennium is $8.588 billion, of which the state is responsible for $3.548 billion. Based on the fiscal note for the original LTSS bill, we estimated that total premiums paid from 2022 through 2025 would be $42.734 billion. (The chart below is from our brief.)

Finally, Richard Birmingham of Davis Wright Tremaine, the attorney for the plaintiffs, writes, “The dismissal shifts the litigation from the federal court to the state court and adds a new state law challenge of WA Cares: Is the WA Cares premium a state income tax assessed on employee wages and, therefore, unconstitutional under Washington state law?” His post lays out that potential argument.