1:57 pm

August 12, 2025

In November, Seattle voters will decide if city business and occupation (B&O) tax rates should be increased. The proposed rate increases would be on top of statewide B&O tax increases that were adopted by the Legislature this year and several other business tax increases adopted recently by Seattle.

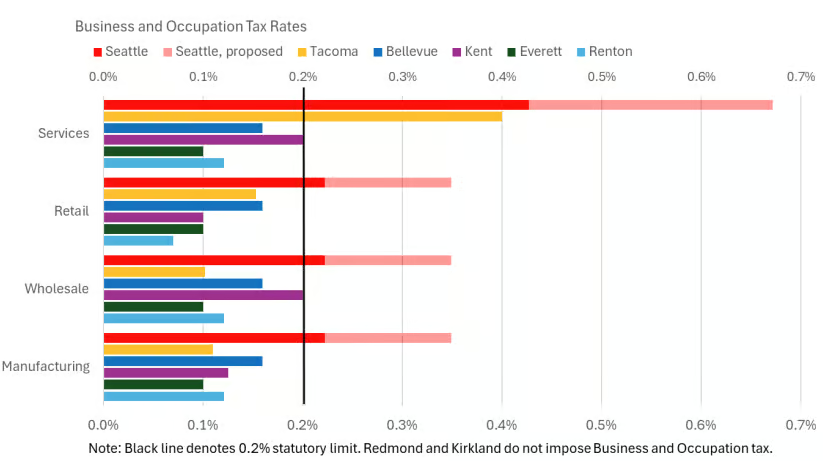

Currently, Seattle’s B&O tax rates are 0.222% for retailers, wholesalers, and manufacturers and 0.427% for services. The proposal would increase those rates to 0.342% and 0.658%, respectively, on Jan. 1, 2026. Then, on Jan. 1, 2033, the rates would be set at 0.273% and 0.526%, respectively. Thus, the rates would increase by 54% on Jan. 1, 2026. The 2033 rates would be 23% higher than rates today.

Meanwhile, the proposal would increase the threshold for owing B&O tax from $100,000 in gross receipts to $2 million. The proposal would also add a standard deduction of $2 million.

Mayor Harrell signed Ord. 127259 on August 4. (CB 121059, which makes a technical correction to the end date for the initial rate increase, is scheduled to be considered by the City Council today. This post assumes it is passed.) Under state law, cities may impose local B&O taxes of up to 0.2% (RCW 35.21.710). However, voters may approve B&O taxes at higher rates (RCW 35.21.711).

According to Seattle’s Office of Economic & Revenue Forecasts (OERF), taxpayers with taxable amounts of up to $2 million would owe $28.4 million in 2026 under current law. The remaining taxpayers would owe $32.8 million on the taxable amount up to $2 million under current law. If the proposal is approved, these amounts would no longer be collected. The proposed rates are estimated to be sufficient to maintain revenues at the level expected under current law (i.e., without the deduction and threshold increase), plus another $90 million.

However, an amendment was approved by the City Council that would exempt comprehensive cancer centers and pediatric hospitals from the rate increases. With that, according to the fiscal note, the proposal would increase general fund revenues by about $80 million a year through 2032. Beginning in 2033, the rates would decrease, but they would remain higher than they are currently in order to pay for the standard deduction and increased tax threshold.

The changes would dramatically reduce the number of businesses that pay city B&O tax, from “more than 22,000 to about 5,400,” according to the OERF. Further, as the OERF notes,

There is a significant overlap between the taxpayers subject to Payroll Expense Tax and the top taxpayers of the B&O tax. As a result of a higher concentration of B&O tax if the proposed changes are implemented, both revenue streams will be more closely tied to financial fortunes and decisions of a relatively small number of businesses. This would make B&O tax revenues more volatile and less predictable.

(We discussed the volatility of the payroll expense tax here.)

Additionally, although the proposed rate increases are substantial on their own, it’s important to consider the increases in the context of recent changes to business taxes in Seattle and the state. (Note, though, that businesses also pay property and sales taxes.)

- Seattle’s payroll expense tax was first imposed in 2021.

- Payroll expense tax rates were increased beginning in 2024.

- A new social housing tax was imposed on businesses in Seattle beginning in 2025.

- This year, the state Legislature increased many state B&O tax rates as part of ESHB 2081 and ESSB 5794 and added a temporary B&O tax surcharge for certain businesses. The state changes will largely take effect Jan. 1, 2026 and Jan. 1, 2027.

The OERF put together the chart below comparing Seattle’s current and proposed B&O tax rates to B&O tax rates in nearby cities. Given the significant proposed increases in Seattle, the city should expect the movement of some jobs and businesses out of Seattle. The OERF writes,

It is difficult to predict how large businesses will react to the cumulative impact of all these increases in tax burden, but several large employers have recently moved thousands of jobs out of Seattle, to some of the surrounding cities. A large increase in B&O tax rates could potentially further exacerbate this problem, which would then lead to negative downstream effects, lower job and income growth in the local economy, as well as lower B&O Tax, Payroll Expense Tax, and Sales Tax revenue growth in the coming years.

To summarize, under the proposal, a narrower tax base would pay a substantially higher tax rate than businesses face in neighboring cities. Jobs have already started moving out of Seattle. Although smaller businesses would pay less B&O tax under the proposal, would they still come out ahead if they lose some of their customer base as jobs move?