8:58 am

January 19, 2024

Yesterday the House Finance Committee heard a proposed substitute to HB 2276, which would increase a real estate excise tax (REET) threshold and add a new 1% real estate transfer tax.

As I wrote last week, the bill as introduced was ambiguous about whether the transfer tax applied to the portion of the selling price over $3.025 million or the entire selling price, if it is more than $3.025 million. The proposed substitute does not clarify the language. However, the Department of Revenue’s (DOR) preliminary fiscal note interprets the proposed substitute bill to mean that the transfer tax would apply to the portion of the selling price over $3.025 million. (That is, for a $3.5 million sale, the 1% transfer tax would apply to $475,000, not $3.5 million.)

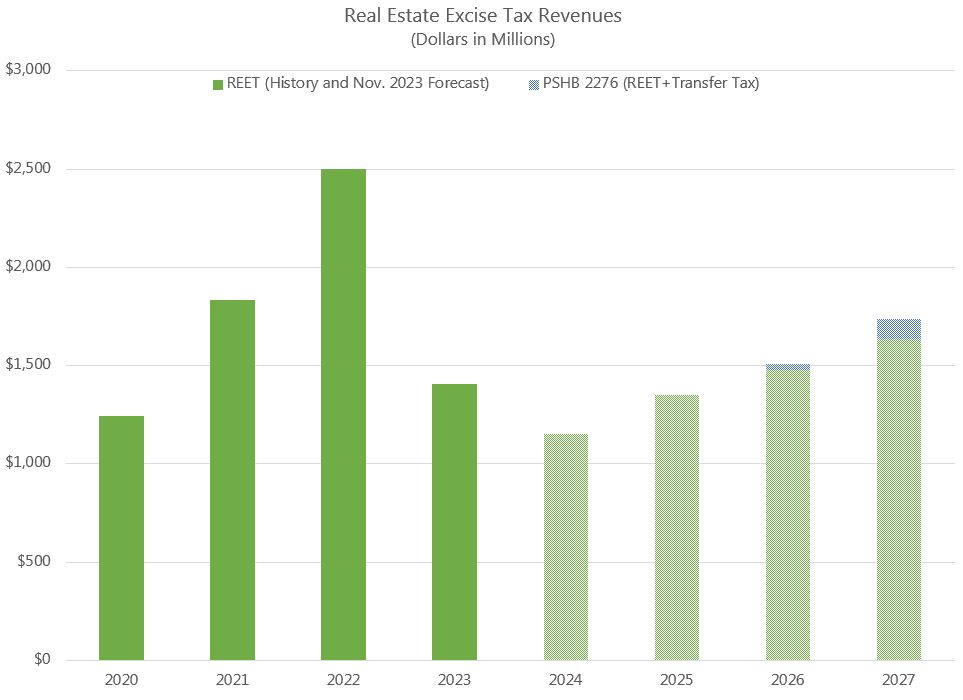

The preliminary fiscal note estimates that the proposed substitute would increase revenues by $133.6 million in 2025–27 and by $256.9 million in 2027–29. Most of that increase would go to five housing accounts ($132.3 million in 2025–27 and $252.7 million in 2027–29).

Under the bill as introduced, only 7% of the transfer tax revenues would go to the housing accounts. The proposed substitute provides that revenues from both the REET and the proposed transfer tax would be distributed to housing accounts. For both the REET and the transfer tax, 93.2% of revenues would be distributed as the REET is currently (79.4% to the general fund–state, 14.0% to the education legacy trust account, 5.2% to the public works assistance account, and 1.4% to the city-county assistance account). The remaining 6.8% would be distributed to five housing accounts (25% to the housing trust fund, 25% to the apple health and homes account, 25% to the affordable housing for all account, 15% to a new developmental disabilities housing and services account, and 10% to a new housing stability account).

According to DOR, the 93.2%/6.8% split was chosen in order to keep the accounts that are currently receiving REET revenues whole. The chart below shows the current forecast for REET revenues and adds in the estimated combined revenues from the REET changes and new transfer tax in the proposed substitute bill.

It seems to me that the proposed substitute is overly complicated. If the REET and the transfer tax would apply to the same amounts and their revenues would go to the same accounts, why go to the trouble of creating a new tax (rather than simply increasing the top REET rate to 4%)?

The bill title includes this: “an act relating to increasing the supply of affordable and workforce housing by reducing taxes on real property sales under $3,025,000.” It is not accurate to say that taxes would be reduced for all properties under $3.025 million. There would be no tax change for properties that sell for $525,000 or less. There would be small tax reductions for properties that sell for more than $525,000 up to $3,065,500. (For example, a property selling for $550,000 would pay $6,050 in REET, which would be $45 less than under current law. A property selling for $1.0 million would pay $11,450 in REET, which would be $405 less than under current law.) There would be tax increases for properties that sell for more than $3,065,500. The chart below shows the effect of the increased REET threshold and the new transfer tax by selling price.

Finally, the proposed substitute would require DOR to study how it might “implement and administer a local option graduated real estate excise tax.” A report would be due by Jan. 13, 2025.

Categories: Tax Policy.