1:54 pm

April 25, 2019

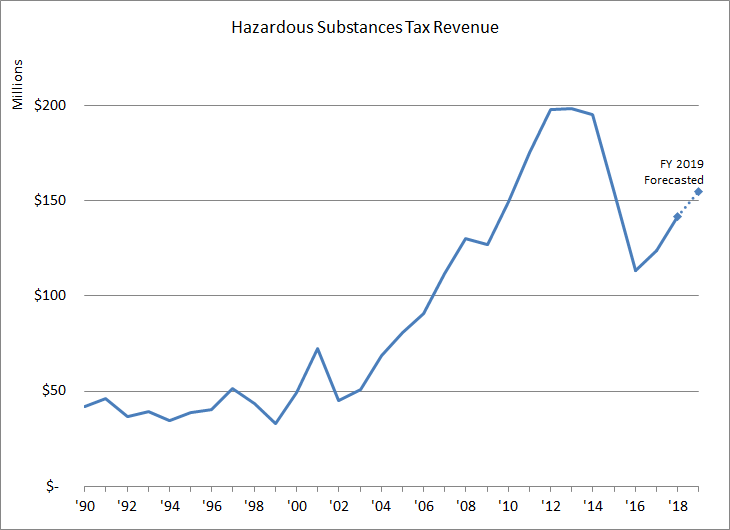

The state hazardous substance tax (HST) was created by Initiative 97, which voters approved in November 1988. This tax applies to various products deemed by the state Department of Ecology to present a threat to human health or the environment. The current tax rate is 0.7 percent of the wholesale value of the product. Petroleum products constitute approximately 95 percent of products subject to the tax.

HST revenue is dedicated to three accounts, the state toxic control account, the local toxic control account and the environmental legacy stewardship account. Money from these accounts is used for cleanup of toxic sites, solid waste management and certain operating programs.

The Senate Ways and Means Committee has passed out a bill intended to increase revenue from the HST while decreasing its volatility. This bill (Substitute Senate Bill 5993) would replace the current ad valorem HST with a volumetric tax. The initial rate for this tax would be $1.39 per 42-gallon barrel, approximately 3.3 cents per gallon. This rate would be increased annually by the percentage change in the implicit price deflator for investment in nonresidential structures (NRS IPD), which is a price index published by the U.S. Department of Commerce’s Bureau of Economic Analysis (BEA). Revenue from the new tax would be dedicated to three new accounts: (1) the model toxics control operating account, which would receive 45 percent; (2) the model toxics control capital account, which would receive 40 percent; and (3) the model toxics control stormwater account, which would receive 15 percent.

Because the wholesale prices of most petroleum products move up and down with the price of crude oil, revenue from the HST has been very volatile over the years, as shown in the chart below.

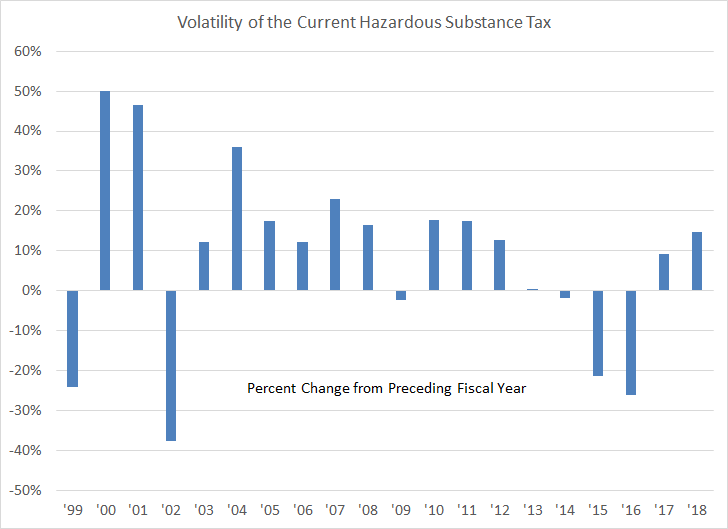

The HST’s volatility is emphasized in the following chart, which shows annual percentage changes in revenue for the last 20 years. This legislature’s affinity for highly volatile tax sources has become a trend. We previously published similar charts for the real estate excise tax [here] and a flat rate income tax [here].

A useful metric of tax volatility is the standard deviation of the percentage change in annual revenue. (See Pew Charitable Trusts’ methodology discussion here.) Over the 1999–2018 period, the standard deviation of the percentage change in HST revenue was 0.227, more than 4 times the 0.053 standard deviation of the state retail sales tax.

There is as yet no official fiscal note for SSB 5993. Senate Ways and Means Committee staff estimates that the volumetric tax would generate $600 million during the 2019-21 biennium compared to $310 forecasted for the existing ad valorem tax.

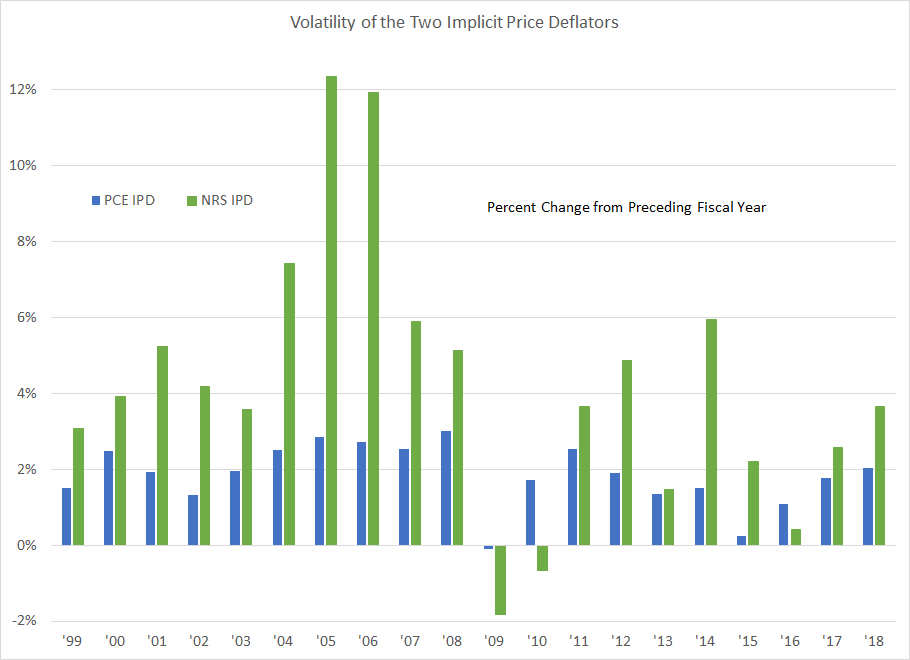

Historically, inflation measured by the NRS IPD has tended to exceed inflation measured by the BEA’s personal consumption expenditure implicit price deflator (PCE IPD), which is a more commonly used price index. Over the period from 1970 to 2018, for example, the average annual increase for the NRS IPD was 4.9 percent, while the annual average increase for the PCE IPD was 3.5 percent.

The NRS IPD has also been more volatile than the PCE IPD, as shown by the next chart, which compares annual percentage changes in the two IDPs from 1999 to 2018.

Retail customers ultimately bear the hazardous substance tax collected on products sold in the state. Shifting to a volumetric tax at the rate of $1.39 per barrel would likely increase the price of gasoline by approximately 1.7 cents. With indexing, this increment would increase over time. Indexed to the NRS IPD, the volumetric tax would be more stable then the current ad valorem HST. However, the volumetric tax would be even more stable if it were indexed to the more conventional PCE IPD.

Categories: Categories , Tax Policy.